The Inverting Yield Curve Is About More Than Recession This Time

A key slice of the U.S. yield curve inverted on Thursday for the first time since October.

(Bloomberg) -- A key slice of the U.S. yield curve inverted on Thursday for the first time since October, reviving memories of growth fears that plagued investors last year and signaling doubts that the Federal Reserve will succeed in reviving inflation.

The gap between the yield on three-month and 10-year Treasuries at one point slipped to as low as minus 2 basis points on Thursday. The spread -- seen by some as a warning signal because it has inverted before each of the past seven U.S. recessions -- last reached those levels as economic conditions deteriorated at the height of the trade war.

With the coronavirus outbreak threatening to disrupt the Chinese economy, concerns about the business cycle are undoubtedly a factor. But more important still are emerging doubts over the ability and commitment of policy makers to shore up growth and spur inflation.

The inversion has deepened since Chairman Jerome Powell and colleagues kept rates unchanged this week and signaled they would pull out all the stops to combat a global disinflationary downdraft.

Following his press conference Wednesday, fed funds futures showed increased conviction by traders that a cut is coming this year, although they continue to price in just one quarter-point reduction. Meanwhile, inflation-linked debt markets are expressing doubts that price pressures will increase, with so-called breakeven rates slipping in the wake of Powell’s comments.

“The bond market is basically telling the Fed that it hasn’t done enough and will be called back to do more and that the longer they wait the more they will have to do,” said Michael Darda, market strategist at MKM Partners. “If the bond market thought Powell’s comments on wanting higher inflation were credible in his press conference, you wouldn’t have seen break-even inflation rates falling as they did.”

A measure of core U.S. inflation released Thursday showed price pressures slowed to an annualized 1.3% in the fourth quarter from 2.1%, a weaker figure than analysts had expected.

Derailed Optimism

The yield curve has historically reflected the market’s sense of the economy, particularly about inflation. Investors who think inflation will increase typically demand higher yields to offset its effect. Because price growth usually comes from a strong economy, an upward-sloping curve generally means that investors have upbeat expectations.

The spread of the deadly virus from China has derailed new-year optimism among investors and thrown a spotlight on the ability of policy makers to handle a downturn. Merian Global Investors reckons the market is screaming for more easing. Societe Generale SA expects a 100-basis-point drop in the policy rate this year.

“People are looking for some form of safety and buying Treasuries out the curve is really the only way to do it,”said Nick Maroutsos, co-head of global bonds at Janus Henderson Group Plc. “The Fed has been adamant about pumping as much liquidity into the market as possible. And you could see the Fed try to pump even more in over time if this risk-off scenario continues -- to try to normalize the curve a little bit and bring front-end rates down.”

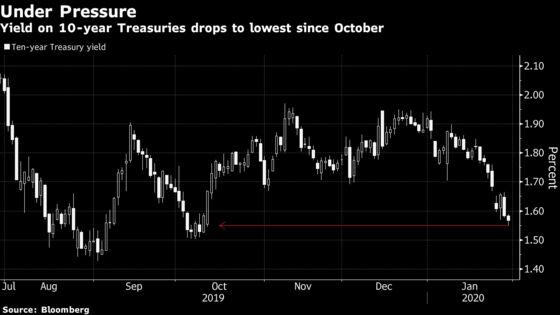

Falling yields also triggered other market dynamics which are exacerbating the move. Convexity hedging -- when mortgage portfolio managers buy or sell bonds to manage their duration exposure -- is back in play. As yields fall, they make purchases. The yield on 10-year Treasuries dipped as low as 1.53% on Thursday, the lowest since October.

The sequence of a swift drop in yields and curve flattening unleashing convexity-linked forces that re-starts the cycle is a recurring feature of the Treasury market .

A massive wave of convexity-related hedging in the swaps market in March helped send 10-year yields to levels then not seen since 2017. That came after the Fed took an abrupt shift away from policy tightening they had been doing in 2018. The Fed went on to cut rates three times over all of 2019.

Other factors may be at work now as well. Structural demand for long-dated Treasuries -- linked to liability-driven investment and hedging from foreign investors including Taiwanese insurers -- has helped to drive the curve flatter, according to Citigroup Inc.

Pascal Blanque, the chief investment officer at Amundi SA, said the market shouldn’t read too much into the latest yield-curve inversion.

“We don’t see these recent movements as indicators of a global or U.S. recession, but as an overreaction of financial markets that usually happens under these circumstances,” he said. The Fed’s decision Wednesday suggests that “despite the warning sign, there is no immediate need for further stimulus,” he said.

Still, the death toll from the coronavirus is climbing, and it means investors are likely to remain cautious. The risk of reduced economic activity is raising a chance of rate cuts, according to ING Bank NV.

The inversion “highlights broader market fears that the virus and its human and economic threat could spread,” wrote James Knightley, chief international economist at the bank. “The more that it does, the more likely it starts to alter consumer and corporate behavior, thereby promoting policy action to mitigate the dangers.”

--With assistance from Stephen Spratt.

To contact the reporters on this story: Anchalee Worrachate in London at aworrachate@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Benjamin Purvis, Elizabeth Stanton

©2020 Bloomberg L.P.