The Fed Isn't Heeding the Bond Market's Message

The Fed Isn't Heeding the Bond Market's Message

(Bloomberg Opinion) -- Rising wages have the U.S. Federal Reserve on track to raise interest rates by a quarter of a percentage point on Sept. 26. That would be the eighth increase since December 2015 and put the target for the federal funds rate in a range of 2 percent to 2.25 percent. And, the Fed may not stop there. Another 25 basis-point hike could follow on Dec. 19.

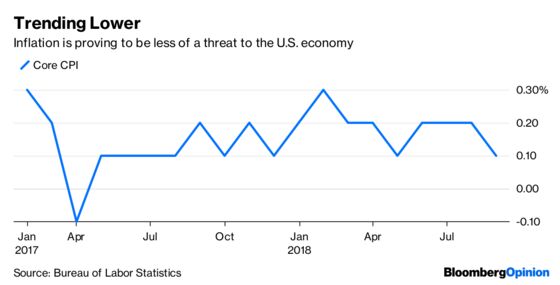

Although an acceleration in average hourly wage growth to 2.9 percent over the past year has increased pressure on the central bank to tighten monetary policy, the latest inflation data tell a different story. Reports last week showed producer prices dropping in August, consumer prices excluding volatile food and energy rising by a feeble 0.1 percent and the import price index falling the most since January 2016.

The financial markets are sending the Fed a powerful message. If the central bank continues to tighten policy despite signs of softness in inflation, it will not cause the gap in short- and long-term U.S. Treasury yields to widen as desired. Instead, it will succeed only in flattening and eventually inverting the yield curve. An inverted yield curve has been an almost sure-fire signal of a recession several months later. A mistake by the Fed would cause steep losses in equities as the economy goes into a recession as well as burn bond bears who have built bear-record bets against Treasuries.

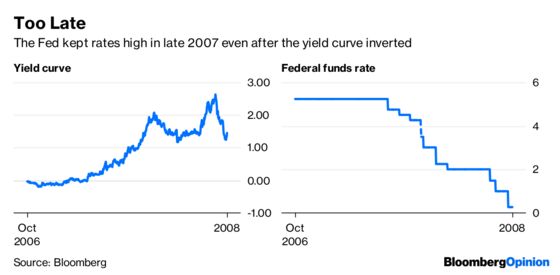

The Fed may be repeating the mistakes that were a contributing factor to the financial crisis a decade ago. Even though yield curve inverted in November 2006 with yields on two-year notes rising above those of 10-year notes, the federal funds rate remained elevated at 4.25 percent in December 2007 when the Great Recession began. Subsequent rate reductions came too late to materially affect the economy’s downward trajectory, especially after the collapse of Lehman Brothers Holdings Inc. on Sept. 15, 2008, making the Fed a follower rather than a leader for markets.

The Fed was not the only major central bank to maintain an excessively tight policy for too long. The European Central Bank was increasing rates as late as July 3, 2008, believing that the price of Brent crude reaching a peak of $146 per barrel that day was a sign of a strong global economy. In fact, high oil prices were really a reflection of a weak dollar. Oil producers raised prices to maintain purchasing power and not in reaction to a surge in global demand. When the dollar surged after September, the price of Brent crude collapsed to $38 per barrel in December.

The ECB may be repeating the error. Despite lowering economic growth forecasts for this year and 2019, President Mario Draghi announced on Thursday that monetary policy is set to tighten. Monthly bond purchases will be reduced from the current 30 billion euros ($35 billion) to 15 billion euros in October before ceasing at year-end. His reasoning is that even though inflationary pressures are muted, they are rising.

The impact of the tighter policies may already be apparent on both sides of the Atlantic. U.S. retail sales rose by 0.1 percent in August, the smallest gain since February, as higher gasoline prices curtailed consumers’ spending power. Higher borrowing costs resulting from Fed policy may further crimp consumer spending that accounts for about two-thirds of gross domestic product.

Euro zone growth has slowed since the end of 2017, and the exit of the U.K. from the European Union is set to occur next March with no agreement reached yet on the terms of the separation. Worries about a “hard” Brexit have created uncertainty for investors in the U.K. In addition, trade sanctions against EU exports being considered by U.S. President Donald Trump could be particularly harmful to the export-dependent German economy.

Bad central bank policies were a factor in the collapse in global markets a decade ago. A coordinated tightening of monetary policy in the U.S. and Europe could have similar implications for equity and bond investors today.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Komal Sri-Kumar is the president and founder of Sri-Kumar Global Strategies, and the former chief global strategist of Trust Company of the West.

©2018 Bloomberg L.P.