Debt Ceiling May Affect Markets Long Before It’s Reinstated

The Debt Ceiling May Affect Markets Long Before It’s Reinstated

(Bloomberg) -- Traders in short-term funding markets are already busy assessing the potential impact of the U.S. debt ceiling coming back into force in the second half of this year even as Congress trains its focus on more immediate matters like finalizing President-elect Joe Biden’s victory this week.

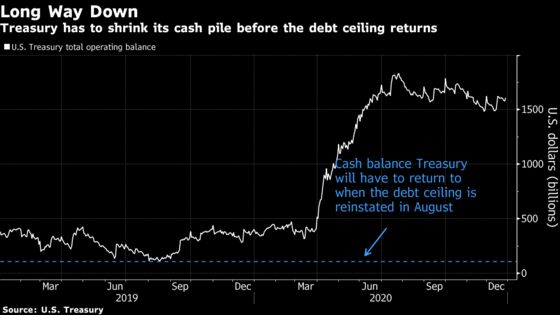

The country’s borrowing limit, which was suspended back in August 2019, is scheduled to come into effect once again on Aug. 1. Without a Congressional deal that extends or defers it once again, the Treasury will eventually have its ability to borrow curtailed, although it has historically found ways to delay officially hitting that limit.

Perhaps more critically for dollar funding markets, the reinstatement of the ceiling is also likely to cause the Treasury to slash its cash pile. Just how it does that could have a marked impact. The amount of cash that the Treasury currently holds is around $1.73 trillion, but it will need to whittle that down over the next seven months to the level it was at when the last ceiling suspension took place -- around $118 billion. That’s a far bigger reduction than it has historically had to do around debt-limit episodes.

The Covid-19 pandemic and the government’s response to its economic fallout are at the heart of this dilemma. To fund emergency stimulus measures, the Treasury ramped up its issuance of debt -- in particular short-dated Treasury bills. Now that they need to shrink the cash pile, there is a risk that the supply of bills will drop too quickly, forcing market rates below zero and forcing the central bank to intervene.

“The impending supply squeeze in the bill sector and the corresponding glut in the reserves market will be dominant themes for the front end this year,” Wrightson ICAP chief economist Lou Crandall wrote in a note to clients.

This could be a headache for the Federal Reserve because swings in the amount of cash that the government has deposited at the monetary authority have a direct impact on the level of bank reserves. By effectively ramping up the total amount of bank reserves in the system, there’s a risk that other assets get crowded out from lenders’ balance sheets, according to Crandall.

Read more on the Treasury cash balance here.

The central bank has already hinted that it could intervene should reserves flood the market. Lorie Logan, executive vice president at the Federal Reserve Bank of New York, said in a speech last month the central bank is prepared to tweak its interest on excess reserves rate if downward pressure on rates were to emerge. The rate was set at 0.10% back in March, which is 1 percentage point above the effective fed funds rate.

The minutes from the central bank’s Dec. 15-16 meeting, due for release Wednesday, may offer some further insight into how policy makers are thinking about a possible adjustment to IOER.

Besides the Fed taking action, Crandall said there are a few things Treasury could do, such as reduce the amount of weekly cash management bill offerings beginning in February and cut the outright size of the bill auctions in the second quarter. Just how the Treasury will engineer a decline in its cash balance over the coming months is “the central question,” according to Crandall.

©2021 Bloomberg L.P.