The Fed Balance-Sheet Contraction May Actually Boost Treasuries

The Dark Case for Both QE, QT Being Bad. And Treasuries as Haven

(Bloomberg) -- Could Treasuries, the asset scooped up by the Federal Reserve during its unprecedented quantitative easing rounds, also benefit from the central bank’s bond-portfolio run-off?

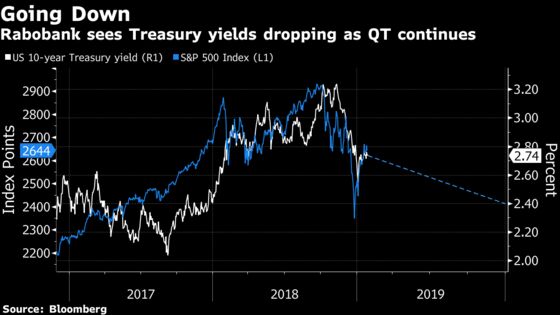

That’s the scenario painted by analysts at the Dutch lender Rabobank. Their thinking: quantitative tightening, or QT, will prove bad for economic fundamentals, in turn spurring haven demand for Treasuries. The team’s key takeaway is that the market implications of QT aren’t a mirror image of what happened in QE -- when bonds and stocks both benefited. Treasuries can still rally while risk assets slide under balance-sheet contraction, they argue.

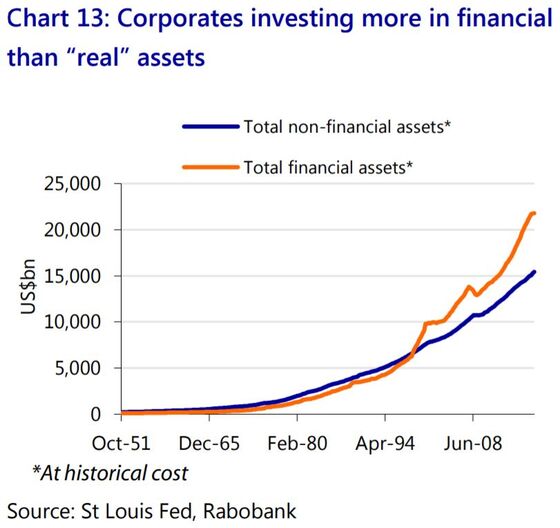

While most observers might credit the Fed’s first round of QE, launched in 2008, for preventing a wholesale financial collapse, subsequent rounds came under greater debate. Rabobank strategists led by Richard McGuire contend that they spurred companies to invest in financial investments rather than productivity-enhancing plant and equipment. And it kept inefficient operators alive -- so-called zombies -- through cheap borrowing costs.

“The risk of de-zombification will only build as corporates roll over more and more of their debt” at higher cost, London-based McGuire and colleagues wrote in a Jan. 25 note. “The exit of these companies from the market” will then trigger an economic downturn, they wrote. That in turn means that “yields will need to fall long before they are able to rise” in response to the Fed’s shrinking balance sheet.

The Rabobank team sees U.S. 10-year Treasury yields dropping to 2.40 percent by year-end, the lowest level since December 2017, the tail end of the quarter when the Fed began QT. The yields were at 2.74 percent as of 9:20 a.m. in London Tuesday, down from a 3.26 percent high reached last October.

For McGuire and his team, the likely consequences of QT go back to distortions from QE, which “accelerated an already clearly emergent trend of corporates investing in

financial rather than ‘real’ assets. Companies ramped up buybacks of their stock and made use of easy financing conditions to mount takeovers -- “investment designed to absorb somebody else’s output,” they wrote.

“The misallocation of capital away from the ‘real’ world explains the conspicuously low level of investment demand in recent years,” the Rabobank strategists wrote. “Next, the dearth of investment in fixed assets helps explain the sluggish nature of productivity growth in the post-crisis period.”

As unproductive companies find it harder to refinance, it will tip the economy into a slowdown -- spurring demand for Treasuries, they concluded.

To contact the reporter on this story: Christopher Anstey in Tokyo at canstey@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Ravil Shirodkar

©2019 Bloomberg L.P.