Risk Parity Trade Made Famous by Ray Dalio Is Now Ringing Alarms

Risk Parity Trade Made Famous by Ray Dalio Is Now Ringing Alarms

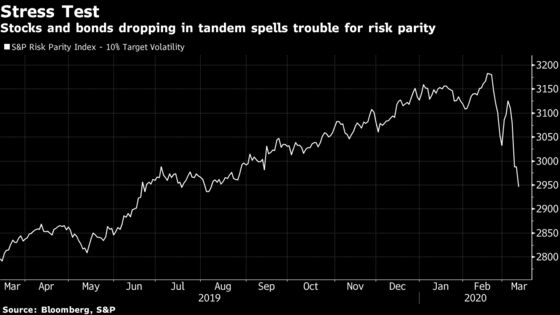

(Bloomberg) -- A booming quant trade touted for its diversification appeal is starting to feel the pain in this once-a-decade explosion of volatility. It’s also raising scary questions about billions riding the tried-and-tested link between stocks and bonds.

Known as risk parity, the levered-investing method made famous by Ray Dalio allocates to an array of assets based on their volatility. Before this week, it had -- at least on relative terms -- outperformed in the turmoil, benefiting from its outsized fixed-income exposure.

But now, just like for everything else on Wall Street, the worries are stacking up. The $948 million Wealthfront Risk Parity Fund lost more than 8% on both Monday and Wednesday. An S&P benchmark for the strategy has been suffering its worst start to a week since the global financial crisis.

Cracks are appearing as U.S. bonds had their worst two-day run since 1987 while the Dow Jones Industrial Average entered a bear market. Those moves hurt an inverse relationship that typically cushions losses for cross-asset portfolios.

Amid a spreading coronavirus outbreak and fears over the slow U.S. policy response there’s a breakout in cross-asset price swings of practically every asset class from bonds to commodities, and the turmoil is intensifying. The S&P 500 fell so fast it was briefly halted on Thursday. The benchmark European gauge was headed for its worst day ever.

While the amount of cash following risk parity strategies pales in comparison to the trillions controlled by human stock pickers and index funds, it’s morphed into the poster child of Wall Street’s volatility complex. The strategy oversees an estimated $500 billion of assets while volatility-targeting funds manage another $350 billion, according to a 2018 paper.

The trade has a reputation for exacerbating market sell-offs since it tends to deleverage when volatility is elevated. That’s not always a fair charge, and performance so far in the sell-off has been good. The strategy is down nearly 6% this year, about half of a classic portfolio that puts 60% in stocks and 40% in bonds.

Since most risk-parity products had been performing in line with the S&P benchmark, they likely hadn’t done anything too extreme, JPMorgan strategist Nikolaos Panigirtzoglou said on Tuesday. That may be about to change.

“Some risk parity funds that take an inverse correlation between stocks and bonds for granted may have been forced into deleveraging,” Masanari Takada, a quantitative strategist at Nomura Holdings Inc., wrote in a note.

Around 40% of risk-parity funds cut leverage on Wednesday, and the rest may wait till their regular re-balancing period, according to Takada’s estimates. That typically falls at the end of each month.

Deleveraging

Vontobel Asset Management’s risk-parity product has cut its stock position from 140% about a month ago to around 28%, while its bond exposure remains around 260%, says head of multi-asset Daniel Seiler.

“You reduce your volatility with a negative correlation and if that is not the case anymore, you will obviously need to reduce the volatility with a different measure and this could deleverage your whole portfolio,” he said from Zurich, referring to the link between bonds and shares.

On a positive note, for both asset classes to fall in tandem for an extended period, “what you would need is an inflationary shock and at the moment I don’t see that at all,” Seiler added.

With bond yields now so low, there are others on Wall Street who may disagree.

To contact the reporter on this story: Justina Lee in London at jlee1489@bloomberg.net

To contact the editors responsible for this story: Sam Potter at spotter33@bloomberg.net, Sid Verma

©2020 Bloomberg L.P.