The Bond Is in the Mail: Muni Market’s New Way Around Trump Ban

The Bond Is in the Mail: Muni Market’s New Way Around Trump Ban

(Bloomberg) -- Anyone who agreed to buy the bonds sold by Washington state this month has a long wait until they see a return on their investment: the nearly $400 million of securities won’t be delivered until March 2021.

The delay is the result of an increasingly popular maneuver that states and cities are using to get around a provision of President Donald Trump’s 2017 tax-cut law, which stripped them of their ability to sell tax-exempt bonds to refinance debt that can’t yet be called back from investors.

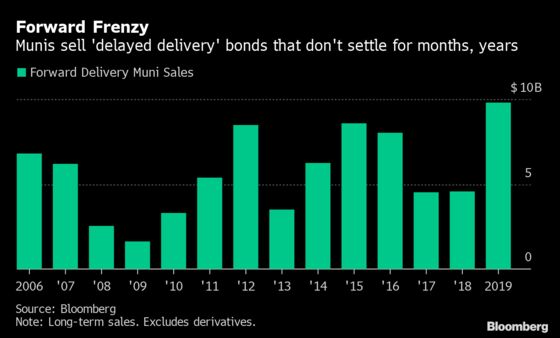

But with rates hovering near more than half-century lows, local governments are eager to refinance. So they’re selling bonds now that investors won’t receive until months -- or even years -- later when the outstanding securities can be bought back. There have been $10 billion of such municipal bonds sold this year, the most since at least 2005, with $1.4 billion in the last month alone, according to data compiled by Bloomberg.

The surge is the latest example of how much the little-known part of Trump’s tax law has shaken up the $3.8 trillion municipal market by doing away with a type of refinancing that once accounted for a big slice of the bond deals Wall Street banks arranged each year. It has also triggered a big increase in taxable municipal-bond sales because rates have fallen low enough that governments can still come out ahead by using them to pay off tax-exempt debt, which typically carries lower yields.

Illinois’s Metropolitan Pier and Exposition Authority is planning next week to sell $923 million in bonds that won’t be delivered to investors until March 2020. Washington D.C.’s airport authority is selling $364 million in bonds Dec. 12. Those won’t settle until July.

"The interest rates are just so favorable right now," said Larita Clark, chief financial officer of the Metropolitan Pier and Exposition Authority, which expects to save as much as $150 million. "We just wanted to lock in those rates."

After the Federal Reserve cut rates for a third time this year, Henry Dachowitz, the chief financial officer for Norwalk, Connecticut, decided to sell about $18 million of forward delivery bonds. He had been talking to multiple underwriters who were marketing the structure.

“The forward structure was new to me. I explored it and when I saw the present value savings were almost $2 million, it was compelling,” he said in an interview. “I thought interest rates if anything would go up. It was time to pull the trigger after the last rate cut.”

Washington delayed the delivery date longer than any other borrower this year, according to data compiled by Bloomberg. The nearly year-and-a-half wait did come with a price: the 10-year bonds were priced with a 2.3% yield, or 73 basis points more than top rated debt. Comparatively, the state in September sold 10-year bonds for 1.47%, a 16 basis-point spread.

Sylvia Yeh, co-head of municipal fixed income at Goldman Sachs Group Inc., said the deals are largely suited to bigger institutional investors, given the risks that could crop up between when the bonds are sold and when they’re delivered.

“The funds definitely have the opportunity to do this. For them it comes down to spread,” she said. “There is appetite at a price. That speaks to how our market continues to develop.”

--With assistance from Sowjana Sivaloganathan.

To contact the reporters on this story: Danielle Moran in New York at dmoran21@bloomberg.net;Fola Akinnibi in New York at fakinnibi1@bloomberg.net

To contact the editors responsible for this story: Elizabeth Campbell at ecampbell14@bloomberg.net, William Selway, Michael B. Marois

©2019 Bloomberg L.P.