The Average U.S. Stock Is Catching None of That Megacap Magic

The Average U.S. Stock Is Catching None of That Megacap Magic

(Bloomberg) -- If you own the biggest American companies, congratulations: you’ve nearly made up your losses. But if you own practically anything else, the wounds are far from healed.

Rarely have lines between the haves and have-nots been more pronounced than in the 2020 stock market, where capitalization-weighted indexes -- ones sorted by size -- are trouncing their egalitarian brethren by some of the widest margins ever. It’s not just a story of small-cap weakness. Even in the realm of big companies, size is telling the whole story.

Consider the Nasdaq 100, sitting just a few points away from erasing an annual decline that was once as big as 20%. An equal-weighted version of the same index, one in which Amazon.com counts as much as American Airlines, is still more than 7% away from completing the feat.

It’s worse in the S&P 500, now down 12% in 2020, whereas the equal-weighted index has fallen nearly twice that. The phenomenon, bad news for active managers who are less wedded to index weightings, highlights an underemphasized fact of the coronavirus rout: the typical U.S. stock had a much worse time than major benchmarks showed.

“Megacaps make up the biggest part of the upside,” said Gary Bradshaw, a portfolio manager at Hodges Capital Management in Dallas. “You take them out and the market wouldn’t be where it is today.”

Equal weight indexes are so much farther away from erasing losses because they fell so much more in March. While most investors are aware cap-weighted indexes like the S&P 500 had their fastest-ever bear market plunge last month, the pain in benchmarks that strip out market-value biases was significantly worse. The equal-weighted S&P 500 fell almost 40% during the rout.

The disparity reflects the nature of the threat. A spreading virus that’s caused global economies to shutter has raised the specter of a credit crunch and insolvency. More than before, investors are laser focused on measures of company quality, cash balances and liquidity. In that type of environment, the size of a company matters.

Among 10 quantitative factors tracked by Bloomberg -- which classify stocks based on different characteristics like growth potential or volatility -- a measure of size is the second best performing this year, only behind profitability. A pure portfolio focused on firm size just had its best quarter ever in data that goes back two decades.

Some of America’s largest companies are also in a position potentially to benefit from the aspects of the crisis, or at least demonstrate resiliency. Microsoft has seen demand for its cloud services rise, while Amazon is hiring thousands of more workers to counter incessant interest in its e-commerce business. Google parent Alphabet and Apple announced they’re teaming up to develop a contact tracing system for Covid-19.

“Your tech names had such high valuations going into the crisis, you would have expected them to have some of the biggest drawdowns,” said Lauren Goodwin, economist and multi-asset portfolio strategist at New York Life Investments. “They don’t because they have high levels of cash availability, everyone they employ can work from home, they are the creators of the tools for the rest of us to work from home, and they’ve invested in themselves. Those are characteristics of a very Covid-resilient business.”

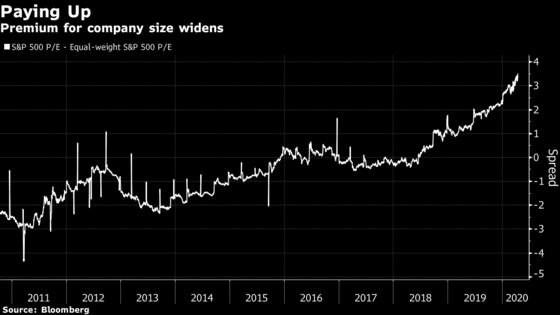

Whereas the S&P 500 now trades at 18.6 times booked profits after a 16% contraction in its P/E multiple, the benchmark’s equal-weight counterpart trades at just 15 times earnings. The premium for the market-cap weighted index is the widest since 2008, showing just how sacred megacap firms have become. And Hodges Capital Management’s Bradshaw sees reason for that to continue.

“Five or six megacaps are the ones that are putting up the best revenue growth, the best earnings growth,” he said. “They’re getting higher multiples, but they’re going to continue to pull the wagon. They’re the lead horses out there and that’s going to continue.”

There’s also an element of safety. Investors grew used to the biggest companies growing even larger, dominating market-cap weighted indexes. At the start of the year, the top five publicly-traded American companies made up a record 18% share of the S&P 500. Through the 11-year bull market that just recently ended, the S&P 500’s five biggest companies accounted for more than a fifth of the index’s 400% gain.

“It’s partially what people are comfortable getting into in a market downturn,” said Sam Huszczo, the founder of SGH Wealth Management. “The large cap space is still the juggernaut, large cap stocks have more stability.”

©2020 Bloomberg L.P.