The ‘Absurd’ Muni-Market Signal Showing SALT Tax Pinch

The ‘Absurd’ Muni-Market Signal Showing SALT Tax Pinch

(Bloomberg) -- The $3.8 trillion municipal-bond market offered yet another sign this week that the new tax regime may be painful for some Americans.

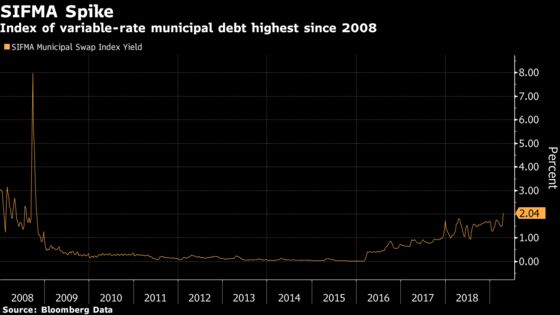

An index of variable-rate municipal-bond debt saw the biggest jump in yields since 2008 on Wednesday, an increase likely due to retail investors selling their holdings to pay their tax bills. The bump in yields typically occurs in March and April ahead of the tax filing deadline, but this year’s jump was delayed -- suggesting that investors waited until the last minute to file their returns with the U.S. Internal Revenue Service.

Congress in late 2017 approved a tax overhaul that capped how much state and local taxes can be deducted from federal returns, hitting high-tax states like New York and California hard.

Nisha Patel, portfolio manager for Eaton Vance Management, said investors likely sold the securities to raise what could be thousands or tens of thousands of dollars for tax-related costs. "There were a lot more redemptions," she said.

The SIFMA Municipal Swap Index reset Wednesday at 2.04 percent, a 50 basis point increase from the previous week, putting the yield at the highest since 2008. The yield is the same as AAA-rated municipal bonds maturing in 11 years -- something that Patel called “absurd.”

The later-than-typical increase in the index during tax season is also due to mutual funds buying variable rate securities as yields on fixed-rate, tax-exempt debt have been lower than those on U.S. Treasuries, making muni bonds expensive on a relative basis, said Vikram Rai, head of muni strategy at Citigroup Inc. Rai estimated in an April 15 report that the SIFMA index would reset “significantly higher” this week by 25 basis points or more.

“The bond funds temporarily parked a lot of their money into VRDNs,” Rai said. “So basically they made up for the lack of demand from money market funds.”

Unlike fixed-rate bonds, variable-rate municipals can be sold at full face value anytime. The index should decline again as the spike in yields should attract buyers, Patel said.

“I imagine it’ll pop right back down,” said Patel, who said she expects it to reset lower next week as investors see the higher yields and buy up the debt. “It’s going to drive a lot of flows in. Even institutional investors like us will buy knowing full well it’ll reset lower next week.”

To contact the reporters on this story: Amanda Albright in New York at aalbright4@bloomberg.net;Michelle Kaske in New York at mkaske@bloomberg.net

To contact the editors responsible for this story: James Crombie at jcrombie8@bloomberg.net, Michael B. Marois, Allan Lopez

©2019 Bloomberg L.P.