The $6 Billion Arbitrage Trade That Kept the Koruna on a Leash

The $6 Billion Arbitrage Trade That Kept the Koruna on a Leash

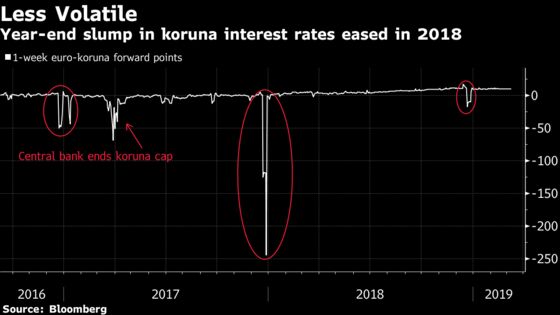

(Bloomberg) -- The closing weeks of each year used to bring increased volatility to Czech markets that was unpleasant to foreign investors and the central bank alike. The end of 2018 turned out to be remarkably quiet.

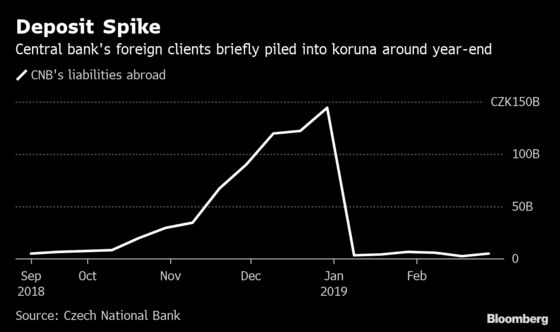

The reason was that some market players engaged in a series of cross-border transactions, moving an equivalent of about $6 billion in koruna from the Czech Republic and quickly depositing them back with the country’s central bank to profit from the year-end mispricing of Czech assets.

“This limited the market distortion,” policy maker Tomas Holub said Friday, adding the central bank didn’t initiate the transactions. “Any market distortions aren’t exactly welcome by market participants as well as the central bank, and in that sense we obviously didn’t mind the reduction of the distortion.”

Lenders in Europe are obliged to pay contributions to a deposit insurance fund based on the size of their balance sheets on the last day of each year. This is particularly painful for banks in the Czech Republic, which hold much more deposits than loans. To lower the payments to the so-called resolution fund, they try to temporarily shrink their liabilities by switching from cash into other instruments or currencies.

The resulting brief koruna weakness and a drop in short-term interest rates have irritated foreigners, who piled into the Czech currency during the central bank’s 2013-2017 intervention regime, because it hurt their annual returns.

Czech central bank data show it accepted about 140 billion koruna ($6.1 billion) in deposits from abroad in the last six weeks of 2018 as domestic lenders were pulling money from their accounts with the monetary authority. Both flows were almost fully reversed in the first days of the new year.

“I think we don’t have a reason to change our approach in the future,” Holub said. “The only conclusion that can be made from this is that there are institutions that can use the market distortion to look for some return as part of their portfolio management, and of course any arbitrage using market distortions has a tendency to reduce those distortions.”

The monetary authority, whose foreign clients comprise mainly other central banks and international institutions but could also include private entities, didn’t disclose any details about those conducting the trades.

--With assistance from Marton Eder.

To contact the reporter on this story: Krystof Chamonikolas in Prague at kchamonikola@bloomberg.net

To contact the editors responsible for this story: Blaise Robinson at brobinson58@bloomberg.net, Peter Laca, Michael Winfrey

©2019 Bloomberg L.P.