Dismayed by Musk’s Antics? Investors Aren’t

Dismayed by Musk’s Antics? Investors Aren’t

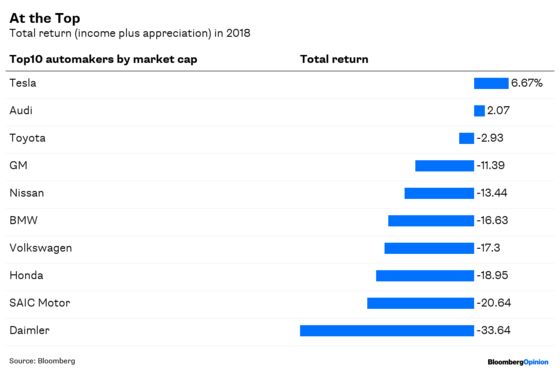

(Bloomberg Opinion) -- Stocks of automakers in China, France, Germany, India, Japan, South Korea and the U.S. are down as much as 36 percent in the worst year for equities since 2011 amid slowing global growth. Only one of the world’s 10 most valuable car companies is setting sales records and outperforming the equity market. That would be Tesla Inc., proving that the zero-emission future works.

For all his trouble as the world’s most-ridiculed and penalized chief executive officer (the Washington Post called him “a double-turkey” at Thanksgiving for “a totally nonsensical tweet in August” that prompted a Securities and Exchange Commission settlement removing him as chairman with a $20 million personal fine), Elon Musk made 7 percent for shareholders in 2018. The Model 3 battery electric vehicle, meanwhile, became the best-selling car in America by revenue and the six-year-old Model S BEV remains No. 1 in customer loyalty. The company even reported a profitable third quarter in October, just the third in-the-black showing in its history.

How is the rest of the industry, still overwhelmingly committed to fossil fuel, doing? Daimler AG, the parent of Mercedes, lost a third of its value. Porsche Automobil Holding SE declined 23 percent. BMW AG, which brands its product “the ultimate driving machine,” made stockholders 17 percent poorer. Even Toyota Motor Corp., the global No. 1 making everything from the popular hybrid Prius to the esteemed Lexus luxury line, is down 3 percent. All of the giants, including General Motors Co., Ford Motor Co. and Fiat Chrysler Automobiles SA, reported minuscule sales growth the past five years, a major reason why they are investor also-rans.

Hardly a day passes without breathless write-ups of Tesla killers. Except nobody has done it yet. That’s why Tesla became No. 3 in market capitalization among the 20 largest automakers with a total return (income plus appreciation) dwarfing the few that are up on the year when the industry average was a loss of 13 percent. Tesla also produced the greatest risk-adjusted return, which is the market’s way of saying that Tesla investors received the most compensation for price fluctuations, according to data compiled by Bloomberg.

During the past five years, Tesla’s market capitalization almost quadrupled, easily beating Fiat Chrysler (2.2 times), GM (decline of 13 percent), and Ford (decline of 44 percent), while Tesla sales exploded (6 times). Revenue for Fiat Chrysler and Ford appreciated 9 percent and 7 percent respectively and GM’s declined 6 percent, according to data compiled by Bloomberg. Tesla’s 82-percent sales growth made it No. 1 among 40 companies in the Bloomberg Intelligence Global Automobiles Valuation Peer Group in 2018, and 26 analysts surveyed by Bloomberg predict that Tesla will lead the industry again in 2019 (38 percent) and in 2020 (20 percent).

Tesla’s relationship with its shareholders is similarly exceptional in the face of relentless news reports saying the company “burns through cash.” The $11 billion invested by mutual funds in Tesla represents 1.2 percent of their assets. That commitment is substantially greater than the 0.7 percent of assets by 298 funds investing $7.7 billion in GM, according to data compiled by Bloomberg. The same 159 funds holding Tesla produced a 1.9 percent risk-adjusted return the past three years, easily beating the 1.5 percent by 472 mutual funds holding other U.S. carmakers, according to data compiled by Bloomberg.

For some of these mutual funds, Tesla has been the gift that keeps on giving. The $5 billion T. Rowe Price Global Technology Fund produced a 120 percent total return during the past five years, the best of a group of 367 funds. Since money manager Joshua Spencer assumed control in 2012, Tesla’s weighting in the fund increased to 8.5 percent from zero, based on public data as of September.

Tesla remains a favorite target of short sellers led by Jim Chanos, who use sales of stock they don’t own to capitalize on anticipated price declines. Tesla’s ratio of shorted shares to its total tradeable shares was 22 percent, greater than any of the companies in the S&P 500. But the short sellers continue to be frustrated by the company’s resilience and the present short-interest ratio is a shadow of the 70 percent that greeted the company when it went public eight years ago.

“Elon Musk has made such a sideshow of himself that people started to forget about — including myself — the underlying business,” said Citron Research’s Andrew Left, a prominent short seller, on Bloomberg TV in October. “It’s a revolution that I actually underestimated — the way people are buying these cars.”

Left, who predicted that Tesla would decline to $100 a share by the end of the year from its current $332, became an enthusiast two months ago. That’s when he wrote: “While the media has been focused on Elon Musk’s eccentric, outlandish and at times offensive behavior, it has failed to notice the legitimate disruption of the auto industry. While everyone is focused on Elon smoking weed, he is quietly smoking the whole automotive industry.”

(With assistance from Shin Pei)

To contact the editor responsible for this story: Jonathan Landman at jlandman4@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Matthew A. Winkler is a Bloomberg Opinion columnist. He is the editor-in-chief emeritus of Bloomberg News.

©2018 Bloomberg L.P.