The Best Single Change to the Tax Code? We Have 7 Ideas

The Best Single Change to the Tax Code? We Have 7 Ideas

(Bloomberg Opinion) -- The Tax Cuts and Jobs Act of 2017 left some Americans celebrating their gains, others decrying losses, and a good chunk of the nation unsure of what to think, actually. That’s to be expected – it will take time to understand the true impact of such sweeping changes. For Tax Day, we posed a simpler question to our columnists: What single change in tax policy would do the most good for the nation? They offered the following suggestions.

Make the Tax Credit for Children Permanent

Perhaps the most popular feature of the tax law Republicans enacted in 2017 was its modest provision of tax relief for parents. The law eliminated the dependent exemption but expanded the tax credit for children by more than enough to make up for it. But the law made this pro-parent tax cut temporary. Republicans defended making it temporary on the theory that a future Congress would find it politically imperative to extend it.

I hope it will. Congress should make the enlarged tax credit for children permanent and make it grow automatically as nominal wages rise. Parents, and especially parents of larger families, pay too large a share of the costs of modern government. The tax credit is already too small to offset this tendency, and should not be allowed to shrink further. RAMESH PONNURU

Take Down the Stepped-Up Basis

The tax law doubled the threshold at which the estate tax kicks in -- making it even more essential to do away with a decades-old capital gains loophole for wealthy heirs. Known as stepped-up basis, the tax code lets heirs drastically reduce their tax bills for inherited assets by ignoring any gains before they acquired them. That means any appreciation of those assets during the original owner's lifetime could potentially escape taxes entirely if the estate is below the new $22 million estate tax limit for married couples. It's hard to make the argument that changing the tax treatment of inherited wealth will somehow inhibit economic growth. Instead, the loophole is really just helping the rich get richer. Of course, other changes would be needed to complement an end to stepped-up basis and help to reform the estate tax system, but targeting this giveaway is a good place to start. The president even seemed to think so too, at one point. ALEXIS LEONDIS

My First VAT

Just one change to the tax code could both stabilize state finances and protect against a federal budget crisis in this age of chronically low interest rates and deficit-financed tax cuts: a Value Added Tax.

Crucially, it should keep the rate very low, from a half percent to one percent. And state governments should have the opportunity to piggy back on the federal program. VATs are similar to sales taxes but they are much more broadly based and less regressive. If a state switched from using the sales tax to piggy backing on the federal VAT, its revenues would be more stable and the burden on the working poor would be reduced. The rate on VATs could also be much lower while bringing the same revenue as a sales tax.

State coordination would also encourage the federal government to hold down its own VAT rate in normal times. If interest rates started to soar and the federal debt became unsustainable, the VAT would be the perfect tax to replenish the budget. A rough rule of thumb is that a five percent VAT would reduce the deficit by three percent of GDP.

That’s a stiff but manageable surcharge for Americans to pay and a strong incentive for Congress to find a more permanent solution to any government budget crisis. KARL W. SMITH

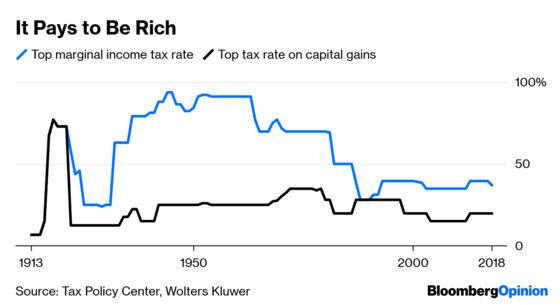

Increase Taxes on Long-Term Capital Gains

The single most consequential change to the tax code would be to raise the tax rate for long-term capital gains and qualified dividends to match rates for income taxes. We should do it immediately.

Unlike wealth taxes or 70 percent tax rates on the incomes of the rich, a fix for capital gains is politically plausible in the near term while still addressing the issue of income and wealth inequality. In fiscal 2016, Americans declared income of roughly $200 billion from qualified dividends and $300 billion from long-term capital gains, taxed at a rate of 15 percent. If that were instead taxed at a rate of 35 percent, it would raise an additional $100 billion in revenue. That revenue could be used to lower taxes elsewhere, to reduce the deficit and the national debt, or to pay for any number of programs.

Most financial assets are held by the rich. To the extent that middle-class Americans hold financial assets, they're generally tax-deferred in the forms of individual retirement accounts and 401(k) plans, and at retirement when those assets are withdrawn they're taxed at ordinary income rates.

There's no good reason rich people should pay a lower tax rate on their investments than middle-class Americans do on their investments or labor. Bill Gates agrees. It's the best way to reform the tax code to reduce inequality and raise revenue in a politically plausible way. CONOR SEN

QBI Deduction for All

The 2017 Tax Cuts and Jobs Act was billed as a middle-class tax cut. It wasn’t, but we can fix that. The law created a new tax deduction of up to 20 percent of qualified business income, or QBI. But it’s only available to business owners including S corporations, limited-liability companies, sole proprietorships and other pass-through businesses. A friend of mine — a certified financial planner in California — tells me his own taxes are down more than $20,000 this year as a result of the new deduction.

With this change to the tax code, taxpayers who earn less than $157,500 (single), or $315,000 (married filing jointly), can deduct 20 percent of the QBI they receive via pass-through businesses from their overall taxable income. If they earn above those amounts as service professionals — for example, as doctors, lawyers or accountants — the deduction begins to decline, and is fully phased out with earnings above $207,500 (single) or $415,000 (married).

Why not extend the same QBI deduction available to taxpayers who qualify as “specific service trade and businesses” to everyday W-2 wage earners? Let them pay tax on only 80 percent of their hard-earned income, too.

If it’s good for a self-employed financial planner, or a CPA, lawyer or doctor, why not extend the same tax break to the folks who make their living earning W-2 income? Viola! Middle-class tax cut. STEPHANIE KELTON

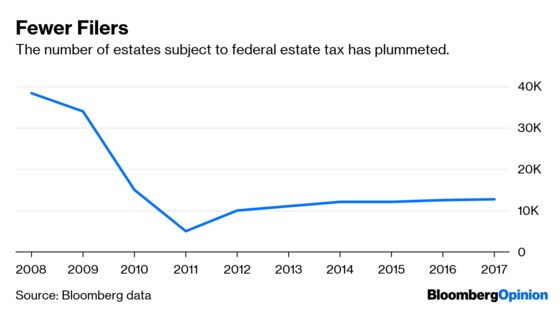

Lower the Estate Tax Threshold

How to salvage an American economy undermined by college and health care costs that widen inequality, by stagnant middle-class incomes, by crumbling bridges, tunnels and infrastructure, and by declining life spans? That would be the estate tax.

It remains the closest thing to Adam Smith's “invisible hand” invigorating capitalism by requiring the super-rich to do what Warren Buffett, Bill and Melinda Gates, and almost 200 other billionaires (including Michael Bloomberg, the owner and publisher of this news organization) have already pledged to do: Give at least half of their net worth to philanthropy.

After Congress increased the filing threshold to $5.49 million from $2 million, estate tax returns declined almost 67 percent to 12,711 in 2008, according to the Internal Revenue Service. More than 38,000 people filed returns when the exemption was $2 million. Estate tax revenue totaled $20 billion in 2017 – a reflection of the huge creation of wealth since the financial crisis. So if the exemption returned to $2 million, annual revenue would at least triple, to $60 billion. That's about 9 percent of the $680 billion budget deficit in 2017. What are we waiting for? MATTHEW WINKLER

Stop Encouraging Corporate Debt

The U.S. tax code pushes companies to load themselves up with debt. By making most interest payments tax-deductible, it encourages borrowing instead of equity finance. This has a number of negative effects on the economy. First, high amounts of leverage can create the risk of a financial crisis; the popular practice of borrowing money to buy back shares or execute mergers has exacerbated the problem. Leverage can also dramatically increase the economic damage from a financial crisis, by suppressing investment after a crash, and by making the economy vulnerable to a spiral known as debt-deflation. Third, privileging debt finance over equity finance encourages private-equity firms and hedge funds to buy companies and load them up with debt, leaving them far more vulnerable to bankruptcy while too often failing to fundamentally increase the efficiency of operations --- something that private equity is supposed to do. President Donald Trump’s recent tax reform limited the deductibility of interest payments, but future reforms should phase it out from the tax code. NOAH SMITH

Double the Childless EITC

The 2017 tax law did not expand the earned-income tax credit for adult workers without dependent children. After years of rhetorical support from Paul Ryan, then speaker of the House, this missed opportunity landed with a thud.

Previous EITC expansions have significantly increased the rate at which targeted populations participate in the workforce by using federal dollars to supplement earnings from paid employment. Because the credit is based on household income, the EITC is highly focused on providing benefits to the working poor. And each year the credit lifts millions of people, including several million children, out of poverty.

The EITC is currently designed to support households with children — it offers very little benefit to childless adults. Such a worker is eligible for a maximum credit of about $500 per year, compared to over $5,700 for a worker with two kids.

Childless adults with relatively less education are a group with troublingly low workforce participation. A more generous EITC for them would likely increase employment, incomes — and help to provide the dignity that comes with paid work. A modest expansion of the credit could easily be financed by curbing deductions and exclusions in the tax code, redirecting spending from the well-off to the working poor without increasing the deficit.

Congress should double the childless EITC. MICHAEL STRAIN

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mike Nizza is an editor for Bloomberg Opinion. He was the executive editor of BloombergPolitics.com, as well as an editor at Esquire Digital, News Corp.’s the Daily, the Atlantic Media Co.’s Innovation Center and the New York Times.

©2019 Bloomberg L.P.