Taiwan Bond Binge Leaving a Mark on the U.S. Treasury Market

Taiwan Bond Binge Is Leaving a Mark on the U.S. Treasury Market

(Bloomberg) --

A flood of fund raising by American blue-chip firms in Taiwan is putting pressure on longer-dated Treasuries, a showcase of how hedging flows are moving markets worldwide.

AT&T Inc. and Verizon Communications Inc. have led a sale of more than $14 billion of so-called Formosa bonds, dollar debt listed in Taiwan, this year. Hedging the risks for these long-maturity notes has set in motion a chain of events that distorts the U.S. yield curve.

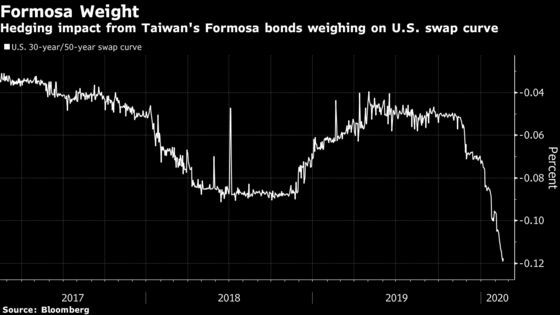

As the bond sales picked up pace in the past weeks, the ultra long-end of the swap curve, a gauge of U.S. interest rates over different maturities, has flattened sharply. The spread between the 30- and 50-year rates slumped to minus 13 basis points Wednesday, the lowest in at least a decade.

“We believe that the recent flattening of the 30s50s curve has been driven by the combination of Formosa issuance and European asset and liability management demand, as well as domestic pension demand,” Citigroup Inc. strategists including Ruslan Bikbov wrote in a Feb. 16 note. “Formosa issuance has been, perhaps, the most tangible flow.”

Here’s a closer look at the Formosa phenomenon and what it means for U.S. rates:

Why Are Formosa Sales Growing

Taiwanese insurance companies are flushed with cash, and have limited room to venture overseas given regulations limiting their foreign exposure. Local-currency bonds have long lost their allure, with benchmark yields trading close to record lows of just under 60 basis points.

Who is Issuing Them

The Formosa market is a favorite with global debt issuers such as technology giants Apple Inc. and Intel Corp. AT&T priced a record $3 billion sale last Thursday, capping a week of issuance from companies including including Citigroup and Verizon.

Forty-year bonds have replaced 30-year equivalents as the most common maturity sold in 2020. This means hedging activity has shifted into even longer-dated securities.

For more details on Formosa bond issuance click here.

How Does the Hedging Work

Formosa bonds tend to have a fixed coupon. Many debt issuers, particularly finance companies, would often enter into an interest-rate swap with a dealer to switch to floating rates to match their cash flows.

The dealer then hedges its position by buying Treasuries or receiving fixed-rate interest rate swaps. Both of these activities put downward pressure on long-dated Treasury yields.

Issuers also have the option to call the bond -- that is to pay investors back before it’s due. They often sell this right to dealers to lower the cost of the debt sale.

Dealers who buy these call options will hedge their exposure by selling similar long-dated volatility derivatives. That in turns flattens the so-called expiry curve, the plot of implied volatilities of swaptions -- options on swaps -- with different maturities.

According to an estimate by Goldman Sachs Group Inc. strategists Praveen Korapaty and William Marshall, $10 billion of Formosa debt sale could flatten the expiry curve by about 2 annualized basis points. Their calculations do come with a lot of moving parts -- changes in levels of volatility, rates and dealer inventory all affect any projections.

How Much More Issuance Can We Expect?

Demand for foreign-currency bonds in Taiwan will likely remain strong this year as insurers reinvest cash from a wave of redemptions. The $15.5 billion of debt maturing this quarter is more than double the $7.4 billion in the previous three months, according to data compiled by Bloomberg.

Formosa sales in 2020 may surpass the average amount raised in the past two years, according to Ernst Grabowski, head of Asia-Pacific debt syndicate at Morgan Stanley. Goldman predicts about $22 billion of issuance this year.

--With assistance from Miaojung Lin.

To contact the reporter on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2020 Bloomberg L.P.