Best Days May Be Over for World-Beating Philippine Bonds

Best Days May Be Over for World-Beating Philippine Bonds

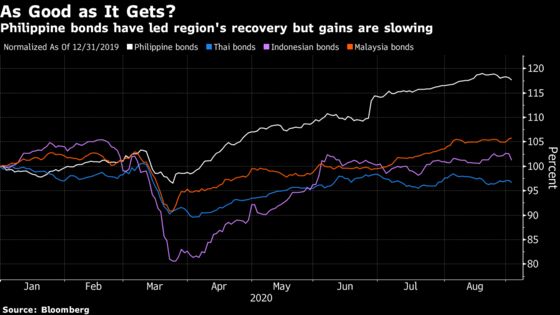

(Bloomberg) -- Philippine peso bonds have outpaced every other major emerging market this year but their halcyon days may be over.

Gains will be harder to come by in coming months after the central bank dialed down expectations for further interest-rate cuts by saying it had entered a “prudent pause.” At the same time, policy makers are seen slowing bond purchases after snapping up an estimated 45% of the government’s domestic borrowings during the first seven months of the year.

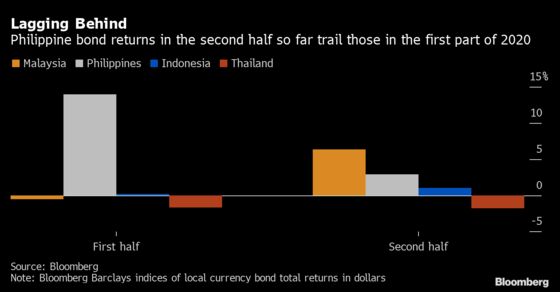

The nation’s sovereign debt has returned 18% this year to dollar-based investors, while the next best Southeast Asian performer, Malaysia, has gained just 6%. The rally in local bonds has seen the benchmark 10-year yield tumble more than 150 basis points since the end of December to 2.75% after touching a record-low 2.52% last month.

Investors hoping for further policy easing to underpin gains are likely to be disappointed. The central bank, which has ratcheted down its benchmark rate by 175 basis points this year, is set to stay on hold for at least the next six months, according to economists surveyed by Bloomberg. There’s no need to cut rates again anytime soon, central bank governor Benjamin Diokno said in late August.

The other main pillar of this year’s rally -- central bank bond buying -- is also looking less impressive. The central bank purchased about 800 billion pesos ($16.5 billion) of government debt through the end of July to help stabilize financial markets, according to Bureau of the Treasury data compiled by Bloomberg and confirmed by analysts. The pace of purchases will probably be lower over the rest of the year, Diokno said last month.

Bond auctions are also starting to give out less positive signals. The government rejected all bids at a 30 billion peso sale of 2033 debt on Aug. 25, saying the yields being sought by investors were “way too high.” The elevated yields being asked may just have been a function of technical factors rather than a worsening of sentiment toward government bonds in general, according to the Asean+3 Macroeconomic Office, a regional government-owned research group.

A final factor likely to weigh on demand for Philippine bonds is the smaller real-yield premium relative to their regional peers. The consumer price index was 2.4% in August, up from as low as 0.8% last October. The rising trend has pushed down inflation-adjusted yields on the nation’s 10-year debt to around 0.5%, the lowest in the region.

“The real-yield differentials over U.S. Treasuries are not particularly appealing, while the central bank is probably done with rate cuts,” said Frances Cheung, head of Asia macro strategy at Westpac Banking Corp. in Singapore. “As such, we are neutral on Philippine bonds.”

There has been a remarkable recovery for the nation’s bonds since the depth of the coronavirus sell-off, and one that has been very profitable for investors. An honest appraisal of the outlook now however suggests the immediate future is likely to be a great deal less rewarding.

What to Watch

- Indonesia will report foreign-exchange reserves data on Monday

- Bank Negara Malaysia will deliver a policy decision Thursday, with bets for another rate reduction helping make Malaysian bonds the top performers in emerging Asia in the second half

- The Philippines will sell 30 billion pesos of three-year bonds on Tuesday, and release trade data on Thursday

Note: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice.

©2020 Bloomberg L.P.