Angst in Bills Market Gets a Break: Debt Ceiling Anxiety Tracker

T-Bill Distortions Are Deepening: Debt Ceiling Anxiety Tracker

(Bloomberg) -- Treasury-bill dislocations continued to wane as Democratic Senator Elizabeth Warren said Senate Republican leader Mitch McConnell “caved” and declared a short-term deal to raise the debt ceiling into December a win for Democrats. The offer alleviated concern over an imminent default, but it also kept investors befuddled as to where a possible new drop-dead date lies on the curve.

“From a political perspective, the only thing less attractive than voting to raise the debt limit to $31 trillion is voting to raise it to $29 trillion and then voting a second time to raise it to $31 trillion,” Goldman Sachs economist Alec Phillips wrote in a note, adding that it shouldn’t be interpreted as a compromise and it might not change the situation.

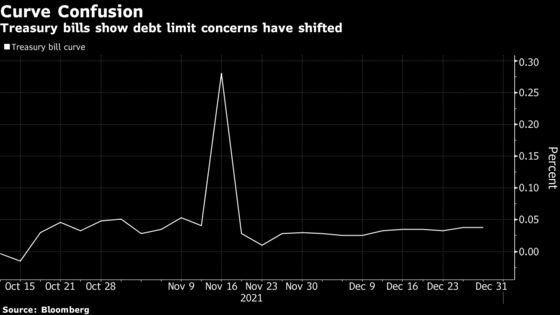

The yield on the Oct. 21 maturity, which earlier traded around 0.16%, dropped by as much as 9.75 basis points to 0.03%. Investors are struggling to reprice risk now that the so-called x-date has been shifted.

“No one knows what to do with this,” said Jefferies economist Thomas Simons. “The wide markets for bills suggests that there’s a lot of people looking to get out of certain dates, but unable to decode which dates are safer.”

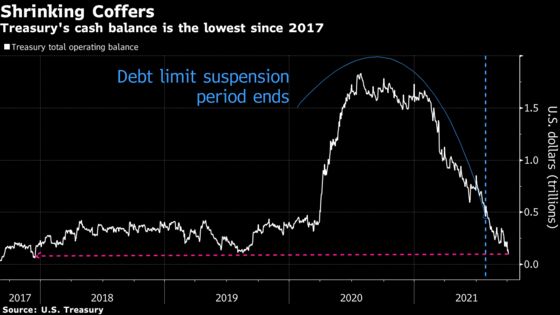

Meanwhile, the Treasury’s cash pile plunged to $99 billion as of Oct. 5, the lowest since December 2017, according to data published Wednesday. Still, a potential December debt-limit deadline now means that the Treasury is unlikely to reach its estimated balance of $800 billion by the end of the year.

Avoiding Bills

If the U.S. runs out of borrowing capacity, debt maturing immediately afterward might not be repaid on time. Investors in those securities are therefore demanding compensation for the risk in the form of higher bill yields.

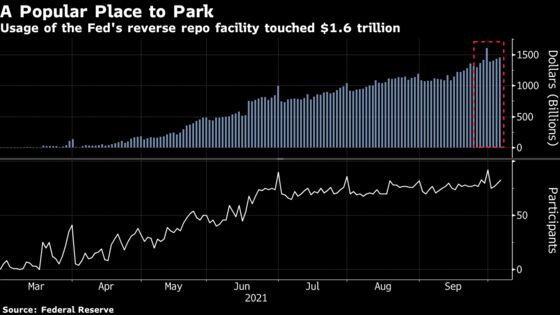

Full Speed Ahead for Reverse Repo

Meanwhile, investors in need of an alternative to certain T-bills are flocking to the Federal Reserve’s facility for reverse repurchase agreements. That’s adding to demand created by T-bill supply cuts made in an effort to keep the debt load under the ceiling. Usage of the facility increased to a record high on Thursday.

Smaller Buffer

One of the starkest proxies for debt-ceiling risk is the Treasury’s cash pile. Inflated by fiscal stimulus and Fed asset purchases, the cash balance exploded to a record $1.83 trillion in July 2020, but has since dwindled to around $99 billion, the smallest since December 2017. A large part of that drawdown was mandated by the reinstatement of the debt ceiling at the start of August. But the pile is now well below what the Treasury itself had forecast for the end of the third quarter. The upshot is that the government has less of a buffer to pay its bills if there’s a disruption in debt markets.

Meanwhile, the department said in a statement Friday that around $173 billion of headroom remained as of Sept. 29 under extraordinary measures that have been put in place to avoid the government breaching its debt ceiling, assuming the Debt Issuance Suspension Period ends on Oct. 18.

©2021 Bloomberg L.P.