Swedish Krona, Worst Major Currency This Year, Can't Get a Break

Sweden's Krona Slumps Most in Eight Months After Inflation Slows

(Bloomberg) -- The world’s worst-performing major currency has no respite in sight.

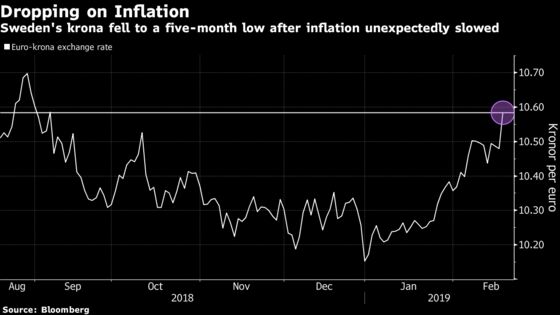

Sweden’s krona slumped the most in eight months after weaker-than-forecast inflation data stoked concern about the central bank’s ability to raise borrowing costs.

The latest numbers add to investor skepticism on the outlook for the krona, which is ironically forecast to return the most among the Group-of-10 exchange rates this year. The currency had its worst January since 1993 after retail sales and consumer confidence slumped in Scandinavia’s biggest economy.

The currency snapped two days of gains on Tuesday after consumer prices fell 1 percent in January from a month earlier, missing even the lowest estimate in a Bloomberg survey that forecast a decline of 0.7 percent.

“The last couple of months has showed that investors are somewhat reluctant to buy SEK, and this figure doesn’t change the negative sentiment,” said Kiran Sakaria, a strategist at Handelsbanken AB in Stockholm. “We expect inflation will pick up somewhat during the first half of 2019, and if we’re right that will lead to the markets pricing a higher probability of a rate hike this autumn and we will probably see a gradual strengthening of the krona.”

The krona weakened as much as 1.1 percent, the most since June, to trade at 10.5947 per euro. It has slumped about 4 percent this year. The krona and the Swiss franc are the only major exchange rates to have declined against the common currency so far in 2019.

Despite Tuesday’s inflation print, it is too early to call the Riksbank’s plans into question as policy makers will await more data, according to Credit Agricole SA. The central bank still has time to decide since investors have penciled in the next rate increase in only the second half of this year, said Manuel Oliveri, a strategist.

Markets may also be looking for any clues from a speech by Riksbank Governor Stefan Ingves later today, he said.

“He is quite likely to reassure the market about the base case,” London-based Oliveri said. “We may even see a reversal lower in euro-krona towards the end of the day.”

Below is a selection of analyst views:

BBVA SA

- Looking beyond the near-term knock-on of the miss in inflation, the krona sell-off still appears a bit overdone, said strategist Alexandre Dolci.

- January’s CPIF downturn was largely caused by larger-than-normal price discounts in highly seasonal items in ultra-competitive markets, and such offers could swiftly reverse in the following months.

- The decline has to be put in the perspective of cooler inflationary pressures in most developed economies.

- As a result, it would require a sharper and longer CPIF downturn to call into question the Riksbank’s assessment, while the next rate hike isn’t expected until 2H19.

- “As we do not see recent developments being sufficient to force the Riksbank to change track yet, the krona should in turn benefit from the tightening stance kept by its own central bank this year, and we would look to short EUR/SEK in any overshooting above 10.60.”

Nordea Abp

- The broad decline in price pressures is bad news for Riksbank and adds to the risk of a downward revision of the rate path in April, alongside potential news on the pre-reinvestment of the December 2020 bond maturity, said strategist Andreas Steno Larsen.

- Apart from that short-term correction probability, the krona outlook is getting more and more worrisome by the week currently.

- In case the Riksbank decides to fully pre-reinvest the December 2020 bond maturity at its April meeting, a 10.75-11.00 range shouldn’t be ruled out in EUR/SEK later in 2019.

- It could, however, make sense to re-sell EUR/SEK up here in anticipation of a positive correction in SEK ahead of the bond maturing on the Riksbank balance sheet on March 12.

Danske Bank

- The inflation data was disastrous and it’s hard to find an argument for the krona to rebound versus the euro right now, other than it looks oversold versus the short-term models, said analyst Stefan Mellin.

- “We still not see a hike this year, but realize that there should still be a certain hike premium.”

- The next key data point is 4Q GDP next week, which could be another blow to the Riksbank; Danske Bank’s preliminary estimate is for growth of 1.2% y/y vs the Riksbank’s 1.7%.

To contact the reporter on this story: Love Liman in Stockholm at jliman1@bloomberg.net

To contact the editor responsible for this story: Ven Ram at vram1@bloomberg.net

©2019 Bloomberg L.P.