Blackstone Joins in Risky Commercial-Property CLO Sales Swell

Blackstone Joins in Risky Commercial-Property CLO Sales Swell

(Bloomberg) -- Sales are once again booming for a growing corner of the bond market used to finance risky real estate properties in transition despite a performance slump threatening some prior deals.

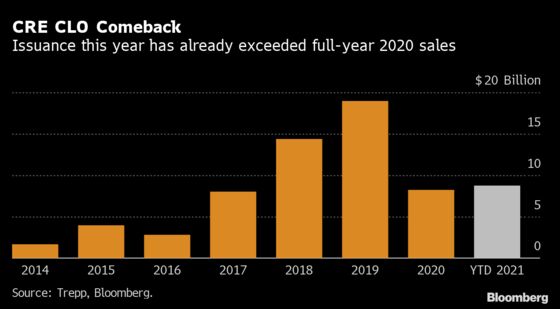

Known as commercial real estate collateralized loan obligations, the complex bonds are a niche financing tool dusted off from before the Great Financial Crisis. After issuance plummeted more than 50% in 2020 as coronavirus restrictions mushroomed, this year’s pace has doubled that of the same period in 2019, the sector’s best post-crisis year.

A variety of Wall Street firms are now rushing to the market to get in on growing investor demand for the product, which offers higher yield than many other bonds and benefits from an expected economic recovery. This week, Blackstone is marketing a $1 billion CRE CLO, and companies such as TPG Capital, Ready Capital Corp. and Benefit Street Partners are among those that accessed the market in March.

Sales of approximately $9 billion through April 8 are already double the pace for the same period in 2019, according to data compiled by Bloomberg, when annual sales reached a post-crisis record of about $19 billion. With a hunt for higher yields this year, growing demand for floating-rate, shorter-duration paper amid the potential for rising rates and increased interest in distressed commercial real estate, the market has had a strong resurgence.

The properties packaged into CRE CLOs don’t qualify for inclusion in more traditional property financings, such as commercial mortgage-backed securities, because they are being refurbished or are otherwise in a state of transition. Projects may include an empty office tower undergoing renovations and waiting for new tenants or a suburban mall being retrofitted and may offer yields as much as the high single digits.

“CRE CLO issuance has exceeded all expectations, resulting in spreads recently increasing,” Cantor Fitzgerald LP analysts led by Darrell Wheeler said in a research note this week. But “collateral performance has started to show some delinquency in older CLOs that had retail and hotel loan exposures that were more than 20% of the initial collateral balance.”

In some transactions from 2018 and 2019, “the delinquency percentage can be large,” Wheeler said, but frequently only involves a few loans in the pool. More than 50% of the loans contained in the deals successfully refinance but if the few troubled loans remain in the pools, Wheeler says that certain compliance tests may be tripped causing cash to be diverted from investors of lower-rated debt to senior-tranche holders.

The overall delinquency rate of CRE CLOs climbed to 2.63% in January, the most recent data available, up from 0.11% the same period a year ago, according to commercial property data firm Trepp LLC. Lodging and retail are suffering the most with delinquency rates of 10.74% and 6.62%, respectively.

Servicer modifications and forbearance approvals have played a role in keeping a lid on overall rates, according to Trepp. A handful of specific deals heavy on retail and hotel have far higher delinquency rates, according to Cantor Fitzgerald.

Questionable Quality

The quality of the loans going into these structures was already deteriorating before the pandemic as increased competition, new managers with scant track records and more aggressive deal terms began appearing.

Read more: Real-Estate CLOs May Be The Next Shoe to Drop

“The terms of loans going in to CRE CLOs were weak, and so there may have to be some comeuppance,” Dan Zwirn, chief executive officer of Arena Investors, said in an interview this week. In several property sectors, there is a new reality, he said.

“Post-Covid, it’s plain for all to see: in office buildings in dense urban areas, for example, occupancies are lower, rents are lower, and if you dealt with people leasing space, there are enhancements on leases, such as tenant improvements, or they gave some free months or even free years,” Zwirn said.

The fact that bond payments to investors depend on a project’s completion and the willingness of a sponsor to make that happen has some investors worried.

CRE CLO managers often own a large equity piece of the transactions, so usually have an incentive to avoid defaults. But while CRE CLO managers have done what they can -- often buying out a loan from the pool, replacing it, or modifying it -- that approach may not last forever. That means some borrowers may eventually have to face default.

“Patience won’t be infinite on the part of the CRE CLO manager who wants to bring a positive return to the equity she or he owns,” Zwirn said.

Relative Value: Agency MBS

- Goldman Sachs Asset Management remains overweight Ginnie Mae MBS versus Fannie Mae MBS, according to a recent research note

- The expiration of the supplementary leverage ratio (SLR) exemption may result in increased bank demand for Ginnie Maes, thereby providing a marginal tailwind for the sector, analysts said

- Additionally, GSAM expects Ginnie Mae production coupon prepayment rates to moderate. Ginnie Mae production coupons generally benefit into a rate sell-off, given their prepayment function tends to be more sensitive to interest-rate incentive than Fannie Maes

Quotable

Regarding the new bill signed by New York Governor Andrew Cuomo on Tuesday that was developed by the Alternative Reference Rates Committee to facilitate the transition away from Libor:

“The newly enacted New York state legislation will facilitate the transition for legacy Libor contracts governed by New York law to SOFR and mitigate cash flow risks,” said Moody’s analyst Peter Hallenbeck. “Most of U.S. ABS and RMBS Libor-linked notes issued before 2018 are legacy contracts that either have no Libor fallback provision or fallback to a Libor-based rate.”

What’s Next

ABS deals in the queue for next week include CarMax (prime auto), DriveTime (subprime auto), Amur (equipment), Diamond Resorts (timeshare), Byrider (subprime auto), Navient (FFELP student loan), and Toyota Motor Credit (prime auto lease).

©2021 Bloomberg L.P.