Stock Sales at 13-Year Low Signal Waning Appetite for U.S. Shale

Stock Sales at 13-Year Low Signal Waning Appetite for U.S. Shale

(Bloomberg) -- U.S. oil and gas producers have raised the least funds from share sales this year in over a decade, as investors lose their appetite for shale.

Sources of funding are likely to be scarce in 2020 too. While U.S. oil prices have climbed about 33% in 2019, they are still below the $65-$75 a barrel level that analysts say is needed to boost investor confidence in the companies. Industry stock sales plunged about 70% in 2019, and debt issuance was largely flat from a year ago as companies face a wall of maturing bonds.

“It seems to be fairly unloved as a sector,” said Andy Brogan, Global Oil & Gas Sector Leader for Ernst & Young LLP, referring to the energy industry. Next year may prove to “be a continuance of this year,” he said.

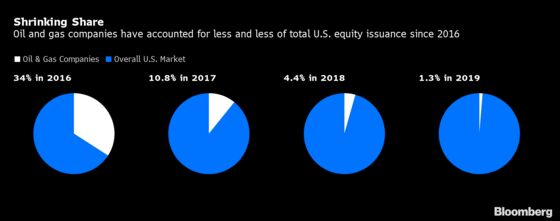

Equity Doldrums

Share issuance from American producers has totaled only $1.3 billion so far in 2019, the lowest since at least 2006, according to data compiled by Bloomberg.

Share sales boomed in 2016 as oil prices recovered from their biggest crash in a generation. Output cuts by OPEC and strong global growth rescued the market, according to CreditSights Inc. analyst Jake Leiby.

Meanwhile, the energy industry’s share of total U.S. equity sales has declined for three consecutive years. It contributed to just over 1% in 2019, compared to 2016’s 34%.

“Few fundamental catalysts will likely emerge in 2020 to sustain sentiment for crude and U.S. oil-exposed E&Ps, as resilient production collides with concerns about a maturing economic cycle,” said Vincent Piazza, a senior analyst at Bloomberg Intelligence.

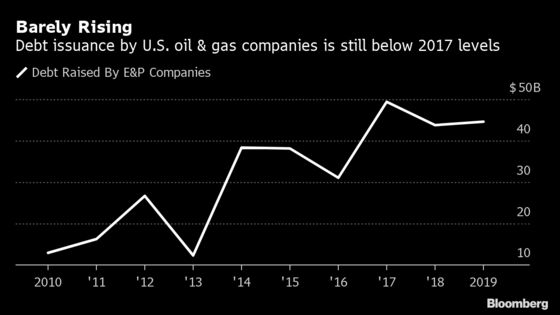

Debt Alarm

Annual bond issuance by U.S. exploration and production companies has totaled about $44.5 billion as the year nears its close, slightly higher than in 2018, though the figures include refinancing of prior debt.

The concern for companies is that, in the coming year, securities due in 2021 and beyond will become current liabilities on the balance sheet. That could push valuations even lower for the already struggling industry.

“The market was OK with extra leverage on the balance sheets when crude was at $75 a barrel, it was the wild west,” said Spencer Cutter, a credit analyst at Bloomberg Intelligence. If oil goes back below $50 a barrel, banks may start cutting borrowing bases, he said.

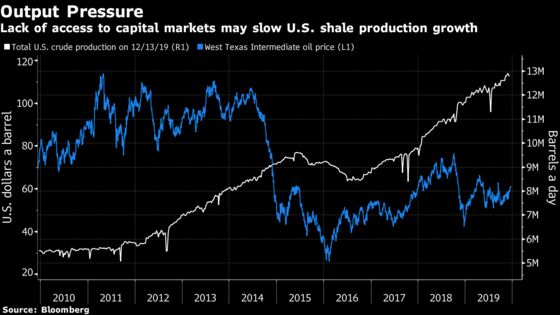

Output Pressure

The lack of access to capital markets is expected to force companies to show restraint on production. That’s at a time when operators in the Permian Basin will have to drill “substantially more” wells to maintain current output, according to IHS Markit. The industry researcher says the rate at which well output decreases with age -- known as the base decline -- is rising in the region.

“Poor financial performance, excess leverage and an increased focus on emissions have pushed the cost of capital of shale oil producers sharply higher,” Goldman Sachs Group Inc. said in a note earlier this month.

Unlike earlier in the decade, when lower oil prices forced U.S. shale producers to limit production, the pressure to curb output is now coming from equity and debt markets, according to the bank.

--With assistance from Allison McNeely, Rick Green, Crystal Kim and David Wethe.

To contact the reporter on this story: Kriti Gupta in New York at kgupta129@bloomberg.net

To contact the editors responsible for this story: Simon Casey at scasey4@bloomberg.net, Pratish Narayanan

©2019 Bloomberg L.P.