Stock Pickers’ Faang Addiction Delivers a Harsh Blow to Workers

Stock Pickers’ Faang Addiction Delivers a Harsh Blow to Workers

(Bloomberg) -- At least in the stock market’s cold-blooded logic, 2020 will be remembered as the year when people became superfluous to the cause of progress.

To recap, at a time when the pandemic put 22 million Americans out of work, equity prices nevertheless rose by $5 trillion, thanks to gains in automated tech titans optimized for lockdown commerce. The situation became a symbol for inequality in the virus age, as money flowed to the rich and the poor got hunger and hardship.

While economists say there may be a reprieve -- their consensus is for unemployment to fall back to 5% by 2022 -- evidence is mounting that the stay-at-home trade and the insecurity it bespeaks will be harder than that to root out. Among it are signs that market forces are convincing corporate managers to shelve Old Economy business investment and plow money into intellectual property.

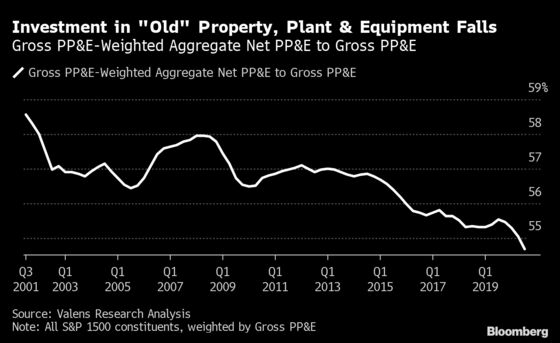

“Companies have been more and more shutting their spending on capex off and accelerating their investment in R&D,” said Rob Spivey, director of research at Valens Research, a boutique investment research firm that focuses on accounting analytics. “They’re focusing more on intangible assets as opposed to tangible assets, so if you’re not looking at that, you’re really missing the picture.”

One fact that should sow concern at the end of any recession is that keeping a lean workforce is a time-honored way of driving profit growth. But for anyone counting on jobs to roar back as vaccinations proliferate, a subtler threat lies in the nature of the lockdown itself, a period when companies were rewarded grandly for figuring out ways of minimizing the role of humans.

The market’s invisible hand can be seen guiding corporate decisions in real time. While growth in investment in plants, property and equipment slows among S&P 1500 companies, Valens estimates that spending on intangibles will rise 13.9% this year, up almost five percentage points from what’s been typical over the last 10 years. (The firm uses research and development outlays as a proxy.)

While the market isn’t the economy, it’s a system for rewarding innovation, conditioning corporate managers to its tastes. This year, those tastes have been for asset-light businesses in which automation and online commerce shoulder profits while labor-intensive models are left behind. When similar alignments took hold in the past, the tidings for the labor market were poor.

Throughout history, economic recoveries heavy on intangible investments have been associated with slower labor market bounce-backs -- in some cases twice as slow. Starting in the early 80s, when it took fewer than 30 months for employment to return to its prior peak, the recovery has gotten progressively longer: to 50 months following the dot-com bust, to 70 following the global financial crisis, data from Carlyle Group show. In each case, growth in outlays for intangibles expanded.

Nothing has defined the 2020 market more than the erosion in the value of human capital. Over 10 months of chaotic swings, companies whose profits rely least on people to generate beat those that depend the most by 27 percentage points, according to an analysis by StoneX Group Inc.’s Vincent Deluard, director of global macro strategy at the firm.

As a result, in a year when the S&P 500 is up 16%, rallies in Facebook Inc., Apple Inc., Amazon.com Inc., Netflix Inc., Alphabet Inc., and Microsoft Corp. average three times as much.

People hoping for a broadening distribution of the stock market’s bounty got signs of it starting in November, when progress on vaccines spurred gains in beaten-down sectors, loosely defined as the “value rotation.” The S&P 500’s best-performing industries since the end of October are banks and energy producers, industries that were down 23% and 54% in 2020 when their rebound began.

Drilling down, however, shows the recovery is somewhat less than meets the eye. Value’s recent outperformance can actually be traced to just “four ‘good news’ days,” including Covid vaccine announcements and Janet Yellen’s selection as Treasury secretary, according to Jonathan Golub, Credit Suisse’s chief U.S. equity strategist. Since reports of Yellen’s appointment, value has lagged 70% of the time, he estimates. Over the last month, information technology is still the best performing S&P 500 sector, up 6%.

Analysts are yet again expecting earnings for technology companies to get a boost. Profit expectations for the S&P 500 Information Technology Index have been rising steadily since October, contrary to a decline for every other sector. Earlier this month, analysts upped their EPS growth projections for the sector by 4% from one week to the next, matching the biggest ever jump in 2021 growth expectations for the sector.

Jessica Rabe and Nicholas Colas, co-founders of DataTrek Research, scoured industry predictions from top consulting companies and found a common theme: an expectation that the trend to automation, digitization and remote work will stick. One of advisory firm Gartner’s top predictions is that by 2025, customers will be the first people to touch more than 20% of products around the globe, as factories and farms continue to be automated.

“Even with the expectation of vaccines being widely distributed next year, top industry consultants don’t see the trend to virtual or remote work, education, doctor visits and experiences slowing down,” wrote Rabe and Colas. “Automation will continue to dominate as a theme in the coming years as well.”

©2020 Bloomberg L.P.