Trade War Threatens Peace Dividend for Stocks

Stock Market Valuation Goes Back on War Footing

(Bloomberg Opinion) -- The Cold War had a chilling effect on the market for decades. The trade war with China and intensifying tensions with Mexico threaten to do the same.

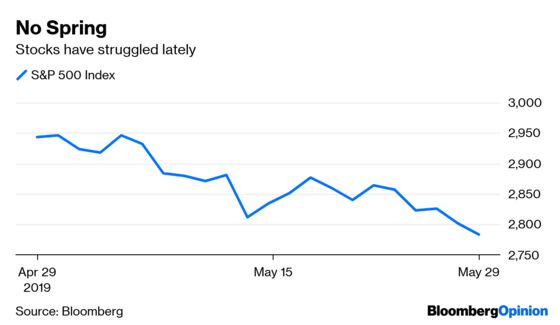

Stocks have been slumping this month, with the S&P 500 Index down more than 5%. There are, of course, many reasons for investors to be wary, from the trade war to sinking bond yields. But what is confounding still-bullish investors is that even given all that, stocks may still be a buy. In fact, except for a brief period at the end of last year, the market is the cheapest it has been in years. And this comes when interest rates look more and more likely to remain low, which often elevates multiples, and corporate profit growth is expected to rebound after a two-quarter lull.

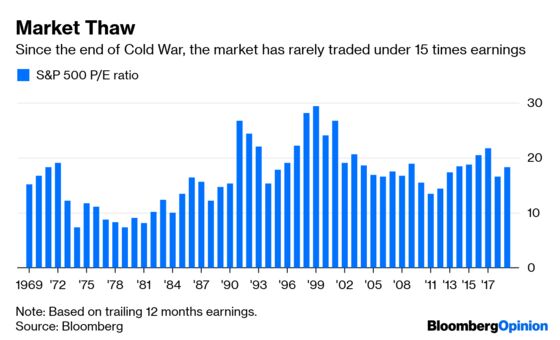

The average stock in the S&P 500 is now trading at just over 18.2 times the trailing 12 months of profit. That’s below the 19 that stocks bottomed at in February 2018. It is also below the nearly 20 times earnings that stocks traded at just before Donald Trump was elected president. During the past five years, the S&P 500 has had an average P/E ratio of just over 19, which is about 6% higher than it is now. It is still higher than the 17.6 P/E that the S&P 500 averaged over the past decade, but that includes the aftermath of the financial crisis.

Stocks didn’t always trade this high. Bloomberg’s data on P/E ratios only goes back to the late 1960s. But Robert Shiller, the Nobel Prize-winning economist at Yale, has collected data back to 1871. For the first hundred years, the average P/E of the stock market rarely rose above 18. In fact, through the end of 1990, the average P/E of the market was just 13.6. Then something changed.

Starting in 1991, the market’s P/E multiple took off. Since then, it has rarely been below 18. It averaged 23 in the 1990s and 19.5 in the 2000s.

Many factors probably contributed to the market’s valuation shift, but one of the most frequently cited is the so-called peace dividend. The Berlin Wall fell, the Soviet Union collapsed in late 1991, and stocks took off. It’s hard to quantify just how much of a boost came from the downfall of a military superpower and the reduced threat of nuclear war. Interest rates also generally fell to new lows during the period; technology and productivity took off; and 401(k)s blossomed along with many Americans’ attachment to the stock market. But a big lift undoubtedly came from a reshuffling of the world order with the United States firmly on top.

Now investors are exchanging the end of the Cold War with the warming of a different one with another type of nascent superpower. It seems clear that the intensifying trade war with China won’t be over quickly or won easily. Both countries are far from resolving the intellectual property issue that is the biggest sticking issue for American companies, and one the president after Trump will most likely still be dealing with. The long-term plan of the Chinese government is to overtake the United States as the largest economic power in the world. That will create more and more tension. Speaking of tension, as of Thursday night Trump threatened to open a second front in the trade war by imposing tariffs on Mexico beginning June 10 unless it stops the flow of migrants into the U.S.

All that is worth noting when looking at the current stock market multiple. For 40 years, from 1950 to 1990, the market multiple for the S&P 500 averaged just 13.5. Based on that, 18 doesn’t look so cheap.

To contact the editor responsible for this story: Daniel Niemi at

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.