Stock Hedges Are Slow to Return as Traders Let Their Winners Run

Stock Hedges Are Slow to Return as Traders Let Their Winners Run

(Bloomberg) -- Equity traders were more than happy to cash out option hedges as stocks plunged in December. Now that the market is back in rally mode, they’re hesitating to build them back up.

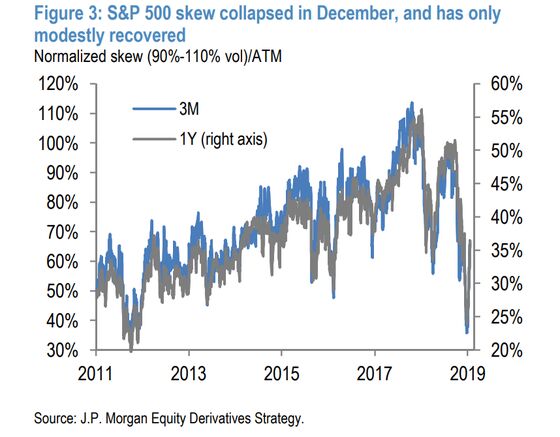

While the S&P 500 bull run is halfway back from its near-death experience before Christmas, demand for contracts that protect against losses in individual companies is rebounding at a slower rate. Options skew, a relative price measure that goes up as dealers find buyers for insurance, “has only modestly recovered,” and remains stuck in its lowest historical range, according to strategists at JPMorgan Chase & Co. led by Bram Kaplan and Shawn Quigg.

While several interpretations exist, the slow reconstruction of equity hedges is another sign of how shocked markets got in the fourth-quarter downdraft, which erased $5 trillion from U.S. equity values.

“Should we see a continuation of the market recovery and equity inflows, skew is likely to continue to steepen as these structural option flows continue to return,” the strategists wrote in a report Tuesday. “As the market recovered and volatility subsided, option flows began moving back toward their more typical patterns (i.e. increased put/hedging demand, increased call supply via overwriting and collar programs)."

Volatility watchers had become concerned toward the end of 2018, when, for instance, the S&P 500 put/call open interest ratio dropped -- the apparent lack of demand for put options potentially implying that investors weren’t protecting themselves from further market declines. The VVIX, which measures volatility of the fear gauge, on Jan. 2 fell to its lowest level in 17 months.

“For all the talk of bear markets and imminent recession, S&P vol markets are pricing in very little downside risk,” strategist Mandy Xu said in a note Jan. 7.

Indicators that would typically rise with greater demand for hedges against unusually large market moves hit multiyear lows late last year; S&P 500 one-month 10-delta versus 50-delta volatility, for instance, reached its lowest levels since early 2016.

The JPMorgan strategists said on Nov. 26 that these things weren’t signs of complacency, but rather typical behavior by investors during a market correction. They echoed that in the Tuesday note.

“During the market correction we saw investors selling cash equities (which reduces put demand as there is less exposure to hedge), substitution of short futures for puts to hedge further downside, increased call demand to hedge right tail risk from being underweight or short equities, and hedge monetization,” Kaplan wrote.

While volatility still has a way to go to return to normal, it appears to be heading in that direction.

Volatility “looks less cheap now,” Wells Fargo & Co. derivatives strategist Pravit Chintawongvanich wrote in a note Thursday. He sees put spreads, such as a Feb. $158/$150 spread on the Invesco QQQ Trust Series 1 exchange-traded fund, as a good way to implement hedges in the current environment.

To contact the reporter on this story: Joanna Ossinger in Singapore at jossinger@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Chris Nagi, Richard Richtmyer

©2019 Bloomberg L.P.