Stock Gains Mask Looming Credit Meltdown, SocGen’s Edwards Says

Stock Gains Mask Looming Credit Meltdown, SocGen’s Edwards Says

(Bloomberg) -- Record highs in equities are masking excesses in the corporate credit market and a reckoning is coming, according to Societe Generale SA global strategist Albert Edwards.

“It’s the quantity of corporate debt which is off the scale, as well as its low quality,” Edwards, who is a longtime market bear, said in an interview. “Monetary largess has been so incredible and that’s where the apex of the next crisis will be,” he said, adding that it’s “a shame, because that’s where the retail money has gone into.”

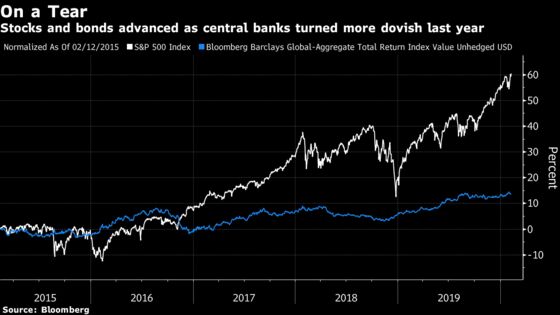

Under normal circumstances, weakness in economic data would hurt equity markets, in turn leading to credit downgrades because ratings companies incorporate stock prices into their models, Edwards said. But that hasn’t happened in the last few years because central banks have repeatedly intervened to prop up markets, he said.

For instance, U.S. manufacturing data hit a weak spot in the second half of last year, Edwards noted -- but instead of hurting stocks, the weakness coincided with equities reaching fresh highs. He doesn’t think it will end well, particularly for individual investors.

“For virtually this entire economic cycle, the retail money has been pouring into bond mutual funds and not equities,” Edwards said, adding that investors are still chasing risk assets, but have preferred corporate bonds and technology stocks.

Edwards isn’t alone in sounding the alarm about the situation, after a record year for flows into fixed income mutual funds and ETFs. Last month, Federal Reserve Bank of Boston President Eric Rosengren warned that financial asset bubbles pose a risk to stability amid a “reach for yield” by investors as a result of continued accommodative monetary policy. Surging corporate debt was identified as a key vulnerability in the International Monetary Fund’s October Global Financial Stability Report.

To be sure, many investors are more optimistic, expecting modest economic growth and accomodative policy from the Federal Reserve and other major central banks to support the outlook for credit in 2020. Average spreads on U.S. investment-grade corporate bonds are back to where they started this year, which isn’t too far off post-global financial crisis lows, following a raft of solid company earnings recently.

Read more about terminal functions to track the debt binge by U.S. blue chip corporations

“Retail investors believe there is limited downside to investment grade,” Edwards said. “They will be shocked by how bad the out-turn is because of the high level of corporate defaults and bankruptcies in the next recession.”

To contact the reporter on this story: Gregor Stuart Hunter in Hong Kong at ghunter21@bloomberg.net

To contact the editors responsible for this story: Christopher Anstey at canstey@bloomberg.net, Joanna Ossinger, Finbarr Flynn

©2020 Bloomberg L.P.