Stock Bulls Get Reprieve as Powell Signals a Limit to Austerity

Stock Bulls Get Reprieve as Powell Signals a Limit to Austerity

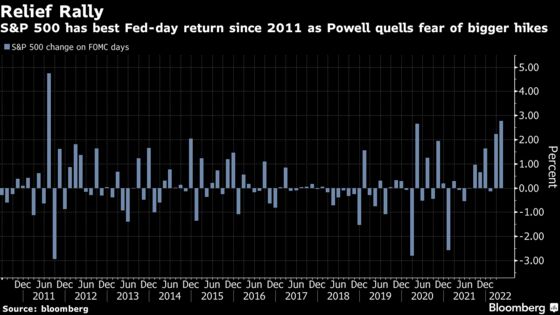

(Bloomberg) -- Under no pressure to throw investors a bone, Jerome Powell nevertheless did, igniting the biggest stock market rally on the day of a Federal Reserve meeting in a decade.

All it took was a few phrases in a day otherwise rife with hawkish pronouncements from a central bank bent on subduing the hottest inflation in 40 years. While stocks initially wobbled on confirmation the Fed had pushed up interest rates by 50 basis points, the S&P 500 took off when Powell said an even bigger increase is “not something that the committee is actively considering” for coming meetings.

For stock bulls, if the response wasn’t overtly dovish, it was at least interpretable as setting a limit -- for now -- on how much hawkishness central bankers see the need for in combating spiraling prices in the economy. Such signaling has been in short supply of late and was not lost on equity traders, who bid up the S&P 500 to its best post-Fed reaction since 2011, according to data compiled by Bloomberg. When stacked against days when rates were hiked, Wednesday’s gain in the S&P 500 was the largest since at least 1990.

“Taking out a left tail risk is the best bone a market can get right now,” said Max Gokhman, chief investment officer for AlphaTrAI. “Hence the S&P is jumping like a pleased puppy.”

The technology-heavy Nasdaq 100 rallied as Treasury yields sunk, with rates on benchmark 10-year notes briefly slipping below 2.9%. The Bloomberg Dollar Index slid 0.9%.

Market sentiment may also have gotten a boost when Powell said policy makers consider the fed funds rate that is neutral for the economy to be between 2% and 3% -- within the scope of expected hikes this year at least. Few market participants expect the central bank to stop there, though some bulls may have emboldened by the fact the Fed chair didn’t specify a higher threshold.

To be sure, most of the Fed statement and subsequent press conference was spent establishing the terms of what is sure to be a protracted fight against inflation. Powell stressed that while the economy and labor market are strong, “inflation is much too high,” and that the Fed will deliver a series of 50-basis point increases, starting with today’s move. But it could’ve been worse, according to Oppenheimer & Co.’s Alon Rosin.

“They jawboned the market down ahead and got what they wanted. The whole Street, especially retail, has been de-leveraging amid margin calls and rough performance,” said Rosin, the firm’s head of institutional equity derivatives. “The Fed is not looking to ‘crush’ the market today on the event. They’re basically saying 50 basis points at each meeting, not more or less. It’s one BIG relief.”

A look at the past few months of performance might explain why Powell didn’t keep alive the threat of a 75-basis point hike, something not seen since the 1990s. Even with Wednesday’s jump, the S&P 500 is 10% lower this year, while the Nasdaq 100 is nursing losses of roughly 18%. Yields on 10-year Treasuries are currently trading near 2.90%, after entering 2022 at 1.50%.

Taken together, that’s pushed financial conditions -- a multi-input measure of stress across asset classes -- to near the tightest levels since 2018, excluding the 2020 coronavirus shock.

While repeatedly stressing that the Fed is committed to fighting the hottest inflation in nearly four decades, Powell also mentioned that there’s some evidence that the personal consumption expenditures index -- the Fed’s preferred gauge of price pressures -- is starting to peak. Once inflation does start to come down, the Fed will return to hiking by 25 basis points per meeting, he signaled.

That suggests that markets are recalibrating what now looks to have been overly hawkish expectations for the path of Fed policy, according to Steve Chiavarone of Federated Hermes. Bond traders are paring bets on expected tightening in June. But still, the Fed wasn’t close to dovish.

“A rally in Treasuries here and a rally in equities there may just be more about expectations that got ahead of themselves rather than any dovish surprise,” Chiavarone, senior portfolio manager at Federated Hermes, said by telephone. “This was a hawkish meeting with a hawkish result and a hawkish outlook, but just maybe not quite as hawkish as some folks feared.”

©2022 Bloomberg L.P.