Junk-Rated Pandemic Winners Brace for a Return to Normal

Junk-Rated Pandemic Winners Brace for a Return to Normal

(Bloomberg) -- European junk-rated companies that gained from people staying home during the pandemic are set for a reckoning as normalcy starts to return.

French supermarket group Casino Guichard Perrachon SA, its Spanish peer Distribuidora Internacional de Alimentacion SA, Dutch-registered maker of plastic garden furniture Keter Group BV, German packaging company Kloeckner Pentaplast and France’s shipping giant CMA CGM are among high-yield corporate borrowers that improved their debt profiles during the pandemic.

“Some of these companies accessed the debt markets after showing robust results, others after selling assets,” said Benjamin Sabahi, head of credit research at Spread Research. “The question is what will happen once the bullish primary-market trend we’ve seen since the first news of efficient vaccines comes to an end, and how will normal results post-Covid 19 look.”

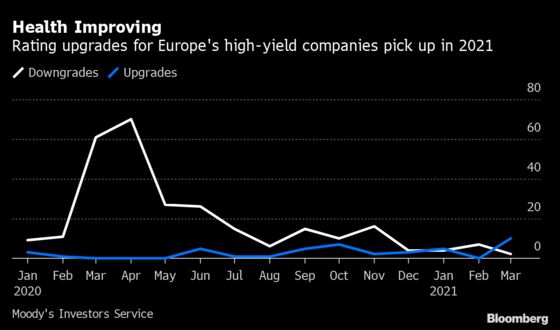

Markets sloshing in liquidity, together with ultra-low interest rates and an upbeat outlook after vaccine rollouts have made high-yield bonds an attractive asset class for yield-hungry investors willing to take on more risk. But when governments and central banks start easing off the emergency support that fueled a 14-month global debt binge, the era of cheap-money may come to an end, raising questions about whether high-risk issuers did enough during the pandemic to put their houses in order.

While even companies without debt pressures that benefited from people being stuck at home, like Netflix Inc., home-gym equipment firm Peloton Inc. and Delivery Hero SE, will need to work out their return-to-normal strategies, for the heavily indebted ones, the challenge could be steeper.

Take Casino Guichard Perrachon, for instance. The parent company of Casino supermarkets and online retailer Cdiscount, which was in a deep restructuring at the onset of the pandemic, saw food and online sales jump as restaurants and non-essential stores shut down. It sold assets and cut debt by 1 billion euros ($1.2 billion), while also tapping credit markets twice in the past six months to refinance borrowings. For all that, Casino may not be where it needs to be as normalcy returns, making asset disposals critical, said Charles Allen, a Bloomberg Intelligence senior analyst.

Grocery Boom

“Casino seems to have gained less in food than most of its supermarket peers during the pandemic,” Allen said. “It has also lagged because it hasn’t put as much focus on ‘drives,’ like online click & collect, as almost all competitors.” The company declined to comment. On Thursday, Casino announced that it is extending an alliance with Amazon.com Inc. to offer a click-and-collect service in France.

Like Casino, Spain’s DIA was also restructuring at the onset of the pandemic. The stockpiling effect in the early days of the first lockdown in March 2020 and strong demand during the rest of the year boosted sales, helping it refinance debt. DIA wouldn’t have been able to ride the surge in demand if it hadn’t put its turnaround plan in place the previous year, a spokeswoman said. Like-for-like sales jumped in 2020 and the company managed to cut losses by 54%.

Still, “defending domestic market share may be tougher if normal shopping patterns resume,” Bloomberg Intelligence analyst Conroy Gaynor wrote in a note on May 13. Like-for-like sales fell 0.4% in the quarter ended March.

Keter Group, based in Israel, is another company whose fortunes were turned by the pandemic. The debt-burdened maker of plastic garden furniture registered revenue gains last year. Its credit rating was upgraded out of the triple-C category and term loans -- marked at around 70 cents on the euro in April 2020 -- are now close to face value again.

Keter Chief Executive Officer Alejandro Pena said the company’s sales boost “positions us well for future growth.” Giuliana Cirrincione, an analyst at ratings firm Moody’s, concurs -- up to a point. Keter will “continue to benefit from efficiency gains” from measures put in place before the pandemic, like a focus on e-commerce and better inventory controls, she said. Still, she cautioned that Keter faces challenges inherent to its business profile, like earnings volatility from input-cost fluctuations.

At Germany’s Kloeckner Pentaplast, the pandemic brought gains. Demand for plastic packaging for pharma and health products and lower raw material costs in some quarters, buoyed earnings 29% in 2020. And while supply bottlenecks and higher raw-material prices hurt first-quarter results, Kloeckner expects to meet its guidance of 6% earnings increase for the year.

The company, whose payment-in-kind notes traded as low as 35 cents on the euro in December 2018 and were exchanged with a discount of at least 40% during 2019, managed to cap costs by refinancing debt in February at more attractive prices.

“The refinancing stabilized the capital structure, addressed upcoming maturities, and going forward it should be able to capitalize on demand recovery,” said Maria Maslovsky, a senior analyst at Moody’s.

Future Stress

Meanwhile, French shipping giant CMA CGM, whose bonds traded at a discount at the back-end of 2019, refinanced 525 million euros of borrowings in October and cut some of its debt pile.

The world’s third-largest container company is riding the boom in online sales of goods, which has boosted shipping rates. In March, S&P bumped up its rating by a notch to BB-, or three steps below investment grade. While CMA is benefiting from a surge in trade, it remains to be seen if the higher shipping tariffs will last, said Spread Research’s Sabahi.

Like for CMA, a return to normal will bring new challenges to scores of pandemic winners. Question is, are they ready for it?

“The difficulty from here is to identify future credit stress,” said Olivier Monnoyeur, high-yield portfolio manager at BNP Paribas Asset Management. “Investors have factored in stronger growth, so it’s hard to see what breaks the market. Until we have seen how well companies and sectors capture that growth, almost everyone gets a free pass.”

©2021 Bloomberg L.P.