StanChart Makes the Right Billion-Dollar Move

StanChart Makes the Right Billion-Dollar Move

(Bloomberg Opinion) -- Standard Chartered Plc Chief Executive Officer Bill Winters is going make a lot of shareholders, including its largest stockholder Temasek Holdings Pte, very happy.

Having paid out a $1 billion fine for violating Iran sanctions, the bank had cleared the decks for buybacks to cheer disgruntled shareholders and boost its return on tangible equity. On Tuesday, the bank delivered. It announced a plan to buy back as much as $1 billion of its shares in its first such move in more than two decades. Winters’ choice to return capital rather than focus on growth is sound: Growth has never been so hard to come by in Asia as a bevy of local banks and homegrown fintech companies provide fierce competition.

With the new buybacks, StanChart is on its way to meeting its goal of a 10 percent return by 2021. The lender posted a first-quarter return on tangible equity of 9.6 percent versus 5.1 percent at the end of 2018.

Even costs seem to be under control with first-quarter expenses down 2 percent over the year at $2.4 billion. The plan to cut $700 million in costs in the next three years and restructure low-return operations in India, Indonesia, South Korea and the United Arab Emirates appears to be on track.

Growth is another story. StanChart said “less buoyant” conditions led it to post a 2 percent drop in revenue for the first quarter at $3.8 billion. While reversing the decline is possible, big gains in sales growth are hard to envision. Beyond a digital banking push in Hong Kong -- its single-largest market, accounting for a quarter of operating income last year -- and getting in on China’s Belt and Road bandwagon, StanChart's prospects to boost revenue are dim.

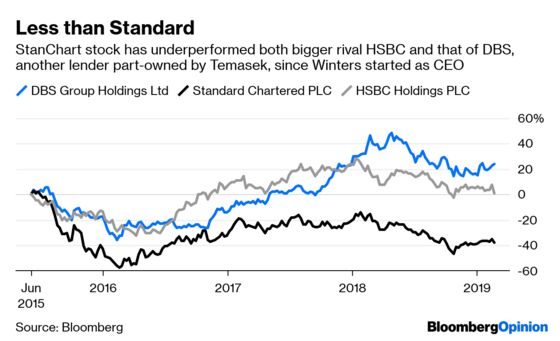

Blame competition. StanChart is often seen as Asia’s No. 2 corporate bank after HSBC Bank Plc. But it competes for that rank with Citigroup Inc., and local players are rising, especially in the dollar business in which StanChart and HSBC have built their names. For instance, more than a third of DBS Group Holdings Ltd.’s deposits were denominated in the U.S. currency last year, up from 26 percent in 2013, according to Bloomberg Intelligence. (Like Standard Chartered, DBS, too, is part owned by Temasek.)

For those reasons, picking capital return over growth is a smart move. Temasek's disappointment with its 16 percent stake in StanChart has been well-publicized. StanChart’s stock has fallen almost 35 percent since Temasek bought its holding in July 2006 and is down almost 40 percent since Winters took over as CEO in mid-2015. Its planned sale of a 46 percent stake in Indonesian lender PT Bank Permata could bring in yet more cash for buybacks. With StanChart now open to the idea, the Singapore state investment firm's bet on the emerging-markets lender may not be as misplaced as it once looked.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.