Sovereign Wealth Funds Love Bonds Now. But Why?

Sovereign Wealth Funds Love Bonds Now. But Why?

(Bloomberg Opinion) -- Sovereign investors command an astounding amount of assets, yet traders typically have only a vague sense of what these behemoths are doing with all that money. Invesco Ltd. has at least one answer: They’re buying bonds.

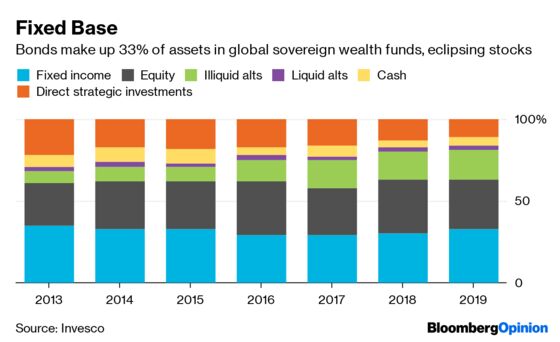

For the first time since 2015, sovereign wealth funds owned more fixed-income assets than equities, according to Invesco’s annual report released Monday. The survey of 68 sovereign funds and 71 central banks, which oversee more than $20 trillion combined, revealed a 33% allocation to bonds among sovereigns, up from 30% in 2018, while the share of equities dropped to 30% from 33%. So far in 2019, both investments have turned a tidy profit — U.S. investment-grade corporate securities, for instance, have gained almost 10%, while the S&P 500 is up more than 18%. Even U.S. Treasuries have earned 5%.

Yet the reason these large sophisticated investors are shifting to fixed income is disappointingly simple. According to Invesco, 89% of those surveyed expect the current economic expansion to end within two years. “Late cycle concerns — both volatility and the prospect of negative returns from equities — have pushed sovereigns towards a more defensive position — supported by improved yields in some fixed-income markets on the back of an increase in U.S. interest rates,” the report said.

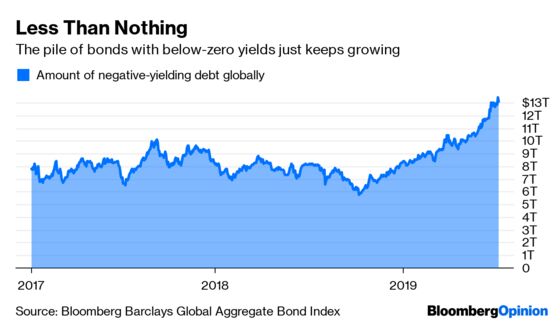

To say there are “improved yields” in this bond market is generous. Benchmark 10-year Treasuries entered 2019 at 2.68%, still well below any sort of historical average, and they’re now hovering close to 2%. U.S. investment-grade credit spreads widened toward the end of the year, but only to the typical level since the recession ended. The only way these interest rates could appeal to long-term investors is if they’re convinced that the U.S. market will soon go the way of Japan’s and Europe’s. The pile of negative-yielding debt across the globe is $13 trillion, more than double the total in October, and spans 10-year government debt in Austria, Denmark, Finland, France, Germany and Sweden, among others.

To be blunt, it’s a bad time to be looking for value in bonds. The rationale among sovereign wealth funds goes to show that the appeal of fixed-income assets now is less about actual fixed income and more about an insurance buffer against a sharp economic decline.

My Bloomberg Opinion colleague Marcus Ashworth demonstrated this “unseemly” yield grab by pointing out that 10-year Greek bonds, which are rated junk, yield about the same as 10-year U.S. Treasuries. “Where does it stop?” he asked. No one really knows, but Invesco’s findings suggest that seemingly permanent low yields aren’t scaring off these big asset managers, which have an average time horizon of 8.5 years.

To be clear, the shift from equities to bonds is relatively minor on a percentage basis. But it’s nonetheless surprising that return-focused managers with long-term mandates aren’t more willing to stick with stocks (or, frankly, anything but low-yielding fixed income) in turbulent times. As I wrote last month, it’s getting hard to take end-of-cycle concerns too seriously when central banks have shown they’ll ride to the rescue time and again.

Without any sort of reasonable yield on bonds, what exactly is the reason for investors to buy them? The fixed payments, after all, have been the chief source of total return over the years. Sure, they have insurance-like properties. And there’s always the “greater fool” theory that someone else will take them at a higher price. The other rationale is that the world is headed toward a deflationary spiral, in which case near-zero yields would provide positive real returns. But that’s a troubling outcome that the Federal Reserve and other central bankers would fight with every available option.

Bloomberg News’s Richard K. Breslow, a former foreign-exchange trader and fund manager, perfectly captured the conundrum in markets today:

The Fed and its peers need to combat the notion that they have no choice but to continue on with business as usual. The perception that we have dug such a toxic hole for ourselves that there is no escape is a real one. The whole world is a “bad bank.” And, ironically, it contributes to the fearlessness with which investors continue to pile into risky assets of all stripes.

I agree, the Fed should push back on demands for a rate cut from the markets (and President Donald Trump). As I wrote last week, thanks to the stronger-than-expected jobs report on July 5, officials now have some cover to keep interest rates steady this month rather than capitulate.

As is often the case, though, there’s a difference between what the Fed should do and what it will do. Mark Grant, chief global strategist for fixed income at B. Riley FBR Inc., predicts it will have little choice but to follow the European Central Bank and Bank of Japan. Grant, who often uses quotes from “Alice in Wonderland” to capture what it’s like investing in a central bank-dominated market, expects yields to fall further, buoying stocks and real estate. “So much money will get forced into them, as so much money gets forced out of bonds,” he wrote.

At least coming into 2019, sovereign wealth funds and their trillions of dollars resisted the temptation to abandon fixed income, preferring to stay “defensive.” But that was before central banks reversed all expectations for raising interest rates and normalizing policy. Janet Yellen once said “I don’t think expansions just die of old age,” with Ben S. Bernanke quipping a few minutes later that “I like to say they get murdered.” The current Fed chair, Jerome Powell, has reiterated that he has an overarching goal of sustaining the current economic expansion, the longest in U.S. history.

Reading between the lines, that means at any hint of serious economic trouble, the Fed will cut interest rates. Time and again, that sort of reassurance has been enough to send risky asset prices higher and bond yields lower. And with every basis-point drop, the case for making money in fixed income gets weaker.

Interviews took place between January and March 2019.

This average excludes central banks.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brian Chappatta is a Bloomberg Opinion columnist covering debt markets. He previously covered bonds for Bloomberg News. He is also a CFA charterholder.

©2019 Bloomberg L.P.