Raising the Retirement Age Won’t Be Easy in South Korea

Raising the Retirement Age Won’t Be Easy in South Korea

(Bloomberg) -- To grapple with a rapidly aging population and the developed world’s highest rate of elderly poverty, South Korea’s officials are talking about raising the retirement age. But a wave of backlash against the idea shows there’s no easy solution to the demographic gloom facing the economy.

South Korea is among countries that seek to protect workers against dismissal until a set retirement age, but concern about old-age poverty has triggered a debate about extending those protections even longer. This month, President Moon Jae-in pledged to work toward extending the retirement age so that the elderly could work longer in full-time jobs.

Some economists say the idea could actually hurt economic growth because it could discourage businesses from hiring younger people. Nam Jae-ryang, a researcher at the Korea Labor Institute in Sejong, South Korea, says most of the benefits would also go to unionized workers who are already relatively better off -- such as employees at big companies like Hyundai Motor Co., or government officials, whose job security is already mocked as “iron rice bowls.”

“The gap between haves and not-haves in the labor market would worsen,” Nam said. “We may see the opposite of what we intended by raising the retirement age.”

The debate about raising the retirement age picked up speed last month when the finance ministry, in a blueprint for tackling the problems of South Korea’s aging society, proposed incentives for companies that keep employees beyond the current retirement age. Demographics is a “significant challenge,” the ministry said.

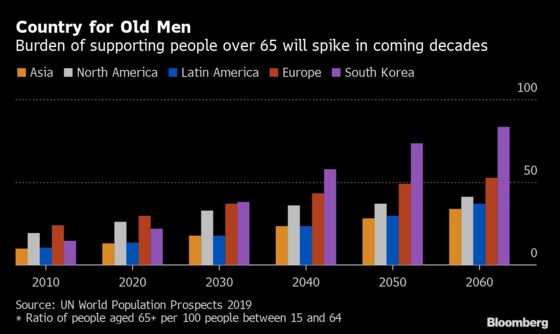

A quarter of South Korea’s population will be 65 or older by 2030, a shrinking work force is already straining the pension system, and the central bank says the decline in working age people will push the economy’s potential growth rate further below the current estimate of 2.5%-2.6%.

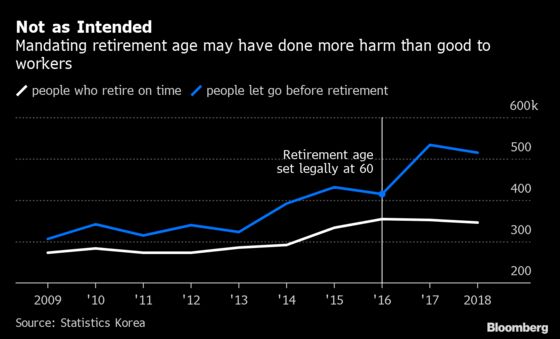

The debate over retirement comes just three years after a law mandated companies to employ workers until 60, and gained momentum after the Supreme Court ruled in February that a person could engage in physical labor until 65. The idea of raising retirement age underscores the urgency felt by the government to economically empower a ballooning elderly cohort. Yet analysts say the measure may end up hurting the jobs market or even the workers themselves, as some say happened after the 2016 law on retirement.

After the law took effect, the number of people quitting before hitting the retirement age rose, according to the statistics office. That’s because rising labor costs gave companies an incentive to pressure employees into leaving before their seniority-based severance packages grew too expensive.

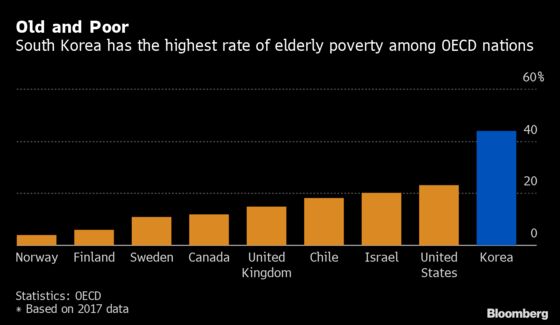

South Korea’s elderly need to work longer for financial reasons. South Korea suffers the worst senior poverty rate among Organization for Economic Cooperation and Development countries, with more than 40% of its people over 65 considered as poor. The lack of social welfare is one reason. The elderly’s pension allowance was just 610,000 won ($515) on average per month as of May 2019, statistics office’s data shows.

Some economists worry delayed retirement worsens overall unemployment by raising labor costs at companies, making them less willing to hire new people. The jobless rate for those aged 15-29 was 10.6% in the second quarter, compared with 4.1% for the overall workforce and 3.1% for those aged 60 and above. The statistics office releases jobs data for September on Oct. 16.

“We’re likely to see more side effects than benefits if the retirement age is raised now,” said Lee Chul-hee, an economics professor at Seoul National University. “It won’t help with elderly poverty and it’ll do little to raise employment.”

To contact the reporter on this story: Sam Kim in Seoul at skim609@bloomberg.net

To contact the editors responsible for this story: Paul Jackson at pjackson53@bloomberg.net, Jiyeun Lee, Jason Clenfield

©2019 Bloomberg L.P.