Stocks Locked In to Credit’s Vortex With Solvency Risk Spreading

Stocks Locked In to Credit’s Vortex With Solvency Risk Spreading

(Bloomberg) -- Massive price jumps. Shaky liquidity. Solvency concern on everyone’s mind. In March 2020, the scariest traits of the equity and credit markets have begun to merge.

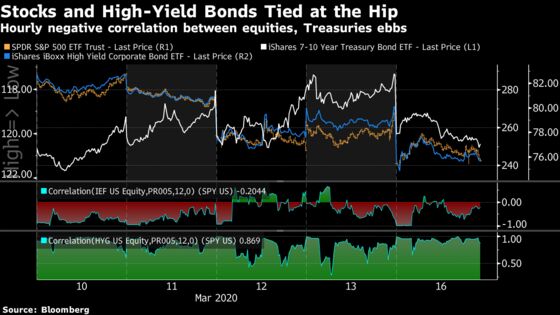

Traditional correlations are fading as lockstep moves between the two assets tighten. Stocks that had once taken their cue from the Treasuries, rising when they fell, have become tied at the hip with a more volatile partner, high-yield corporate bonds. The average hourly correlation -- a gauge of how much the two securities swing in tandem -- has been above 0.8 for equities and junk over the past five sessions, where 1 is lockstep moves. For stocks and government debt, the negative correlation is only -0.4.

The link is visible if you slice the stock market into credit categories. Since the start of the sell-off, the contour of share returns has been dictated by solvency angst. Companies with the highest default risk have fallen 51% since the Feb. 19 top, while those with the lowest risk are down around half that. Within the corporate bond market, safety is the chief input in the sorting process. AAA debt has been modestly positive, and the losses from there are ordered by relative creditworthiness.

“Among assets with an ‘existential’ risk to cash flows, the moves in markets are to send correlations to ‘1,’ as all uncertainty gets maximized at once,” said George Pearkes, global macro strategist at Bespoke Investment Group. “On the other side of the coin, assets which don’t have existential risk can behave in ways driven more by the positioning and liquidity needs of their owners than the fundamental inputs to their valuation.”

A record net 53% of fund managers surveyed by Bank of America said corporate balance sheets are overleveraged. And 61% of respondents want companies to focus on bolstering their balance sheets, the highest share since June 2009.

“One of the chief concerns of investors is the rising risk of a credit event,” said BofA Securities chief investment strategist Michael Hartnett.

Wall Street is of one mind: without stability in credit, any equity rebound won’t endure. Some strategists are calling for the Federal Reserve to reintroduce a facility to aid the commercial paper market to alleviate one facet of funding stress.

“Equities players voice no desire to even think about playing offense until we begin to address credit, corporate cash flows and lending disruptions into an economic shock which is still expanding in scope and scale,” wrote Charlie McElligott, cross-asset macro strategist at Nomura Securities.

“Ideally we would like to see a hard reversal down in both credit and credit derivative spreads to confirm an equity market low,” wrote Brian Reynolds, chief market strategist at Reynolds Strategy LLC. “We have not seen that yet.”

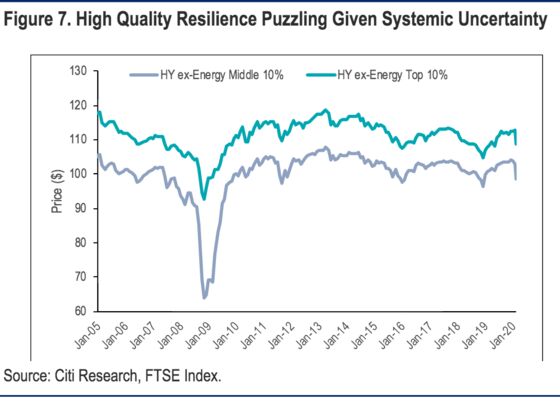

And according to Citigroup, that time might not be arriving soon. Outside of the beaten-down energy space, the top performers –- and more importantly, the middle cohort -- in the junk market are holding up better than they did in February 2016 or December 2016, the trough in previous prolonged sell-offs.

“Relative to those episodes, we believe the recent environment represents a significantly more systemic threat to the credit cycle given growing recessionary concerns,” wrote Michael Anderson, head of U.S. credit strategy at Citigroup. “Therefore we expect lower prices in the current environment.”

It’s a daunting task to cure the many potential credit ailments that may arise. Policy levers may prove ill-equipped given complicated connections between different households and corporations, as well as the extent to which risk has migrated to outside the traditional banking sector, according to his colleague Matt King, global head of credit product strategy.

“Much of the problem is that credit and cash flow streams form long and tangled chains which are only as strong as their weakest link,” he wrote. “With so much credit provided outside the banking system, it is very difficult to implement a system-wide payments freeze which ensures all obligations are simply rolled over.”

©2020 Bloomberg L.P.