SocGen Quants Issue Warning on Stocks Tied to Bond Bull Run

SocGen Quants Sound Warning on Stocks Hitched to Bond Bull Mania

(Bloomberg) -- After this week’s record stock rotation, bonds are flashing a warning for the most crowded trades of this bull market.

Hopes for a coronavirus vaccine are sending the yield on 10-year Treasuries ever closer to 1%, signaling there could be more pain in store for investors in growth and momentum equities.

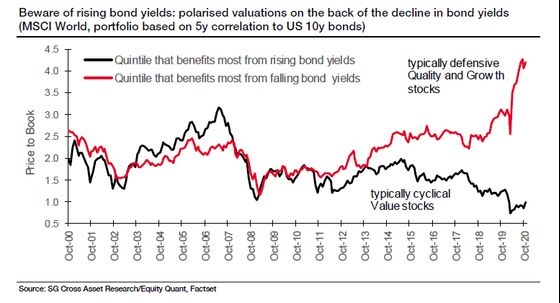

These stocks benefit the most from low rates, and have just been on the losing end of the biggest investing shift in decades. But even after that, the quants at Societe Generale SA reckoned stocks that win from low yields were the priciest in at least 20 years versus those that lose out.

Yet another market reversal on Wednesday will only add to their historical expense -- just as rising rates look ready to finally help value shares end a multiyear funk.

No one knows what will happen to Treasuries. But slicing and dicing stocks by their relationship to rates underscores just how much is riding on yields staying firmly at historic lows.

“If your valuation is expensive, more likely you’ll need a low bond yield to justify it,” SocGen’s global head of quantitative strategy Andrew Lapthorne said by phone. “If a vaccine looks like it’s progressing as they are then on a one-year view, what’s going to happen to monetary policy and what’s the upside for growth stocks given that regime change?”

Read More: Treasury Yields Near Pivotal 1% Level Before Final Supply Hurdle

While tech stocks led a fightback on Wednesday -- the Nasdaq 100 was up 2.1% at 3:38 p.m. in New York -- vaccine hopes triggered a surge in Treasury yields this week and a historic risk-on rotation. Momentum, which buys the past year’s winners like tech names, posted a record drop Monday while value saw its best two-day rally since August, Bloomberg’s long-short indexes show.

For most of 2020, falling yields have boosted the appeal of holding stocks like Big Tech with long-term cash flows. When rates drop on bad economic news, investors flock to these names for their ability to grow profits regardless of the business cycle.

That has generally translated into gains for growth and momentum factors and losses for value, which tends to bet on more cyclical stocks. Demand for defensive trades in the pandemic only intensified the divergence between those winners and losers.

Expensive Bets

In Sanford C. Bernstein’s analysis, the more expensive stock factors such as high credit quality and momentum tend to have a stronger correlation with bonds, while the cheapest ones like value have a negative relationship.

That helps explain the huge rotation. Momentum is even more pricey than its link with bonds would suggest, strategists led by Inigo Fraser Jenkins wrote in a note, making the factor especially vulnerable to a change in rates.

“This week’s vaccine news prompted the biggest dispersion in stock and factor performance that we have seen all year,” they said. “This says a lot about the built-up link within the equity market between valuation and correlation to bond yields.”

To be clear, there’s still controversy over the relationship between rates and factors. AQR Capital Management LLC argued in a paper this year that there’s no statistically robust link between bond yields and value, for example.

Read More: Marko Kolanovic Sees ‘Greater Staying Power’ in Value Rotation

Edward Gladwyn, a portfolio manager at Unigestion SA, agrees the dynamic is far from straight-forward. He says large factor swings are making it hard to make any directional calls for now.

“The sustainability of any rally in value is more likely to be driven by investors being willing to get back in the pool rather than a mechanistic impact of a supportive rate environment,” he said. “I could imagine a value rally even if rates stay depressed.”

For any investor buying value in a bet rates may rise, however, the Bernstein strategists have bad news: they see real yields remaining low.

“Despite antitrust battles for tech companies there is still a generally greater longevity of growth for high growth companies,” they wrote.

©2020 Bloomberg L.P.