Skeptic’s Roadmap Pinpoints Five Risks to Europe’s Market Rally

Skeptic’s Roadmap Pinpoints Five Risks to Europe’s Market Rally

(Bloomberg) -- The bout of investor exuberance over the European Union’s economic prospects that followed July’s landmark recovery fund deal may prove as brief as Belgian summers.

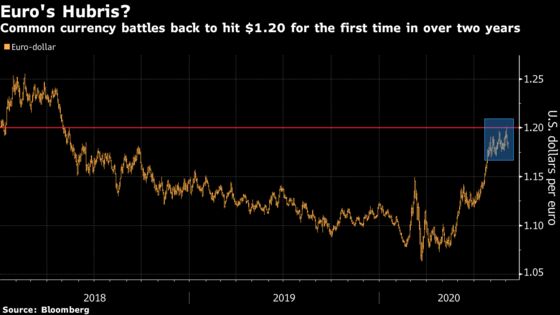

The euro surged above $1.20 this week for the first time in over two years, spurred on by the EU paving the way for unprecedented integration in the region through its 750 billion euro ($888 billion) jointly-financed recovery plan.

But the deal is still way off from being finalized, and with several potential stumbling blocks before year-end, the risk is that the bloc’s internal frictions will resurface and the market euphoria will quickly dissipate.

Add to that a host of other unknowns -- from Brexit to a possible resurgence of coronavirus cases, to growing Greece-Turkey tensions and the prospects of a bounce for U.S. assets -- and the coming months could prove tricky to negotiate.

The unraveling may have already started: the common currency tumbled about 1.5% since breaching that milestone on Tuesday, and European stocks on Thursday dropped by the most since July.

“The euro-area breakup risk has receded for now, but if you incorporate the right political risks, including a collapse of the recovery fund, or clear risks of that happening, then the break-up risks could return with a vengeance,” said Jan von Gerich, chief strategist at Nordea Bank ABP. “The euro’s good momentum would certainly reverse.”

On the optimistic side, the EU and the U.K. could secure a deal and the bloc’s members may ratify the recovery fund, while any progress on a virus vaccine would refuel the market rally. Still, here are five key risks investors and citizens would do well to watch out for in the coming months:

Recovery Fund Falls Through

Timetable: By year-end

The situation:

Investors may have thought that the gigantic stimulus package agreed by EU leaders in July is a done deal. It’s not. The plan for 750 billion euros in joint debt issuance still needs unanimous approval from the bloc’s parliaments, with Hungary threatening to hold back ratification until it’s reassured the disbursements it’ll receive won’t be subject to strict rule-of-law standards. The stimulus package also needs approval by a fragmented EU Parliament, which has threatened to block it.

The potential outcome:

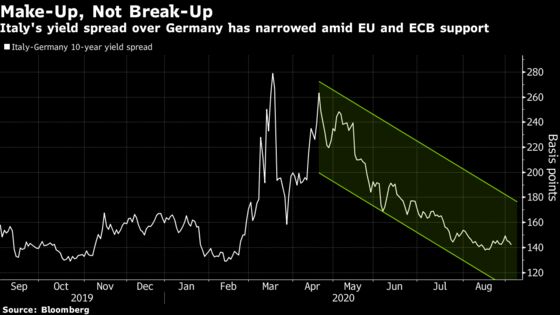

Such a delay could have significant negative consequences for the euro area, given how much debt countries across the region have taken on and how badly the funds are needed. Italy would be most at risk, with a dramatic bond sell-off in March providing a clue of what could materialize -- market liquidity would evaporate and investors may begin to price in a new euro-zone debt crisis.

The European Central Bank will potentially do its best to contain any fallout by boosting its emergency debt-buying program, but President Christine Lagarde may not be able to bear the burden alone.

“If this were to end up as a veto then you could certainly see peripheral countries suffer,” said Richard McGuire, head of rates strategy at Rabobank International Plc. “It’s not clear that optimism is the best thing for European markets.”

More Virus Pain

Timetable: Some countries are already there

The situation:

After a summer of relative calm and easing lockdowns, there are signs that Europe could soon be in the throes of a resurgence in coronavirus infections. Spain is basically there, and the country’s main business lobby warned last month that a second lockdown would have catastrophic consequences. That’s on top of what is already a very shaky recovery from the pandemic -- gauges of activity pointed to both Spain and Italy contracting in August. The Greek economy meanwhile shrank 14% in the second quarter to levels not seen since 1997.

The potential outcome:

A protracted slowdown would in theory be bad for the euro, but it also depends on how other economies -- most notably the U.S. -- are faring with their own efforts to contain the pandemic. For bonds though, more harm to the economy would likely be combated through further ECB action, narrowing the yield premiums of countries like Italy over those of Germany. Still, some of the more hawkish members of the institution’s Governing Council such as Jens Weidmann may be reluctant to agree to more.

Brexit Talks Go Bad

Timetable: The EU and U.K. want to secure a deal by the bloc’s October summit; Britain’s transition period closes at the end of the year

The situation:

Britain’s terms of departure from the EU have been agreed, but the framework of the future relationship has not. The bloc’s chief Brexit negotiator, Michel Barnier, said he’s worried and disappointed about the progress in discussions, warning post-Brexit negotiations between the EU and one of its biggest trading partners may end without a deal. Of course, we’ve been here before and the two sides managed a way through, but the threat of a cliff-edge remains large until an agreement is reached.

The potential outcome:

Right now, the possibility of the U.K. leaving the bloc without a deal on the future relationship isn’t being priced in by the market, with both the euro and the pound rallying to multi-year highs. But therein lies the risk. The closer talks get to the wire, the more market volatility is likely to creep up. Sterling will probably be hardest hit, but for every 1% fall it takes against the dollar, the euro might slide by around 0.2%, according to Jordan Rochester, a Group-of-10 currency strategist at Nomura International Plc.

Trump Secures Presidency

Timetable: Election on Nov. 3

The situation:

The U.S. elections will determine the tenor of the EU’s relationship with it’s largest trading partner. If President Donald Trump wins, the U.S. could double down on threats to penalize the EU with tariffs. He has vowed to dismantle the rules-based international commercial order, upon which the EU’s export-led growth model relies.

The potential outcome:

While a victory for Democratic candidate Joe Biden would likely give European assets a boost, the outlook for a second Trump term is far more murky. Elections, no matter who the victor, normally spur a rally in U.S. markets, and Trump’s last win was no different. Still, the incumbent’s far-from-complimentary view on the EU, and likelihood that the dollar would climb off the back of it, would be bad news for the euro, according to von Gerich.

“Trump’s policies are always a risk,” he said.

Military Standoff in the Mediterranean

Timetable: Ongoing

The situation:

While officials and diplomats in Brussels are busy trying to hammer out a deal on how to cut the EU’s carbon emissions to zero, the bloc’s southeastern flank may descend into chaos over good old hydrocarbon reserves. A standoff between Turkey and EU members Greece and Cyprus over contested maritime claims in the Eastern Mediterranean shows no signs of abating, despite efforts by Germany to broker a compromise. It was only last month when a Greek and Turkish frigate collided, highlighting the risks stemming from the continuing military build up in the region.

The potential outcome:

With Athens demanding EU sanctions against one of the bloc’s biggest trading partners, and France deploying reinforcements to back Greece and Cyprus, the prospect of escalation into an open conflict can’t be excluded. The impact on euro area markets right now is negligible, but alongside the other risks highlighted above, investors would do well to beware of a sudden escalation or an accident that could abruptly drag the region into its first war in decades.

©2020 Bloomberg L.P.