Short Volatility Trade’s Best Friend Is Now Its Biggest Enemy

Short Volatility Trade’s Best Friend Is Now Its Biggest Enemy

(Bloomberg) -- An about-face in derivatives positioning has turned a powerful source of market calm into a contributor to the chaos.

The coronavirus rout is igniting demand for hedges and unwinding option-selling strategies that proliferated in formerly placid markets. Dealers, once a buffer to volatility, have morphed into short-term momentum traders, amplifying swings. Experts hope the dynamic has reached its zenith, however, pointing to the expiration of options and futures on Friday as a potential catalyst for a shift that could re-establish a semblance of calm.

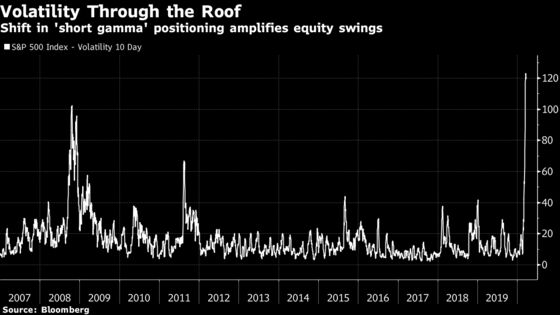

At play is how managing the risks associated with a Greek letter -- gamma -- moved from one class of financial institutions to another, contributing to the highest 10-day volatility in the S&P 500 Index since 1987.

Gamma Flip

Dealers were long the guardians of the Goldilocks markets that befitted an economy that was lumbering along, serving to moderate price action when it got too hot or too cold. Until recently, stated in the simplest terms, there were way more people looking to sell options than buy them, and dealers took their business.

Among the would-be sellers were institutions embracing a variety of fancy tactics, among them one known as call overwriting, in which someone who is long a stock sells an option on it to collect a fee and boost her return. These strategies are big enough to have implications for intraday price action in major equity indexes like the S&P 500.

Consider a pension fund engaged in a call-writing strategy. The dealer on the other side of the trade -- the call’s buyer -- normally goes short the underlying stock, so that if the option’s value declines, the loss is hedged. In Greek parlance, that’s known as staying “delta neutral.” To remain delta neutral, a dealer covers some of this short (buys the stock) when the stock falls, and shorts more when the stock advances. Therefore, dynamically managing of this “long gamma” position has the effect of tamping down realized volatility.

This is what happens in a tranquil market. In a haywire one, it flips on its head. At times like now, options lose their allure as quick bets to enhance yield, and revert to their fundamental role as market hedges. With institutions banging down the door to purchase protection, dealer activity radically changes. If investors are buying puts hand over fist, that means dealers are forced to sell stock to offset their exposure when markets fall.

JPMorgan strategist Marko Kolanovic described how this flip in dealer positioning contributes to an extreme see-saw in price action that sees stocks collapse one day only to zoom higher the next.

First, equities retreat as investors react to negative news on the outlook for the global economy and potential for corporate credit stress by fleeing risk assets. This prompts dealers to short more, driving the price of shares down too far. Then, prices overcorrect as this dynamic reverse itself 24 hours later, he said.

“As the convexity flows create a temporary market impact, the next day there is a reversion as the market returns to its fundamental clearing point,” he writes. “So it reverts (a large part of) the gamma move, but that triggers another round of short convexity flows that push it all the way back to the starting point of previous day.”

Clearing the Decks

Benn Eifert, chief investment officer at QVR Advisors, has chronicled the evolution of institutional option selling and the implications for market volatility since early 2012. Recently, he’s watched volatility-muting players withdraw from the market.

“Earlier in March, the usual suspects were rolling their overwrites and underwrites,” said Eifert. “Lately, it’s been zero, only covering existing shorts. Gamma supply is off for the moment.”

Derivatives experts are staying vigilant for signs that this vicious cycle may dissipate.

Investors might not be inclined to buy protection that appears expensive by historical standards going forward, in part because of how much exposures have been reduced during the market rout. There’s little need to hedge what’s no longer owned.

“From the long volatility perspective, it’s difficult to say there’s an attractive risk-reward proposition,” said Stacey Gilbert, portfolio manager at Glenmede Investment Management.

At one point last week, buying a put to protect against the possibility of the S&P 500 Index falling 10% over the coming year cost so mch the benchmark index would need to fall about 25% before that hedge would break even, according to her calculations.

Analysts also expect the quarterly expiration of options and futures could remove the positioning overhang that forced dealers into magnifying market moves.

“The extreme dealer ‘short gamma’ phenomenon of the past 1.5 months is in the process of clearing,” writes Charlie McElligott, cross-asset macro strategist at Nomura Securities, who suggested that gamma-related exposures could be cut in nearly half after Friday.

He reckons that the passing of these expiries may prompt investors to consider reinstating short-volatility bets, restoring the old state of affairs in which dealers “insulate” the market from shocks. Of course, fundamental developments on the coronavirus and the authorities’ response will remain front of mind for traders deciding what to do next, the strategist cautioned.

Megan Miller, portfolio manager at Wells Fargo Asset Management, highlighted how elevated open interest heading into this particular expiry could set the stage for a “clearing of the field” thereafter.

“The expectation for things to kind of clear out and begin again is quite strong,” she said. “For clients that are seeking yield, especially with rates near zero, it’s a good opportunity to sell as far out-of-the-money options as possible”

History shows that regimes of high implied volatility are likely to persist even after the most frenzied trading begins to subside, added Gilbert, a boon to future short-volatility bets.

“From a psychological and investment standpoint, traders are saying, ‘Hey, I just saw something unprecedented, can I say it won’t happen again in the future? No’ -- and that means implied volatility will stay elevated,” she said. “Maybe we can argue stocks are a great buy here, maybe not, but one thing we can very comfortably say is vols are at levels we rarely see and that opportunity set will be attractive as we come out of the craziness.”

©2020 Bloomberg L.P.