The Misguided Schumer-Sanders Buyback Solution

The Misguided Schumer-Sanders Buyback Solution

(Bloomberg Opinion) -- Senators Bernie Sanders and Chuck Schumer think companies are spending too much on buybacks and dividends to the detriment of their workers and communities. In a New York Times op-ed, they are proposing legislation that would restrict corporations from repurchasing stock unless they, among other things, agree to pay all workers at least $15 an hour and offer better pension and health benefits.

The senators’ solution, though, would reward bad investments and most likely lead to more corporate waste rather than improve the lives of the workers they are trying to help.

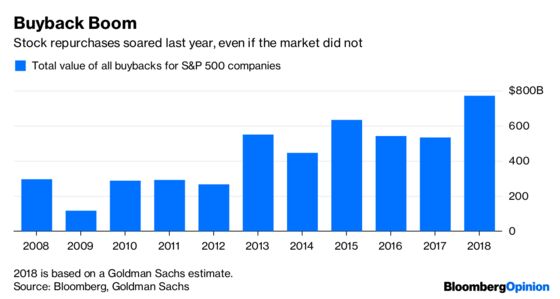

Sanders and Schumer are right that companies are spending a lot on buybacks — more than $4 trillion between 2008 and 2017, roughly equal to the Federal Reserve’s quantitative easing stimulus program. More than likely some, perhaps a lot, of that money has been wasted. As Warren Buffett has said, if the intrinsic value of a company is $100 and executives decide to buy back stock at $120 a share, they are essentially wiping out $20 of shareholder value every time they purchase stock.

Buybacks are seductive because they lift earnings per share quickly by reducing the number of shares outstanding. Even for investors, though, repurchases are not always positive. They can mask problems, like slowing business growth, and cause investors to overpay for shares, particularly when buybacks are not sustainable. And buybacks hide the cost of stock-based compensation that overwhelmingly goes to the executives who are approving buybacks, which is why the Securities and Exchange Commission nearly two decades ago started requiring companies to expense such pay.

That’s not to say buybacks lack value. Even Buffett, who has been generally critical of stock repurchases, has said they make sense at the right price. The brave companies, like investors, that bought stock in much of 2009 and 2010 were rewarded. Those were good investments and most likely better than the ones they could have made directly into workers or their businesses at the time. On the other hand, the $770 billion that S&P 500 companies spent last year with stocks near all-time highs and falling was likely not prudent.

But the regime that Sanders and Schumer propose would only make things worse. The two senators want to set conditions that would require companies to invest in their communities and “long-term strength” of their businesses before being able to spend a dollar on buybacks.

Even putting aside the issues of how to measure and monitor whether companies are investing enough in their workers and long-term strength, the senators’ proposal misses the mark. The reason companies should pay their workers more or make capital expenditures is because they are good or worthy investments. General Electric Co., for instance, has spent $217 billion on capital expenditures since 2000, or nearly $100 billion more than it has put toward buybacks. Given that GE’s market cap has sunk nearly $500 billion in that time, those capital expenditures look just as ill advised, in retrospect, as its buybacks. Force companies to spend money on either workers or plants before they make buybacks, and they will do just that, whether those investments make sense or not.

What’s more, by linking buybacks to minimum wages, Sanders and Schumer would give a further advantage to companies in industries that naturally pay higher wages, like finance and tech, by making it relatively easier for them to do buybacks and boost their stock market returns. This would concentrate even more of the already lopsided investment in the economy in those two sectors, neither of which are likely the employers of workers that Sanders and Schumer think of being the most left behind. If the senators want companies to pay workers more, they have a much more direct way to do that: raising the minimum wage unshackled from whether a company plans to buy back stock or not.

Sanders and Schumer are right that there is a problem with buybacks, but it really has to do with information. The returns from buybacks are often quick and easier to see. Paying higher wages or buying equipment is a less certain, longer-term investment. There should be more information around wages so that investors and others can see the return on that investment. Companies should not just have to expense the cost of stock-based compensation but disclose it more prominently. Prohibiting dividends and buybacks financed by debt could be an avenue worth exploring.

There are ways that Washington can encourage companies to be better long-term thinkers and local citizens, but restricting buybacks alone isn’t it.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.