Schroders Calls Fed's Scary Auto Delinquency Data ‘Fake News’

Schroders Calls Fed's Scary Auto Delinquency Data ‘Fake News’

(Bloomberg) -- A recent report from the Federal Reserve Bank of New York showing auto-loan delinquencies at near-peak levels is “a good example of fake news,” Schroder Investment Management North America Inc. said in a note this week.

Delinquencies are actually low by historical standards, according to the firm, which invests in asset-backed securities. The Fed’s data was calculated to include loan balances that have already been charged off, which exaggerates delinquency numbers, Schroders said.

If defaults that have already been taken as a loss, so-called chargeoffs, are removed from the data set as is the common practice for most indices, it’s clear that auto-loan delinquencies are at relatively low levels, Schroders said. They are certainly below what was seen during the financial crisis era. In fact, U.S. consumer performance overall is generally strong.

“While there has been a modest expansion in consumer credit, delinquency levels and defaults are back to the low end of historical levels,” said Michelle Russell-Dowe, head of securitized credit at Schroders, in a telephone interview. “This good performance is an important consideration that is not well represented by commonly-sourced government agency reports such as the New York Fed auto delinquency data.”

The Fed said that delinquencies were high despite low unemployment and a benign economy. However, Russell-Dowe also points to the fact that bankruptcy filings are at a 10-year low, calling that a “good and meaningful generic indicator” of overall consumer health.

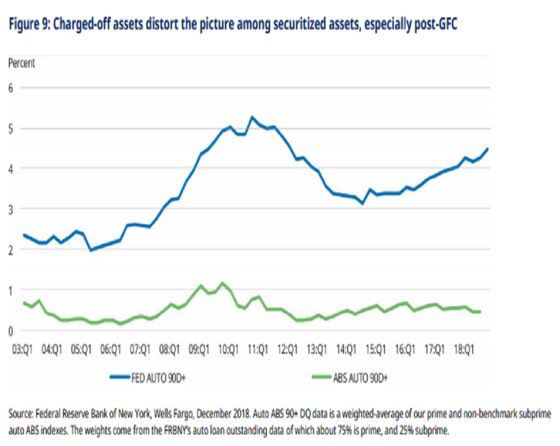

The New York Fed’s report last month showed that payments that fell behind by 90 days or more reached 4.47 percent in the fourth quarter, the highest since the first quarter of 2012. However, these levels are significantly higher than rates seen in a comparable Wells Fargo & Co. 90-plus day auto ABS delinquency index, which excludes charged-off loans and shows delinquency levels under 1 percent for a mix of bundled prime and subprime auto loans:

S&P Global Ratings had a similar message this week, saying in a research note that 90-plus day delinquencies for S&P-rated prime and subprime auto loan ABS was only 0.11 percent and 1.86 percent, respectively, as of Dec. 31. S&P also noted that delinquencies have been rising faster than actual loss levels on the packaged loans, which is said is a more important indicator. Credit protections in the deals, or cushions against loss, have increased commensurately with rising risk, according to S&P.

Deep Subprime Proliferating

Only 14 percent of auto loans originated last year were packaged into bonds, S&P said, but the securitization markets are typically used more often by so-called deep subprime lenders, rather than banks and credit unions. Even so, the ABS delinquency levels are still far less than the NY Fed numbers, pointing to the differences in calculation method.

Both Schroders and S&P acknowledged that delinquency levels have increased notably for asset-backed bonds underpinned by deep subprime borrowers. There has been growth in deep subprime lending over the last few years as private equity and venture capital firms have invested in auto lenders specializing in the least credit-worthy borrowers, pushing volumes amid increased competition.

“Subprime delinquencies of 30 days or more are back at their peak, and subprime borrowers don’t benefit as much from low unemployment as in the prime market,” said Schroders’ Russell-Dowe. “Additionally, the share of these private equity-backed subprime auto issuers in the ABS market has risen quickly; back in 2011 it was perhaps 10 percent, and now it’s closer to 50 percent.”

Then again, securitized debt makes up just a fraction of the overall auto credit market, while the majority is kept on finance companies’ balance sheets. Only about 10 percent of the $437 billion of low-rated car loans have been turned into ABS, according to Wells Fargo.

--With assistance from Randall Jensen.

To contact the reporter on this story: Adam Tempkin in New York at atempkin2@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Sally Bakewell

©2019 Bloomberg L.P.