Saks Parent Shouldn’t Fight a Buyout Like Nordstrom Did

Saks Parent Shouldn’t Fight a Buyout Like Nordstrom Did

(Bloomberg Opinion) -- Hudson’s Bay Co., the Canadian department-store giant, has recently shown itself willing to embrace big change in the name of survival: It sold off its troubled flash-sale business Gilt Groupe last year and has said it is considering selling Lord & Taylor after closing the chain’s storied Manhattan flagship location.

On Monday, its transformation efforts kicked into higher gear. The company announced a deal to sell its German real estate and retail joint ventures for about $1.5 billion, allowing it to focus more on its core North American business, which includes its eponymous department-store chain and Saks Fifth Avenue.

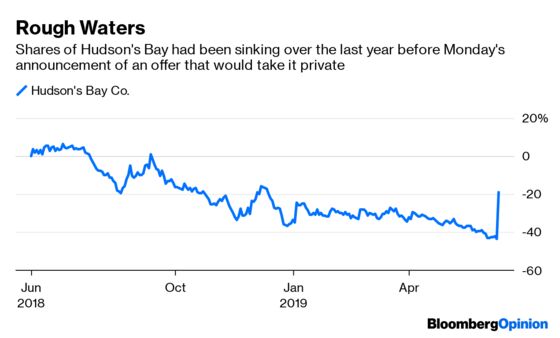

Even more importantly, the company said it is evaluating a bid from a shareholder group that would take Hudson’s Bay private. Richard Baker, the company’s chairman and one-time CEO, is part of a coalition that has proposed a cash deal of about about C$1.74 billion ($1.3 billion), or C$9.45 per share, a price the company said would represent a 48% premium over where shares closed on Friday.

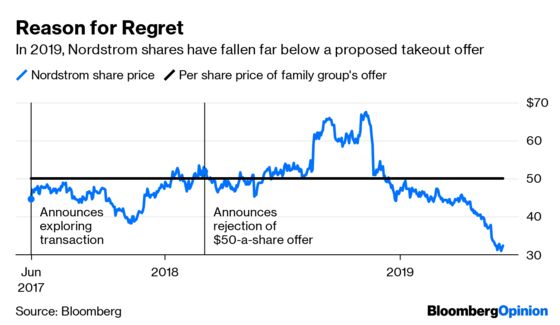

The board ought to accept this offer, and we don’t need to look too far into the past for evidence supporting this conclusion. Nordstrom Inc., a close retailing cousin to Hudson’s Bay, said back in June 2017 that it was exploring a take-private transaction. By the following March, it had announced that a special committee of the board had rejected a $50-per-share offer from a group that included Nordstrom family members. Weeks later, the talks were terminated after the parties couldn’t agree on a price. I have to wonder if the board looks back on that decision with regret now, as Nordstrom shares are trading at around $32.

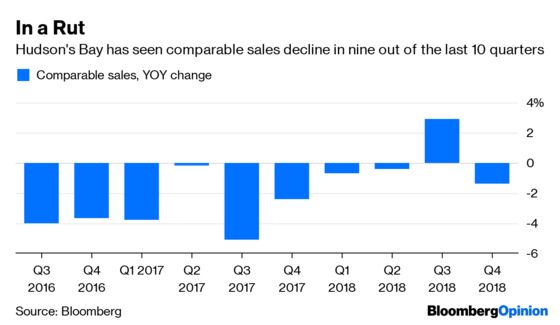

I suspect the story will be similar for Hudson’s Bay if it chooses not to take this buyout opportunity. The company’s recent same-store sales results don’t paint a clear picture of an imminent turnaround that would shore up investors’ confidence.

The department store business, in general, is only going to get harder from here. President Donald Trump has threatened tariffs on apparel and shoes coming to the U.S. from China, a potential curveball for retailers in those categories. Meanwhile, upscale brands such as Coach, Kate Spade and Michael Kors are focused on making their own stores and websites into bigger draws for shoppers, potentially sapping sales from department stores. And several department-store empires are dependent on enclosed malls, which are having a tough time drawing foot traffic amid changing shopping patterns.

Going private will allow Hudson’s Bay to work through these and other issues out of the spotlight. That’s a good thing, because I’d argue it has even more challenges than Nordstrom did when it was considering a similar exit. Also, the board should be comforted that the buyer group – which includes Rhone Capital, WeWork Property Advisors, Hanover Investments and Abrams Capital Management – is led by Baker, someone who has a significant history with the company that can inform his decision-making.

A better offer won’t come along for Hudson’s Bay. With the department-store business as brutal as it is, the board should leap into this safety net.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Sarah Halzack is a Bloomberg Opinion columnist covering the consumer and retail industries. She was previously a national retail reporter for the Washington Post.

©2019 Bloomberg L.P.