Safest Bond in Latin America Suddenly Looks Lot Less Stable

Safest Bond in Latin America Suddenly Looks Lot Less Stable

(Bloomberg) -- A wave of civil unrest has turned Latin America’s best-rated sovereign credit into the worst performer in emerging markets this month. It may be the start of a longer malaise.

Losses in Chile’s dollar-denominated bonds have accelerated this month as the economic cost of three weeks of protests and riots becomes increasingly apparent. Investment has stalled, shops are closed and tourists are staying away amid the biggest social uprising since the return of democracy in 1990.

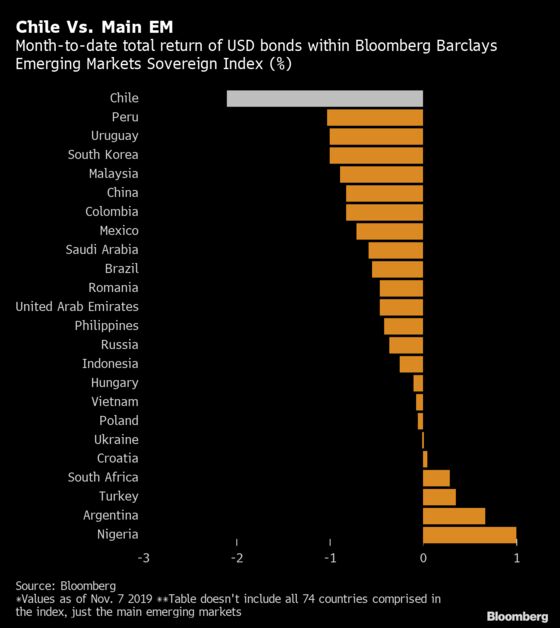

The dollar notes due in 2050 and 2047 posted the first and third worst returns among all 74 emerging and frontier markets in the Bloomberg Barclays Emerging Markets Sovereign Index. Chilean bonds handed investors a loss of 3.1% in the first seven days of the month, while the benchmark fell 0.3%.

Chile’s political and economic landscape has been turned on its head by the unexpected explosion of social rage. Twenty people have been killed and more than a quarter of all supermarkets have been vandalized, ransacked or burnt to the ground. It has come as a shock to the system for a country that was regarded as the most stable and well-managed in Latin America.

“Chilean markets, the economy, social-political system are undergoing regime shift,” said Arthur Budaghyan, the chief emerging-market strategist at BCA Research Inc. in Montreal. “As investors, we have to be open to the idea that this will entail new macro policies that will be more populist.”

Still, the nation’s credit risk is the lowest in the region and among the smallest in emerging markets. The cost of hedging against a Chilean default over the next five years is half that of Mexico and a third of that in Brazil.

Rising Cost

President Sebastian Pinera has announced a social agenda costing $1.2 billion, including a minimum monthly income of 350,000 pesos ($470) that will benefit more than half a million people as he tries to end the disturbances.

“This shock will deteriorate economic activity and investment,” said Felipe Labbe, an economist at Deutsche Bank based in New York. “Subsidies and required reforms included in the recent social agenda will impact the fiscal position and create more deficit.”

Yet, if Pinera he has any hope of quelling the unrest, he will have to go further. Protesters are demanding better pensions, healthcare, education and public transport, as well as a new constitution. They also want Pinera to go.

Finance Minister Ignacio Briones has cut the government’s growth forecast for the year to about 2% from the 2.6% predicted in September. He estimates the direct costs of the riots at between $2 billion and $3 billion.

As the protests go on and the pressure on Pinera builds, Budaghyan says Chilean assets are likely to underperform for six months to a year and he recommends shorting the peso versus the U.S. dollar and downgrading allocation to Chilean stocks from overweight to neutral.

Market Impact

Capital Economics economist Quinn Markwith says there is a good chance that protests will lead Chile’s gross domestic product to contract in the fourth quarter.

The benchmark IPSA stock index has fallen 10% since the troubles started on Oct. 18. The index hit a two-and-a-half year low on Wednesday.

The peso has been little better. The currency was the worst performer of 24 emerging-market currencies in October after the Argentine peso, reaching a 16-year low on Tuesday.

Even external bonds, which had been more resilient, started to decline this month as foreign investors turn more cautious. Chile’s dollar-bond spreads have widened over the past week after narrowing earlier this year.

But as protests drag on and an end to the clashes seems out of sight, even foreign investors are turning more cautious.

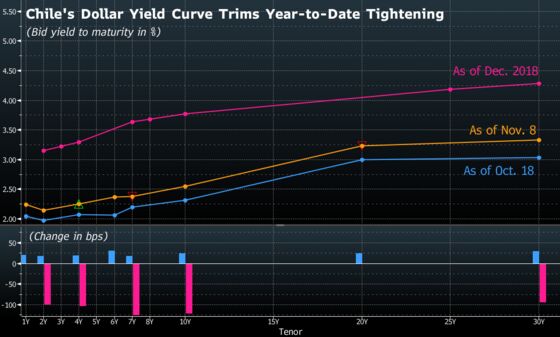

Technical analysis also doesn’t favor a rebound in Chilean bonds. The nation’s most liquid notes were trading at all-time highs before the protests erupted and some analysts say they continue to be expensive even after the recent correction. Bonds due in 2050 were traded at around 102.6 cents on the dollar on Friday, from a peak of 115 cents in early September. The bonds due in 2028 were worth 105 cents from 109 cents two months ago.

“The limited stock of USD bonds and relatively good fundamentals have benefited Chilean bonds valuations, but now investors are assessing the long-term impact of changes in the economic agenda,” said William Snead, an analyst at Banco Bilbao Vizcaya Argentaria SA in New York. “Even after the recent repricing, Chilean bonds look fairly valued to overvalued when compared to some Gulf Cooperation Council countries as Saudia Arabia, Qatar.”

--With assistance from Sydney Maki and James Attwood.

To contact the reporter on this story: Aline Oyamada in Sao Paulo at aoyamada3@bloomberg.net

To contact the editors responsible for this story: Carolina Wilson at cwilson166@bloomberg.net, Philip Sanders, Brendan Walsh

©2019 Bloomberg L.P.