South African Banks Face ‘Chicken or Egg’ Quandary as Economy Lags

South African Banks Face ‘Chicken or Egg’ Quandary as Economy Lags

(Bloomberg) -- South African banks are caught in a conundrum; they either lend into a stagnating economy or wait for signs of life. Should growth not pick up soon, it may not matter which way they go.

One of the world’s highest unemployment rates, tax increases, record fuel prices and gross domestic product that hasn’t expanded more than 2 percent since 2013 are taking their toll on businesses and consumers. Lenders have fought off the onslaught by boosting earnings from the rest of Africa and keeping costs and bad debts at bay. If the slump persists, earnings could start shrinking later next year, according to Denker Capital.

“In a low-growth environment, the banks try to tread water,” said Jan Meintjes, a money manager at the Cape Town-based firm. “It’s very difficult for them to grow their customer base,” while managing expenses gets harder the longer it takes to revive the economy.

The nation’s largest lenders, all of which make most of their earnings at home, are now looking to President Cyril Ramaphosa -- who in February replaced the scandal-tainted Jacob Zuma -- to restore confidence. The finance ministry is busy working on the details of a stimulus package to be unveiled later this month that will include a multibillion-dollar infrastructure fund and a review of power, rail and port tariffs.

For the moment, most lenders have tightened the credit taps amid political uncertainty ahead of elections next year and state-owned companies that are bleeding cash. With the country clinging to its last investment-grade credit rating from Moody’s Investors Service, which has the country on review, the recovery plan will also have to be implemented within existing spending limits.

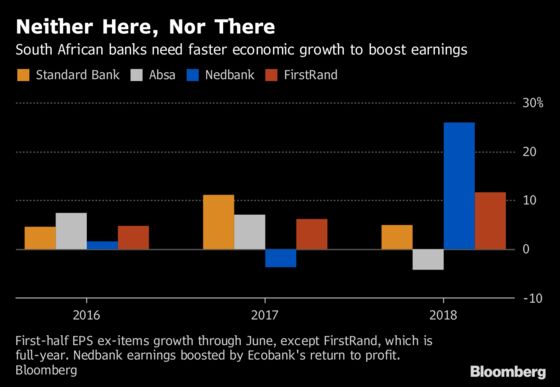

According to an analysis by Bloomberg Intelligence, total loan growth in the sector has been between 3 percent and 4 percent annually since late 2016, below the rate of inflation and weighing on revenue.

FirstRand Ltd., the nation’s second-largest bank, has stood out by winning market share to achieve 7 percent annual revenue growth in the past two years, said Philip Richards, an analyst at Bloomberg Intelligence. Absa Group Ltd. and Standard Bank Group Ltd., the country’s biggest lender, grew between 1-2 percent, he said.

Capitec Bank Holdings Ltd., the biggest provider of personal loans, expanded its book by 3 percent in the six months through August from a year ago.

For revenue to improve, the banks need a rebound in South Africa’s economy to be able to have the confidence to accelerate lending, said Patrice Rassou, head of equities at Sanlam Investment Management in Cape Town. Both are impossible without confidence.

‘Up Cycle’

“It’s a little bit of a chicken or egg situation,” he said. Having gone through the lean years, the banks will be well-positioned to benefit should the economy’s fortunes improve, Rassou said.

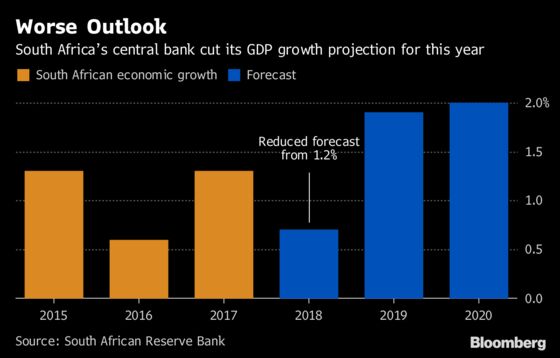

Meintjes at Denker also believes the banks will remain profitable even during the period of weakness because they are well capitalized and managed. They will emerge “stronger through the following up cycle, which will come,” he added. The World Bank on Wednesday cut its estimate for South African gross domestic product expansion to 1 percent this year from 1.4 percent and sees growth in 2019 remaining subdued.

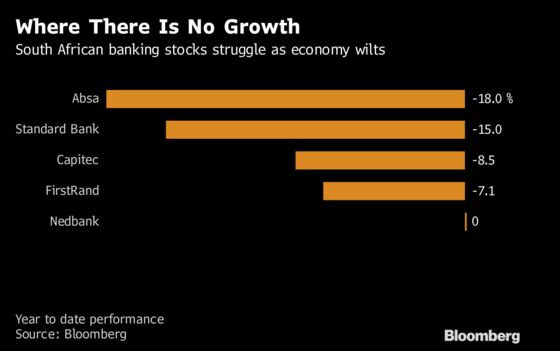

Investors still need to be convinced amid an emerging-market selloff spurred by concerns of a global trade war. The six-member FTSE/JSE Africa Index has declined 11 percent this year, with Absa down 18 percent.

Looming in the background is uncertainty over the governing party’s efforts to change the constitution to ease the expropriation of land without compensation. Banks have extended more than 1.6 trillion rand ($112 billion) in mortgages.

The potential uncertainty about expropriation is going to have a knock-on effect on the mortgage market, potentially stalling activity for borrowers and lenders alike, according to Richards of Bloomberg Intelligence. A parliamentary committee is examining the proposal, but hasn’t made its report yet.

“It is too early for banks to ramp up loan growth,” he said, “particularly in higher-risk personal loan and credit-card segments.”

©2018 Bloomberg L.P.