Rupiah Gyrations to Keep Foreign Bond Bulls at Bay

Rupiah Gyrations to Keep Foreign Bond Bulls at Bay

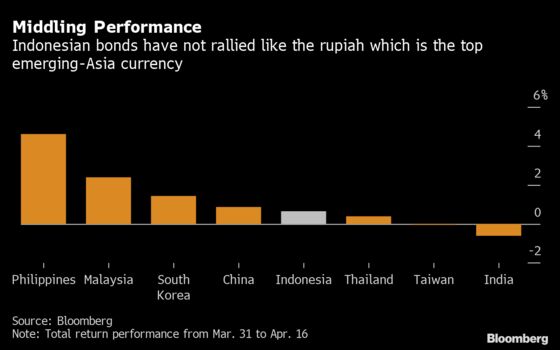

(Bloomberg) -- Foreign buyers are likely to steer clear of Indonesian bonds until the rupiah’s gyrations start to die down. That’s despite the value in the long end of the curve.

International funds fled for the door in the first quarter, with a record $8.7 billion in net foreign outflows, according to exchange data compiled by Bloomberg. Although Indonesian bond performance has improved, global investors still cut holdings by a net $79 million in the first 16 days of April.

The withdrawals have seen a considerable steepening in the Indonesian bond curve as they tend to be more heavily concentrated in the mid-to-long tenors. Foreign participation in Indonesian government bonds has fallen to around 33% from the 2020 high of 39% before the coronavirus pandemic, with a mad rush for the door in February and March causing the spread between two-and 10-year bonds to widen to 193 basis points, the most in nine years.

Local banks and investors were given a leg-up following Bank Indonesia’s decision to cut the reserve requirement ratio last Tuesday in order to free up more capital. This follows the $60 billion credit line with the Federal Reserve on April 7, which improved on dollar liquidity. But for a strong rally in Indonesian bonds to happen, foreign flows need to come on board.

Foreign funds attracted by Indonesia’s relatively high yields are faced with a stark reality -- that rupiah volatility and the associated costs of hedging may still make the game uneconomical at this point, especially for real-money funds. The spread between one-month and 12-month offshore non-deliverable forwards is around 1,000 basis points -- levels last seen during a rout in emerging markets in the third quarter of 2018 or around the time of the U.S. presidential election in 2016.

Bank Indonesia announced on Friday that it will be directly purchasing as much as 25% of the target issuance at the primary auction, with the initial target issuance in recent auctions amounting to 20 trillion rupiah ($1.3 billion). While this may provide some support for bond yields, it will not fully compensate for the decline in bid amounts. The most recent debt sale on April 14 saw incoming bids of 22.3 trillion rupiah, 66% below the average in the first two months of the year.

S&P Global Ratings downgraded Indonesia’s outlook on Friday to negative from stable, while maintaining the nation’s BBB rating, which is two notches above junk.

What to Watch

- It is a data light week ahead for Southeast Asia, with only Thai trade on Tuesday and Malaysian inflation data due Wednesday. Malaysia’s CPI will help reveal how much an impact the lockdown had on demand-led inflation

- Investors should get some insight into the impact of Thailand’s lockdown when the nation’s biggest banks kick off the earnings season this week. The outlook for corporate profits is the bleakest in Southeast Asia

- With Bank Indonesia keeping rates unchanged last Tuesday and the Philippine central bank cutting by 50 basis points on Thursday in an unscheduled move, the prospect of further surprise moves appears low for now in Southeast Asia

- Investors will be on the lookout for any further rating revisions on Indonesia from Moody’s Investors Service and Fitch Ratings following the outlook downgrade by S&P. The other two firms have the sovereign on a similar scale with a stable outlook

NOTE: Marcus Wong is an EM macro strategist who writes for Bloomberg. The observations he makes are his own and not intended as investment advice

©2020 Bloomberg L.P.