This $30 Billion Company Is Breaking Free

This $30 Billion Company Is Breaking Free

(Bloomberg Opinion) -- Roper Technologies Inc.’s stock slide now looks like unfair punishment.

The $30 billion company, which makes software for construction companies and legal firms as well as meter-reading tools, had slumped 11 percent in the month leading up to the release of its third-quarter results on Friday. That matched the decline in the S&P 500 Industrials index, which has been pressured as yellow flags on sales growth and profit margins fueled concerns that earnings have peaked. But there’s little sign of that kind of slowdown in Roper’s better-than-expected results or its 2018 guidance, which it raised for the third time this year. At least on Friday, investors acknowledged that fact, sending the shares higher.

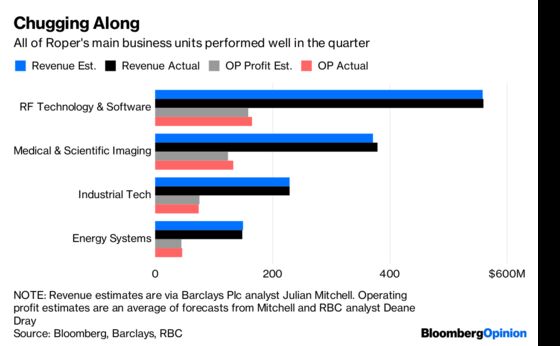

Organic revenue (which excludes the impact of currency fluctuations and M&A) grew 9 percent in the third quarter, tying Roper with Idex Corp. for the most impressive showing so far among major multi-industrial companies tracked by Bloomberg Intelligence. Roper’s adjusted gross margin increased 80 basis points to 63.8 percent, also surpassing analysts’ estimates. All of Roper’s main businesses reported better-than-expected profitability, with the exception of its industrial division, which was just a touch light.

You have to try hard to find something to pick on here. It’s not like that’s a rarity for Roper, which has now surpassed analysts’ earnings estimates for nine straight quarters. But this is the first period with Neil Hunn in the CEO seat, having replaced long-time leader Brian Jellison on Sept. 1. Some of the recent stock weakness could be attributed to jitters about the transition, which happened earlier than planned after Jellison was diagnosed with an unspecified medical condition.

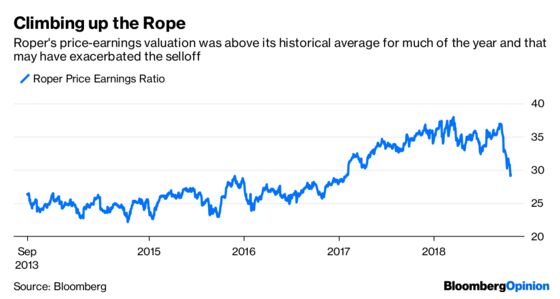

The bigger culprit for Roper’s inclusion in the broader market meltdown is likely its rich valuation and the fact that it’s still lumped in with industrial companies. Before this month’s sell-off, Roper’s average 2018 price-to-earnings multiple was a more than 20 percent premium to its historical five-year benchmark. Even after the slump, it’s easily one of the more expensive large U.S. industrial stocks. But it’s all about perspective, because Roper is only barely an industrial company at this point.

Roper gets more than half its Ebitda from software-related businesses after a series of smart takeovers in niche markets. A good example is this year’s $1.1 billion purchase of PowerPlan, which makes financial-planning software that helps companies manage taxes, compliance and budgeting. Relative to application-software companies, Roper’s valuation looks more reasonable. This shift in focus has made Roper’s business less capital-intensive, helping insulate it from the cost pressures that are a key worry of so many multi-industrial companies. In July, former CEO Jellison said tariffs are going to have a minimal effect on Roper because its cost of goods is so low relative to the typical multi-industrial company. Hunn echoed that sentiment on Friday during the earnings call.

Roper’s lingering ties to the manufacturing world are an energy unit that sells controls, testing and analytic tools to oil and gas companies and an industrial unit that sells pumps and valves. Those aren’t bad businesses. They’re high-margin and impressively stable during downturns. Roper’s private equity-like structure allows the units to be nimbler about pushing through price increases to head off rising costs. That said, these aren’t businesses that Roper needs to have and their cyclicality and capital requirements are elevated relative to the rest of the business.

The energy unit doesn’t hurt Roper that much, especially lately as sales rebound, but “It’s not a business that helps them,” Brent Puff, a portfolio manager at American Century Investments, said in an interview Thursday. “Most shareholders wouldn’t be disappointed” with a divestiture, he said. And because the track record for partial splits is poor, it would probably make sense for Roper to divest the industrial unit at the same time.

Jellison tasked Hunn earlier this year with undertaking a review of Roper’s business structure, but that’s primarily focused on shifting internal leadership and reassessing its business groupings after the software acquisitions. Perhaps Hunn should think bigger. This isn’t a screaming case for a breakup, but proactive portfolio management is what sets the top CEOs apart.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.