The Industrial World Just Lost a Great Leader

The Industrial World Just Lost a Great Leader

(Bloomberg Opinion) -- The industrial world just lost one of its best leaders.

Brian Jellison, who stepped down as Roper Technologies Inc.'s CEO in September due to health issues, died on Friday. He isn't well known outside of industrial-company circles, but he should be.

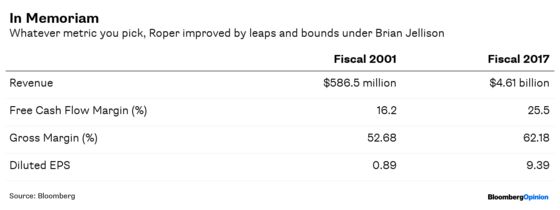

Jellison became Roper's CEO in November 2001 and steered an increase in the company's market value from a little over $1 billion to about $30 billion at the time of his retirement at the age of 72. Roper's 2017 free cash flow represented 26 percent of its revenue, the highest margin for a major U.S. industrial company and up from about 16 percent in 2001, according to data compiled by Bloomberg. The company’s gross margin is also best in class. That's a testament to Jellison's push to transform Roper from a dowdy industrial firm selling fluid-testing equipment and valves into a niche software company.

Roper now gets more than half its Ebitda from software-related businesses and it's constantly buying more of them, such as June's $1.1 billion takeover of PowerPlan, a provider of financial-planning software that helps companies manage taxes, compliance and budgeting. What makes the strategy work is Roper's focus on established markets where competition is scarce and margins are high. Those businesses then throw off a lot of cash that it can use to keep compounding its success. Roper's not trying to reinvent the wheel to challenge incumbent heavy-weights like Microsoft Corp. as some other would-be digital industrial companies have tried and failed to do.

It's always been interesting to me that more companies don't try to mimic Jellison's strategy. Idex Corp. and Ametek Inc. are perhaps the closest comparisons. I think the lack of others goes back to how hard it is to re-engineer the large, multifaceted businesses that comprise top industrial conglomerates. "Niche" software pushes have to be quite large or they get lost in the shuffle. Roper exemplifies the kind of nimbleness that the big industrial companies only find after a breakup. Even Roper itself could stand to streamline, as its continuing M&A push further marginalizes its legacy industrial and energy assets.

Jellison often gets compared to General Electric Co.'s Jeff Immelt because the two leaders' career timelines are closely aligned. Immelt officially replaced Jack Welch as CEO in September 2001, before handing the baton off to John Flannery in August 2017. Apart from the timing, you’d struggle to find two more different CEOs. GE's market value declined by nearly $200 billion under Immelt's watch, a drop that can only partly be explained by his efforts to slim down the company. GE has lost almost $140 billion in value since his departure as it grapples with the fallout from missteps at the power business and undealt-with liabilities at GE Capital. The ongoing slide prompted GE to replace Flannery with former Danaher Corp. CEO Larry Culp last month.

In some ways, the comparison of Immelt and Jellison is unfair. I'm not excusing Immelt, but it's undeniably harder to grow and improve a very large company. That contrast underscores the challenge now facing Culp, whose tenure at Danaher was similar to Jellison's Roper career. Culp took a relatively small, staid industrial company and remade it through smart acquisitions. Now, he's in charge of a sprawling, struggling empire whose market value exceeds Danaher's recent high even after GE’s recent slide. It won't be easy.

Nor will it be easy for Jellison's successor at Roper, Neil Hunn, to continue to drive that company's market value higher. But with Jellison's blueprint in hand, he's better equipped than most new industrial CEOs.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2018 Bloomberg L.P.