Traders Sidelined Robots and Picked Up Phones When Treasury Volume Surged

Traders Sidelined Robots and Picked Up Phones When Treasury Volume Surged

(Bloomberg) -- Panic over the pandemic and stricken U.S. economy catapulted trading in the world’s largest bond market to a record high last month, with much of Wall Street switching off their robots and picking up the phones to get deals done.

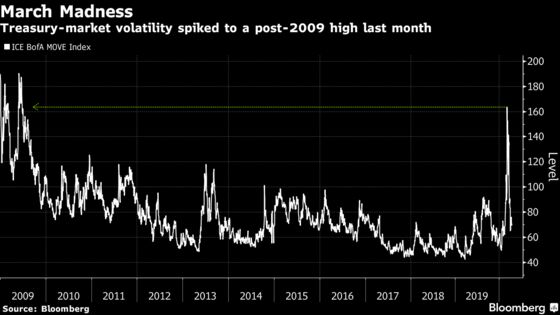

For the first time ever, average daily volume in U.S. Treasuries surpassed $1 trillion in the first week of March, according to research firm Greenwich Associates LLC. That beat the previous all-time high of $886 billion when the U.S. lost its triple-A credit rating at S&P in 2011. The panic stirred by the pandemic and U.S. economic shutdown brought historic lows and unprecedented oscillations in long-end Treasury yields, and a surge in volatility not seen since 2009.

This was a test of endurance for the robots that normally run much of Treasury trading. And the traffic surge in March -- a 41% increase in average daily volume from the prior month -- came without major mishap. But it did see more traders using phones or instant messages instead of the modern alternative: algorithms. Deals brokered via voice and IMs jumped to 42% of volume from just a quarter in February, according to Greenwich.

Michael O’Brien, director of global trading at $518 billion asset manager Eaton Vance Corp., says that’s probably due to the outlandish numbers people were seeing on their screens as it got harder to trade in some corners of the market.

“If you’re getting quotes and the bid/offers are considerably wider than what you’re accustomed to, the natural reaction is to pick up the phone and get a human on the line,” he said.

Overall, the industry seems to have kept up with the increased sprint of trading. There were no major malfunctions like the hour-long outage in January 2019 at CME Group Inc.’s BrokerTec, the biggest electronic Treasuries market. And there’s no evidence of anything systemic behind the wild swings over the course of March -- certainly nothing like the 12-minute roller coaster seen during the October 2014 “flash rally,” which alerted regulators to how market structure could threaten the stability of rates that are benchmarks for borrowing around the world. Though, of course, market participants may have experienced personal inconveniences last month in migrating their desks to their homes.

“In the past when there have been outages in some of the big primary venues, that’s certainly been news and you hear of it immediately,” said O’Brien. “I haven’t heard of any big serious disruptions, and that to me says the market held up well.”

When markets go haywire, banks tend to shut down their automatic pricing functions, or lower the size threshold, said Kevin McPartland, director of market structure at Greenwich.

“The humans reminded this automation-obsessed market how much they matter,” he wrote in the company’s report on Treasuries trading last month. Large asset managers Greenwich spoke with “mentioned periods during which pricing algorithms couldn’t dissect the latest news, if they were running at all.”

The past weeks have also highlighted how far advanced the Treasury market is in adapting to the robot world, compared with other fixed-income asset classes. If anything, O’Brien said, this experience of working from home may force those buyside traders less accustomed to electronic execution to adapt. Though in his view there’ll probably always be a place for human contact in trading, as a backstop, particularly in times of stress, and just to keep tabs on the market.

But that’s a projection for calmer times. At this juncture, with so much still afoot as traders confront the daily barrage of historic Federal Reserve bond purchases and a flood of government issuance, it’s too soon to say the volatility is done.

“It’s not obvious to me this period has ended and volatility has come down permanently and it’s smooth sailing from here,” O’Brien said. “So I wouldn’t say that market structure has passed the test yet.”

©2020 Bloomberg L.P.