Robots Bought Munis Amid Record Sell-Off’s ‘Baptism of Fire’

Robots Bought Munis During Record Sell-Off’s ‘Baptism of Fire’

(Bloomberg) -- In March, Jason Diefenthaler, director of tax-exempt portfolio management at Wasmer Schroeder, noticed something.

On a typical morning, the Naples, Florida-based money manager would get 25 bids each for the 50 to 300 municipal bonds he put up for sale to dealers. Now, he was getting two to five and they weren’t coming from Wall Street. Instead, independent firms that use algorithms to respond to thousands of auctions, were providing the best bids and buying bonds.

“Legacy dealers that we were accustomed to seeing step in were pulling back from all the volatility,” Diefenthaler said.

The liquidity crisis peaked in mid-March as fears about the economic impact of the coronavirus pandemic unleashed an unprecedented $40 billion stampede out of municipal-bond mutual funds during a two-week period. With Wall Street dealers’ inventories of unwanted securities swelling and traders focused on executing large trades for their biggest clients, algorithmic trading firms stepped in to make markets in smaller “odd-lot” bonds. These blocks of $100,000 or less make up 80% of secondary market trades.

On March 19, at the height of the sell-off, the number of unique bonds put up for auction in the secondary market rose to 32,000, triple the average. Headlands Tech Global Markets LLC, an affiliate of Headlands Technologies LLC, a Chicago-based quantitative trading firm, responded to 20,000 offerings, executing 4,400 trades, Chief Executive Officer Matt Andresen said in an interview. In March, the firm averaged 4,700 trades a day, compared with 1,600 in February.

“Our activity exploded,” Andresen said. “We knew this was a chance to really make our name in a baptism of fire.”

Nevada-based Sierra Pacific Securities LLC’s trading volume increased two to three times, reaching more than 1,000 trades a day, said Jarrod Dean, the firm’s co-president. New York-based Brownstone Investment Group LLC’s said its daily portfolio turnover, a measure of trading activity, reached as high as 20% in March.

Quantitative trading firms like Headlands, Sierra Pacific and Brownstone crunch more than a decades worth of data to build pricing models for hundreds of thousands of municipal bonds that rarely trade. Wall Street banks also employ machines to trade the smaller pieces of debt that prevail in the retail-oriented municipal market.

They bid each day on thousands of securities put up for sale on electronic platforms like ICE Bonds, Tradeweb Markets Inc. and MarketAxess Holdings Inc. After purchasing the bonds, the firms turn around and offer them seeking to capture a profit.

The $3.9 trillion municipal market still largely functions through over-the-counter trading where mutual funds, insurance companies and wealth managers place orders over the phone directly with dealers. However, electronic trading is growing, with 12% to 15% done that way, Greenwich Associates estimated last year.

The average daily volume of municipal-bond trades on Tradeweb rose to about $400 million in March, a 44.8% increase from a year earlier, the company reported. MarketAxess reported an average of $61 million traded in March, triple the prior year. ICE Bonds, a unit of Intercontinental Exchange doesn’t report trading volume.

Firms using a pricing algorithm picked up a larger share of trades on Tradeweb in March, said John Cahalane, head of Tradeweb Direct, the company’s retail trading platform. He declined to share specifics.

“If you didn’t have some kind of suggested pricing or algorithmic pricing, you couldn’t possibly have been responding to just the sheer number of requests for quotes,” Cahalane said. “If there was an advantage the algo firms had during that period, it was the ability to be present.”

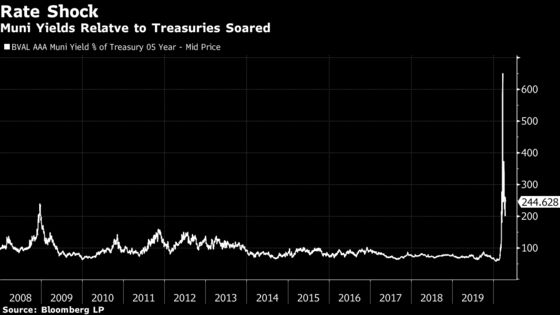

Yet, some investors said they saw a noticeable decline in bidding by algorithmic traders during the extremely volatile period. With too many sellers at once and buyers scarce, prices went into free-fall and closely-watched trading relationships went haywire. On March 23, yields on five-year municipal bonds skyrocketed to 6.5 times yields those on Treasuries of the same maturity, almost three times the peak during the 2008 financial crisis.

“Their presence in the market at times of volatility has diminished,” said Lyle Fitterer, co-head of municipal investments at Baird Advisors, said of algo firms. “They don’t take a tremendous amount of capital risk.”

The pullback by computer traders was more evident among banks that use them, not independent firms, said Ben Pease, Head of Municipal Trading at Breckinridge Capital Advisors Inc., which oversees $40 billion assets. The average number of bids Breckinridge received on odd-lot bonds from major bank algos dropped by almost half during the weeks of March 9 and March 16 from the prior two weeks, he said. On average, they bid on about 30% of Breckinridge’s thousands of items, down from about 75%, he said.

“My feeling is that banks were selectively allocating their remaining capital, which ultimately reduced bids for the extensive numbers of odd lots and small blocks seeking liquidity,” Pease said. “‘Pure’ algo shops provided more liquidity when it was needed, albeit at a higher cost.”

The cost to trade investment-grade state and local government bonds maturing between 5 and 10 years rose to almost 2.6 percentage point on March 25 as all dealers demanded more compensation for the risk of taking debt onto their balance sheets, according to BondWave, a financial technology company.

Headlands was able to balance its buying and selling throughout the month, Andresen said. Computers enabled the firm to react to the market and update prices in real time. The market value of the firm’s portfolio was just under $1 billion at its peak in March.

“It was definitely harrowing,” said Andresen, a former co-chief executive at Citadel Securities, who founded Headlands in 2010. “Your P&L will swing around and your portfolio will swing around. We’re not going to panic, we’re not going to drop out of the market.”

©2020 Bloomberg L.P.