ADVERTISEMENT

Risk of Big Rates Swings on Brexit Vote Is Options Trading Arena

Risk of Big Rates Swings on Brexit Vote Is Options Trading Arena

18 Oct 2019, 08:46 PM IST

(Bloomberg) -- The risk for big market swings on the back of the Brexit vote in Parliament Saturday is the ideal territory for savvy options traders.

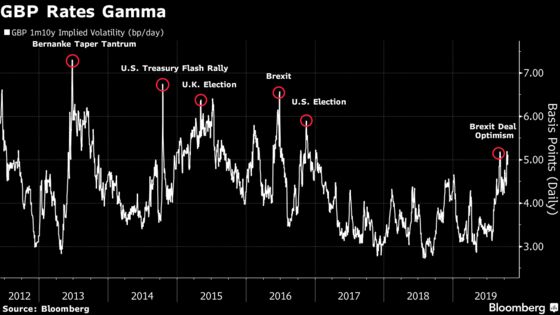

There is scope for gilt yields to keep moving higher if a deal is ratified by lawmakers. But the outcome of the vote remains too close to call and so positioning for it is best done through options that protect the risk either way.

- If Boris Johnson can pull off getting the deal to pass through Parliament, then 10-year gilt yields should move close to 1%; otherwise in the event that the tail risk of a no-deal starts looking more likely (if the vote fails and the EU refuses an extension) then yields should see new record lows as emergency BOE rate cuts come into view

- Positioning for a limited sell-off in the case of the deal getting ratified while limiting the risk points to payer spreads rather than outright exposure

- For the short term, implied volatility on the 10-year swap rate is suggesting a potential move of around 28 basis points in either direction over the next three months, which seems reasonable relative to the Brexit premium and macro picture; over the next one year, volatility on the 10-year swap rate implies a 68% chance of 10-year yields trading between 0.10% and 1.40%

- Payer swaptions can be cheapened by selling high-strike options that would benefit from yields rising but settling in a higher range given the focus would then shift to a global growth slowdown

- Another option to consider in the case of a deal would be conditional bear steepeners, as the front-end would find it difficult to price in a BOE hike cycle convincingly given the global slowdown and signs of U.K. labor market weakness

- In the case of a further extension or if a deal gets passed, implied volatility should fall across the surface, but may underperform on longer-dated tenors given the top-left of the volatility surface is sensitive to the outlook for monetary policy

- Selling elevated volatility has been a profitable trade since the EU referendum where investors take advantage of a build-up of Brexit uncertainty before a period of calm

- The Brexit premium in U.K. fixed-income markets is by far the highest in inflation breakevens; there is still plenty of premium to be removed if a deal is ratified, to the benefit of floor options that bet on inflation falling below a certain threshold

- NOTE: Tanvir Sandhu is a global fixed income and derivatives strategist who writes for Bloomberg. The observations he makes are his own and are not intended as investment advice

©2019 Bloomberg L.P.