Repo Is Ending a Very Eventful Year in an Unusually Subdued Way

Repo Is Ending a Very Eventful Year in an Unusually Subdued Way

(Bloomberg) -- The end of each year tends to be a bit antsy for short-term dollar borrowing but -- as with many things -- 2020 is turning out to be quite different.

The Federal Reserve’s response to the coronavirus pandemic and a ballooning of bank reserves appears to have anesthetized the funding market against many of its usual new year’s headaches -- even more than the central bank did with the extraordinary measures it implemented in late 2019. There is, of course, the usual increase in demand for greenbacks, but the flood of cash from the Fed means that the premium for getting your hands on U.S. dollars has been relatively muted.

“This year may be unique given the set of constraints that typically impact year-end,” said Gennadiy Goldberg, a rates strategist at TD Securities. “The Fed’s flooded the market with liquidity and the banks are not trying to whittle down their balance sheets as aggressively as they typically do.”

In key funding markets such as those for repurchase agreements and cross-currency basis, rates have tended to spike in December over recent years. That’s in large part due to regulations and capital surcharges that encourage banks to curtail their balance sheets at the end of the year. That helps to create a pinch in the supply of dollars at a time when others in the market typically seek funds to cover positions over the year-end turn.

That doesn’t look like it will be a problem this time around. Repeated upheavals during the past two years -- most notably in September 2019 and March 2020 -- have seen the central bank utilize a formidable arsenal of new repurchase-agreement operations, asset purchases and other tools to safeguard the financial system. And even though some of them are relatively dormant right now, their very presence appears to be keeping rates in check.

In addition to the abundance of cash in the market and the availability of Fed repo operations, Curvature Securities’ Scott Skyrm points to the lack of leverage at hedge funds and the effect of the supplementary leverage ratio for banks being suspended in helping to create a “perfect” year-end for repo markets.

“There’s almost no year-end premium priced in the market and no one expects the chance of funding pressure,” he wrote in a note to clients. “But note, this is the last quarter with all the stars aligned,” he said, drawing attention to the fact that the SLR suspension will expire on March 31.

Nonetheless, the Fed on Wednesday gave another clear signal that it’s not in any hurry to pull back from some of its more recent innovations, announcing that it would extend through September two of the programs that help insure there is a ready supply of U.S. dollars worldwide. Officials will extend U.S. dollar liquidity swap lines that were opened in March between the Fed and nine foreign central banks, and they will also extend the temporary repo facility for foreign and international monetary authorities.

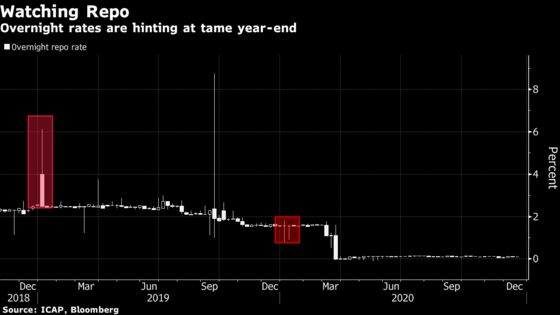

Previous Spikes

As year-end approaches, levels on repo agreements, which allow borrowers to temporarily exchange their U.S. debt holdings for cash, have barely budged -- a stark contrast to what took place two years ago and during the major spike of September 2019. In 2018, overnight funding rates soared above 6% on the last trading day of the year. And that paled in comparison with what took place some nine months later when repo turmoil saw rates shoot to 10% from around 2%.

That particular episode prompted the U.S. central bank to undertake its own repo operations, which grew to the point of making available around half a trillion dollars of extra liquidity for the end of 2019. The central bank further boosted those facilities in March this year when pandemic-related strife also spurred the Fed to revive its asset-purchase program, introduce myriad credit facilities and fine-tune existing operations to ensure market functioning.

The Fed’s renewed foray into bond buying has had the effect of creating vast bank reserves that are well in excess of what America’s lenders need to hold. The result is that firms have plenty of liquid assets on their balance sheet, further reducing pressure in a market already supported by the backstop of Fed repo facilities.

With the year entering its final stretch, the only real signs of stress have been in the market for cross-currency basis swaps -- and even that is a far cry from the upheaval of times gone by. At one point the cost to borrow dollars for yen over the next three months rose to the highest level since May. And while similar signs of dollar demand also showed up in euro-related markets.

| Related Stories |

|---|

ECB Buying Puts Squeeze on Year-End Funding SNB Operation May Open Funding Pressure Valve Demand for Dollars Amps Up Pressure on Libor |

TD’s Goldberg said that with bank reserves being ample and growing, the current situation is quite unlike what took place in September 2019 and “there shouldn’t be much of a problem at year-end.”

The Fed’s liquidity measures have also eliminated demand from relative-value investors, a group that tends to need to lock in funding for the end of the year to roll their trades, according to NatWest Markets strategist Blake Gwinn.

“When the Fed is buying, their opportunities get squashed,” he said. Taken together, “all signs point to no balance-sheet pressures.”

©2020 Bloomberg L.P.