Record Bond Rally Hinges on Draghi Delivering a Full QE Package

Record Bond Rally Hinges on Draghi Delivering a Full QE Package

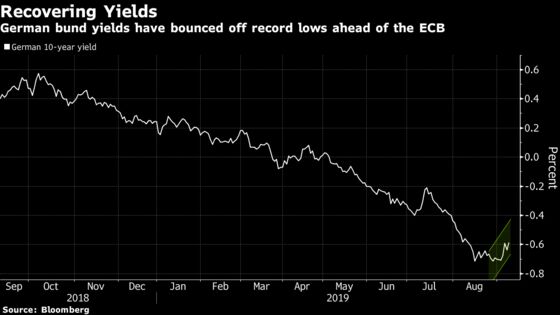

(Bloomberg) -- Mario Draghi needs to go out with a bang if he’s to renew a surge in bond prices that sent yields to unprecedented lows.

Markets have factored in the European Central Bank’s president slashing interest rates and restarting quantitative easing, so it will take a multi-faceted stimulus package in his penultimate meeting Thursday to impress investors. Bond gains have faltered and the euro has staged a recovery from the weakest since 2017 this month after opposition from some officials raised doubts over the size and timing of any new asset purchases.

Money markets are still betting on a 15-basis-point interest rate cut on Sept. 12, a bigger drop than the 10 basis points forecast by economists. Those expectations for policy easing to revive inflation have depressed the euro to $1.10 and driven German bund yields well below the ECB’s minus 0.4% deposit rate.

“I think that the ECB will struggle to exceed the already dovish market expectations,” said Valentin Marinov, head of Group-of-10 currency strategy at Credit Agricole SA. Any failure to mitigate the fallout from even more negative rates on banks and to lift limits on the bonds the ECB can buy could spur euro gains to $1.12, he said. “Without them, people will conclude that Draghi is done and that the ECB may not have the courage for more once he is gone.”

| Read more: |

|

Given this week’s ECB gathering “appears to be one of the most unpredictable of the past five years,” strategists at Bank of America-Merrill Lynch are recommending option hedges in case the central bank fails to deliver on quantitative easing. Goldman Sachs’ strategists have stopped recommending bets on the euro’s decline against the yen ahead of the announcement, while Morgan Stanley has scaled down its estimate for the size of future asset purchases.

That caution led European bonds to fall in recent days, the latest in a series of pullbacks from the rally. Longer maturities have been worst hit, following poor demand in a 30-year German auction, as they would benefit the most from renewed ECB asset purchases. Allianz Global Investors has warned of a bigger sell-off in German bunds and does not see the central bank relaunching its asset purchases at this stage.

Here are further views by analysts:

Credit Agricole (Risk of Euro Rebound)

- “Lot of negatives” are in the price of the euro -- a 10-basis-point rate cut is fully priced in and investors attach a 45% chance to a 20bps rate cut: Marinov

- Euro could “squeeze higher” versus the yen and Swiss franc and to a lesser degree the U.S. dollar

- Euro-dollar estimated fair value has been reduced from $1.1234 to $1.1186 on the back of a flattening in the European bond curve relative to the Treasury curve

- This variable is the strongest driver of the euro’s fair value at present, especially in the run up to this week’s ECB meeting with the market anticipating a fresh round of QE

- If the European curve bear steepens on Draghi, the euro’s fair value could bounce again

Morgan Stanley (Bund Steepeners, Euro Rally)

- ECB to deliver an easing package of 10 basis points of rate cuts and restart QE at a pace of 30 billion euros per month for nine-12 months, according to strategists including Chetan Ahya

- “However, markets could be disappointed by the timing and size of the QE program”

- Suggests investors put on positions in 5s30s bunds steepeners -- as they see 10- and 30-year bund yields ending the year higher

- Continues to recommend investors short two-year German bunds at minus 90bps and/or pay March 2020 ECB meeting OIS

- The euro should rally post the ECB decision “as sentiment is already bearish and a more hawkish ECB outcome that leads to a steeper yield curve will push the euro higher and dollar down”

Bank of America-Merrill Lynch (Imperfect Package)

- “Hard-to-forecast ECB meeting could disappoint high expectations,” strategists said in a client note, adding that they predict a 20bps deposit rate cut with tiering and a “small” QE of EUR20b-30b for 9-12 months

- There is a risk smaller or no QE, for which they recommend option hedges

- BofAML still have a 10s30s flattening view in rates

- Disappointment could see some steepening but strategists “think this is unlikely to be sustained” as monetary policy will “struggle to change the narrative for the long-end of the curve”

- They recommend selling any euro rallies as the currency remains under pressure from weak euro-zone economic data

Allianz Global Investors (No QE Relaunch)

- Predicts 10bps deposit rate cut, multi-tier deposit facility and stronger forward guidance, with an explicit commitment that key rates will remain low for a long time, according to Franck Dixmier, global head of fixed income

- Unlikely the ECB will announce the relaunch of its bond-buying program at this stage as there seems to be no consensus about “whether a new round of QE is desirable, even if the option remains on the table”

- If high market expectations aren’t met by the ECB there might be an opportunity “to take advantage of possible rate and spread tension to buy on dips -- in particular by reinforcing duration on sovereign bonds and increasing credit exposure”

NatWest Markets (Flatteners Attractive for Bond Bulls)

- “ECB expectations got too aggressive this summer. They may have more to correct,” according to Giles Gale, head of European rates strategy

- “Flurry of hawkish rhetoric was more of an attempt to dial-back over-ambitious market expectations and give some headroom for a dovish surprise, rather than a sea-change at the Governing Council”

- Would be “surprised if no QE were announced” -- sees 10-basis-point rate cut (accompanied by tiering) and a re-start of QE at 30 billion euros a month for six months (accompanied by increases in the issue and issuer limit to 50%)

- Steepeners don’t look like the ideal bearish trade right now, while if bullish, 5s30s flatteners (with positive carry) look attractive

Commerzbank (Fleeting Euro Impact)

- Commerzbank still expects a “substantial extension” of QE purchases despite the hawks’ opposition and this could weigh on the euro

“Any immediate euro-negative reaction to the ECB could prove short-lived,” according to Esther Reichelt, a currency strategist - Expects growing political pressure on the Fed to continue rate cuts, in particular if we see (temporarily) lower euro-dollar levels

- Sooner or later the market should become aware, that the bigger the ECB’s easing package this week, the less the ECB will be able to do in the future, which could actually support the euro

To contact the reporter on this story: Anooja Debnath in London at adebnath@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Neil Chatterjee, William Shaw

©2019 Bloomberg L.P.