Recession, Rating, Politics: A Winding Road for Italy's Bonds

Recession, Rating, Politics: A Winding Road for Italy's Bonds

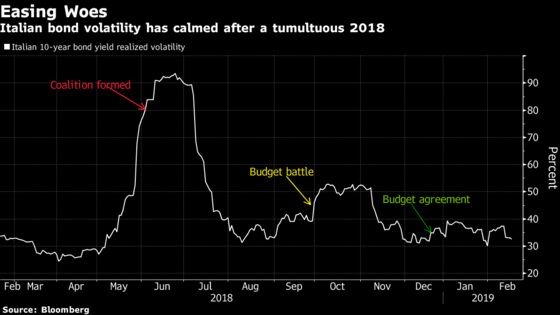

(Bloomberg) -- Italy’s bonds are enjoying a period of relative calm while Spanish politics hogs peripheral euro-area headlines. But the market’s sense of stability is looking increasingly fragile as economic uncertainties mount.

The nation is already in recession, the budget deficit is widening and the threat of a credit-rating downgrade looms -- a risk cocktail that could potentially blow out bond yields. At the same time, the market will draw some support from the European Central Bank’s asset purchases and the possibility of new, cheap loans, while the lingering prospect of early elections may be favorable even though it could fuel volatility.

Here is a rundown of the potential hurdles for Italian bonds:

Recession

The economics don’t bode well. Already the euro area’s second-most indebted nation, Italy is the first to dip into recession during the current cycle, with the economy having contracted in the second half of 2019. Data published Tuesday added to the bleak outlook, showing a bigger-than-expected slump in industrial orders in December.

That casts serious doubt on Rome’s ability to cap this year’s deficit at the targeted 2.04 percent. While an overrun would result in increased bond supply, it could also put the nation in conflict with the European Union once again. The bloc’s deficit limits stipulate a shortfall of no more than 3 percent, with the goal of bringing the debt-to-output ratio down to 60 percent. Italy’s is currently at 130 percent.

“Against the backdrop of low growth, risks of possible downgrades and concerns about debt sustainability possibly resurfacing among investors, we struggle to see too much upside on BTPs,” HSBC Holdings Plc strategists Fabio Balboni and Chris Attfield wrote in a note. “The deficit could hit 3 percent of gross domestic product, or more, which could again put Italy on a collision course with Brussels.”

In the immediate future, the threat of a downgrade by Fitch Ratings Friday to one level above junk is looming amid rising fears that the securities may soon not be eligible for inclusion in global benchmarks. Citigroup Inc. strategist Jamie Searle said that a cut to BBB- could also propel the yield on German bunds to four basis points and lower.

Politics

A coalition between the League and the Five Star Movement was perhaps never likely to be a stable one, especially in a country that has had 66 governments since the war, but their diverging fortunes in the polls has fueled the prospect of fresh elections.

Such an outcome may not be that bad for investors though. The strong showing of the League may mean that it could govern with its natural allies on the right -- Silvio Berlusconi’s Forza Italia and the Brothers of Italy -- which would probably be more market-friendly than the current partnership.

Mizuho International Plc strategist Peter Chatwell estimates that, under such a scenario, the Italy’s 10-year yield premium over German bunds could narrow to around 200 basis points, a level not seen since last May. The spread was around 265 basis points Monday.

Supply

Italy has front-loaded its debt issuance this year, taking advantage of record demand for euro-area bonds amid slowing economic growth and receding expectations for an interest-rate increase. But the nation still needs to underwrite around 88 percent of its funding requirements for the year -- that means it remains vulnerable to the risk of a slump in investor appetite should the economic backdrop worsen or the sovereign rating is cut.

“The ‘tango de la muerte’ between markets and the Italian Treasury is likely to be very interesting this year,” said James Athey, a money manager at Aberdeen Standard Investments. “The point at which the market is satiated is very difficult to find ex-ante, but you sure as sugar know when you’ve found it ex-post.”

ECB

The bond market may draw comfort from the falling expectations for an ECB rate increase, with money-market pricing already pushing out the estimated timing of a hike to mid-2020. With bund yields grinding down toward zero, investors could choose to snap up Italian bonds, which pay some of the best rates in the euro area.

Additional support could come in the form of another round of targeted longer-term refinancing operations by the ECB, which is currently being discussed by the institution, according to Benoit Coeure, the Executive Board member in charge of markets. That could help support peripheral euro-area bonds, including Italy, according to Credit Agricole SA.

--With assistance from Marco Bertacche and Cecile Gutscher.

To contact the reporter on this story: John Ainger in London at jainger@bloomberg.net

To contact the editors responsible for this story: Ven Ram at vram1@bloomberg.net, Anil Varma, Scott Hamilton

©2019 Bloomberg L.P.