Waste Hauler to Face Resilience Test as Analysts Start Coverage

Recession-Proof, Maybe, But Waste Hauler Needs More to Bag Buys

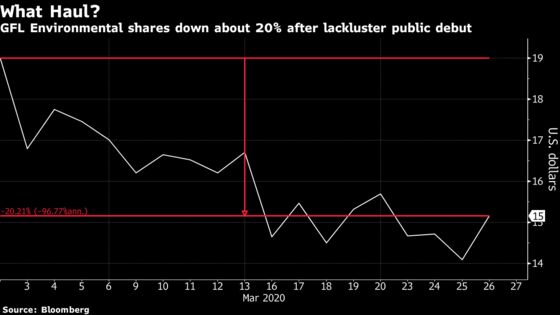

(Bloomberg) -- Waste haulers tend to be a resilient bunch in a downturn, hence GFL Environmental Inc.’s ability to complete its IPO even amid the early stages of a market sell-off.

The Ontario-based company’s durability will again be tested when analysts offer up their ratings as soon as Monday. Despite being positioned in a sector that’s seen as recession proof, there are some weak spots in GFL’s armor, including a debt-laden balance sheet and an unproven ability to generate cash.

Shares are down about 20% since the IPO, hitting an all-time low on Wednesday, and may fall further if analysts at the banks that underwrote its initial public offering initiate coverage with less friendly reports than what typically follows freshly issued stock.

“Waste haulers are a defensive bunch during times of volatility,” said Scott Levine, industrials analyst at Bloomberg Intelligence.

He cited the performance of the Big 3 haulers -- Waste Management Inc., Republic Services Inc. and Waste Connections Inc. -- during parts of the last recession. However, it’s difficult to ignore GFL’s negative cash flow and its debt, which is higher than the peer average, Levine said.

GFL went public in March after a pair of withdrawn launches. After the second attempt, the company racked up acquisitions, which has left its net debt four times that of its earnings as measured by Ebitda and on a pro-forma basis, Levine said. That’s higher than the debt ratios of the three major solid waste haulers, which are about two to three times earnings. In addition, that group tends to generate free cash of about 8% to 12% of sales, and on an operating cash to capital expenditure basis. GFL is cash negative.

Organic growth overall is a bit better than the group, Levine added. Ebitda margins, however, are also lower than that of peers.

What’s critical in persuading sell-side analysts to issue a buy rating is the company’s ability to convince investors that its higher-than-average growth will eventually turn into cash. Such liquidity would allow GFL to hold its breath with its peer group as coronavirus rocks markets and global economies.

©2020 Bloomberg L.P.