RBA Drops Hints QE Coming and It Differs From Expectations

RBA Drops Hints QE Coming and It Differs From What Many Expect

(Bloomberg) -- Australia’s central bank has just dropped one of its strongest hints of how quantitative easing could look Down Under. It turns out to be quite different to what many in markets are expecting.

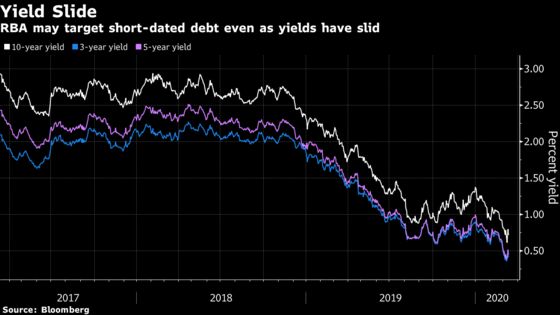

The Reserve Bank of Australia may follow the Bank of Japan’s targeting of bond yields rather than making large purchases each month to keep rates low, according to comments made Wednesday by Deputy Governor Guy Debelle. To be truly effective, that suggests the RBA will have to target shorter-dated government debt, according to JPMorgan Chase and Co. and Royal Bank of Canada.

“If you’re thinking about trying to keep the front end of the risk-free curve low for a period of time then that’s more analogous to an interest-rate reduction,” Debelle said of potential operations in Australian bond markets. “It’s easier to think about it more in terms of the price sense than in the quantity sense.”

Investors are already pricing in some form of potential unconventional policy with longer-dated Australian bonds outperforming interest rate swaps in recent weeks. Still, expectations were for RBA action across the yield curve, or focusing on longer-dated bonds and fixed monthly purchases.

This is the strongest hint yet from officials on the possibility of QE, coming with a mere quarter of a percentage point gap before interest rates hit their effective lower bound of 0.25%. Such measures could come as early as May, according to Commonwealth Bank of Australia, the nation’s largest bank.

The RBA would want to ensure yields for bonds up to three years remained low to foster loose financial conditions for household borrowing, JPMorgan strategist Sally Auld wrote in a note.

“This is an easier policy to implement quickly than asset purchases,” she said of yield-curve controls.

In comments after a speech, Debelle suggested the RBA would need to be operating “as necessary” in the bond market to keep the yield curve consistent with its outlook for interest rates.

Tailored Circumstances

As a small sovereign debt market, investors have long pointed to the roadblocks facing the RBA if it became a mega buyer of the nation’s bonds. Australia’s net government debt was estimated to be about 21% of its gross domestic product last year, compared to 81% in the U.S. and 154% in Japan, according to the International Monetary Fund.

The Bank of Japan undertook a yield curve control policy in 2016 after large-scale asset purchases and negative interest-rates failed to adequately boost price growth, though inflation remains short of its target.

By targeting Australian yields up to 5-year maturities, this “would deliver YCC that is more tailored to Australian circumstances, with the majority of mortgage and business lending at this tenor or below,” said Su-Lin Ong, Royal Bank of Canada’s head of economic and fixed-income strategy, in a note.

In practice, this could mean a 5-year yield target of 25 basis points over the cash rate, with a “cap” of another 10–20 basis points higher, she added.

The 5-year yield dropped 8 basis points to 0.43% on Wednesday, just below the RBA’s policy rate of 0.5%.

For fund managers such as M&G Investments, yield-curve control measures will be a far more welcome development than negative interest-rates to kickstart Australia’s economy.

“If we do get a prolonged crisis, I do think central banks will need to do more than what we have seen so far,” said Pierre Chartres, fixed-income investment director in Singapore. They “will have to be maybe be a little bit innovative” to avoid negative interest rates.

--With assistance from Michael Heath.

To contact the reporters on this story: Stephen Spratt in Hong Kong at sspratt3@bloomberg.net;Ruth Carson in Singapore at rliew6@bloomberg.net

To contact the editors responsible for this story: Tan Hwee Ann at hatan@bloomberg.net, Cormac Mullen

©2020 Bloomberg L.P.