Rates Market Lurches Toward Fed’s Darker 2020 Policy Scenario

Rates Market Lurches Toward Fed’s Darker 2020 Policy Scenario

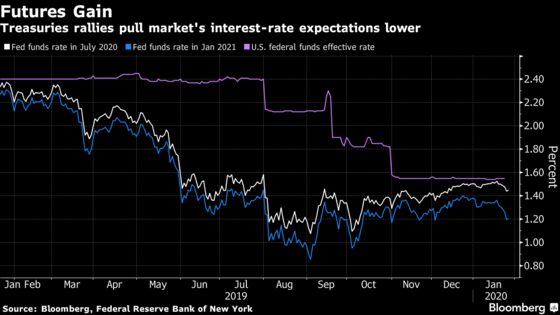

The coronavirus’s rapid spread has spurred buying of super-safe assets, driving gains in interest-rate markets as stocks tumble. Last week, the futures market saw one rate cut by year-end, but now it’s fully priced for that to happen by October.

Related story: Treasuries rally after travel bans stir havens, Fed-cut bets

That shift is to the benefit of investors like Aberdeen Asset Management’s James Athey, who’s putting money on short-dated Treasuries and futures on the basis that a serious downturn will force the Fed to ease aggressively, starting as soon as March.

“Look where equities are, look at the world we’re facing up to,” Athey said. “I think by the end of Q1 they will have had to cut.’

This call is still out of consensus. Indeed, investors say the near-zero chance of a hike is skewing the market. They view the single cut priced in as reflecting a split between bets for rates on hold -- the Fed’s stated preference -- and a smaller camp calling for steep cuts. That’s in line with the Fed’s pledge that it will act on a “material reassessment” of the outlook.

Policy makers may be gratified the market is heeding them, even if the interpretation of the Fed’s message varies. That’s a change from last year, when traders insisted that multiple cuts were coming even as the Fed kept hikes on the table. And the market prevailed, securing 75 basis points of easing to head off a downturn despite a robust labor market and above-trend growth. Treasuries turned in their best performance since 2011.

Drastic action is a tough call with U.S. payrolls still adding in excess of 100,000 a month, and no one expects the Fed to signal much shift in its intentions at this week’s meeting. Jefferies Senior U.S. rates trader Dave Shiau wrote in a note Monday that “the Fed will be pretty neutral.”

Some have also argued that the bar to action in this election year, particularly anywhere near November, is high given the risk of appearing to have succumbed to unprecedented political pressure.

The pessimists’ case rests on an economic or markets downturn so worrying that the Fed will cast any political reservations aside. The virus adds to the risks that could topple stock markets, or push the global economy toward recession. These include a further slowdown in China, another flare-up in Iran-U.S. tensions, domestic political uncertainty, and concerns about the Fed’s plans to wind up programs supporting money markets.

“What the market’s pricing in is probably conservative, and if there’s any sort of weakness the cuts could come in as early as midyear,” said Subadra Rajappa, head of rates strategy at Societe Generale, which forecasts a recession and as many as four cuts this year.

Even money managers like Nils Overdahl, who don’t see the central bank forced into action this year, say that any cut would likely be steep.

“While I think it’s a low probability we get a Fed cut this year, I think if they get to the point where they’ve got to cut once, they’re probably cutting multiple times,” said Overdahl, senior portfolio manager at New Century Advisors.

NatWest strategist Blake Gwinn said the strongest near-term catalyst for markets to rally around deeper cuts would be if stocks tumble from what some consider to be precarious heights.

“If we look at the past three or four years we’ve had periods, often in the first quarter, where there was a big stock sell-off,” Gwinn said. “If we were to get something like that, that’s one thing that I think could very quickly switch the narrative by the Fed.”

To contact the reporter on this story: Emily Barrett in New York at ebarrett25@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Debarati Roy, Mark Tannenbaum

©2020 Bloomberg L.P.