Rate Cuts Bring Earnings Headwinds, and Gains, for Canada Banks

Rate Cuts Bring Earnings Headwinds, and Gains, for Canada Banks

(Bloomberg) -- The Bank of Canada’s interest-rate cut is likely to hurt earnings at the country’s biggest lenders as they face a margin squeeze -- but there may be some offsets.

TD Securities analyst Mario Mendonca trimmed his earnings expectations for Canadian banks following 50-basis-point cuts by both the U.S. Federal Reserve and the Bank of Canada. On Thursday, Mendonca lowered his fiscal 2021 estimates by 3% for Bank of Montreal and Toronto-Dominion Bank, and 1% to 2% for other banks. His revision assumes no further cuts.

The Bank of Canada cut its overnight lending rate by half a percentage point to 1.25% on Wednesday, the lowest since mid 2018, following Tuesday’s move by the Fed. Canada’s large lenders matched the central bank’s move with cuts to their own prime rate, which influences borrowing costs for variable mortgages and credit lines. Royal Bank of Canada, Bank of Nova Scotia and other large Canadian lenders now have prime rates of 3.45%, a level not seen since the first half of 2018.

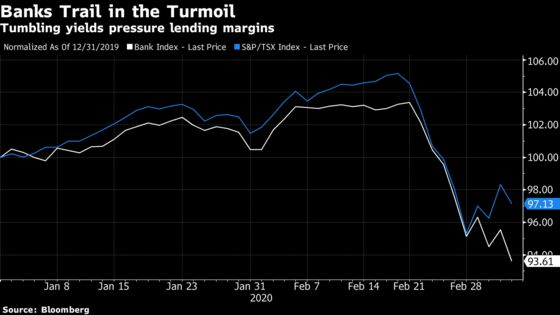

The cuts can erode earnings as the banks face tighter net interest margins -- the difference between what a bank charges for loans and pays for deposits. Three rate cuts by the Fed last year showed up in financial results of the Canadian banks in the fiscal first quarter. Those with significant U.S. operations, such as Toronto-Dominion Bank and Bank of Montreal, showed the tightest margins in years for their American divisions.

Ahead of the move by the Bank of Canada, analyst Gabriel Dechaine of National Bank of Canada forecast that an immediate 50-basis-point cut in Canada would have a less pronounced impact on Canadian margins at personal and commercial banking divisions of the country’s largest lenders.

“However, considering the size of the domestic loan and deposit books, the absolute earnings impact could be larger,” Dechaine wrote in a March 3 note to clients, adding that such a cut would reduce per-share earnings at the lenders by 1% to 2%.

Homebuying Season

TD’s Mendonca said he expects “elevated” mortgage competition, given changes to Canada’s five-year bond yields -- an added challenge in a key lending product for the domestic banks as Canada enters its spring homebuying season.

“Reflecting the low yields and following the interest rate cuts, several of the banks announced a meaningful mortgage-rate cut,” Mendonca said in a note to investors. “At this time, our estimates reflect continuing retail banking competition in 2020.”

Banks can also see some benefits from rate cuts, according to Scotia Capital analyst Sumit Malhotra.

“In theory, rate cuts can help other components of bank earnings power,” Malhotra said in a note to clients. “These include an increased demand for loans, reduced interest rate burden on borrowers that should benefit credit quality, and lower cost of leverage that can fuel business activity and/or consolidation.”

Robert Colangelo, DRBS Ltd.’s senior vice president of credit ratings for North American financial institutions, expects earnings growth at the banks to moderate through the rest of 2020.

“The banks have been dealing with this low-interest-rate environment since the financial crisis, so they’ve become fairly well adept at managing through something like this,” he said.

To contact the reporter on this story: Doug Alexander in Toronto at dalexander3@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, ;Derek Decloet at ddecloet@bloomberg.net, Jacqueline Thorpe, Daniel Taub

©2020 Bloomberg L.P.