Rapid Market Swoon May Not Be as Ominous as Feared

Rapid Market Swoon May Not Be as Ominous as Feared

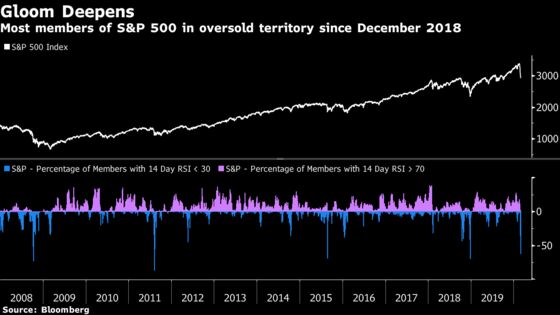

(Bloomberg) -- The S&P 500 Index has not seen so many of its members fall so fast and so far since the year-end sell-off in 2018.

Yet, some strategists say this is just the correction that was needed after stocks scaled to record highs, only to be partly undone by fears of the widening coronavirus outbreak.

The widely-followed gauge for U.S. equities is now down for the seventh straight session, with today’s move fueled by the World Health Organization’s decision to raise its global risk level and a White House official’s suggestion that some schools could close. Countries around the world have also started reporting new cases, adding to the nervousness.

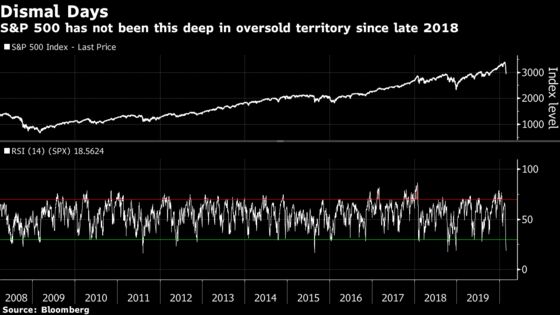

After Friday’s plunge, the S&P is now down 13% from the record high reached on Feb. 19. According to the 14-day relative strength index, which tracks the persistence and magnitude of price swings, the S&P last had this many of its members in the oversold territory during the Christmas Eve sell-off in 2018.

“We got the correction we have been looking for,” Canaccord Genuity’s Tony Dwyer and Michael Welch said in a note on Thursday. “The market has now become washed out enough to generate a meaningful reflex rally.”

The strategists expect that at some point in the next month, major market indices will test the lows, with more intermediate-term indicators turning pessimistic. “It is at that point we plan to put more offense back on the field,” they wrote, citing historically low interest rates, full employment and widely available credit.

Meanwhile, the S&P 500 itself has not been this low, this persistently since mid-2015.

According to Mark Haefele, chief investment officer at UBS Global Wealth Management, history shows that once a disaster hits and markets sell off, investors “tend to be bad at pricing in how quickly growth can recover.”

As an example, Haefele cited Japan’s 2011 Fukushima nuclear disaster. The consensus expectation for third-quarter gross domestic product was 1.6%, though in reality it came in at just over 10%.

“While we cannot say exactly when the coronavirus uncertainty will peak, we think many of the conditions that can allow for a rapid recovery are in place,” Haefele said, recommending that investors buy oversold sectors such as the U.S. consumer discretionary and communication services. The sell-off also provides opportunity to take position in long-term winners, exposed to key trends such as genetic therapies, 5G, artificial intelligence and big data, he said.

To contact the reporter on this story: Esha Dey in New York at edey@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Will Daley, Steven Fromm

©2020 Bloomberg L.P.