Quirk in Europcar Credit Insurance Offers Lucrative Trade

Quirk in Europcar Credit Insurance Offers Lucrative Trade

(Bloomberg) -- An anomaly in credit insurance on Europcar Mobility Group could prove lucrative for some traders as the French rental-car firm seeks to restructure 1.3 billion euros ($1.5 billion) of debt.

The cost of buying Europcar’s bonds and credit-default swaps in a combined trade has risen to 110% of the notes’ face value, indicating that traders expect they’ll get more than par if the insurance pays out, according to Jochen Felsenheimer, who trades both markets as managing director at XAIA Investment GmbH. He doesn’t have a position in Europcar.

Swaps typically pay 100% of face value in a successful settlement, and investors are betting a payout on Europcar would be higher than normal because of an unusual feature -- the contracts reference a loan, as well as the company’s bonds. A 50 million-euro loan from Credit Suisse Group AG last year was designed to be deliverable into credit swaps and traders are betting that will have a lower recovery value.

“For some people, this will have been a superb trade,” said Munich-based Felsenheimer, who saw the package quoted at about 100% of face value a couple of months ago. “It’s a very special situation because of the loan being deliverable and cheaper to deliver than the bonds.”

It’s unusual for swaps to be linked to loans and a derivatives index tied to them stopped trading because there wasn’t enough liquidity in the underlying contracts.

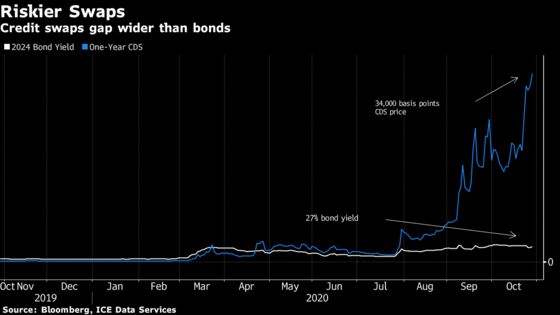

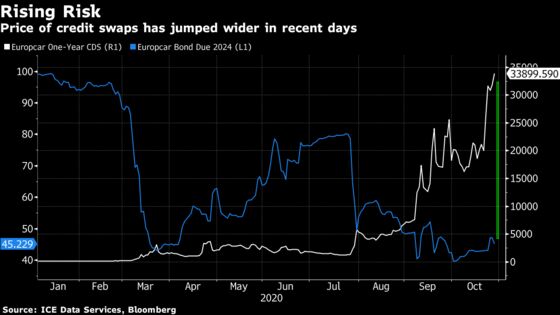

Europcar has struggled since the Covid-19 pandemic prompted a collapse in international travel, wreaking havoc on the tourism industry. Its bonds are quoted at about 45 cents, while the swaps signal a 95% likelihood of default within a year, according to prices compiled by Bloomberg and ICE Data Services. Loans are traded privately, but the swaps indicate that traders see it trading lower than the bond.

Spokespeople for Europcar and Credit Suisse declined to comment.

Read more: Europcar to Start Restructuring Talks Amid Travel Disruption

Outstanding swaps insure about $100 million of Europcar’s debt, according to Depository Trust & Clearing Corp. The contracts are changing hands as traders bet on a possible payout, with more than $30 million traded in the week ending Oct. 27.

The cost of default protection on Europcar’s bonds is also increasing relative to the bond price. The gap between the two has jumped to the equivalent of 34,000 basis points compared with less than 40 basis points in January, according to data from Bloomberg and ICE Data Services.

Credit insurance may be more expensive in part because of demand to hedge bond holdings and express short views on the company. Buying credit swaps is a quicker and cheaper way of expressing a negative view than shorting with bonds.

©2020 Bloomberg L.P.